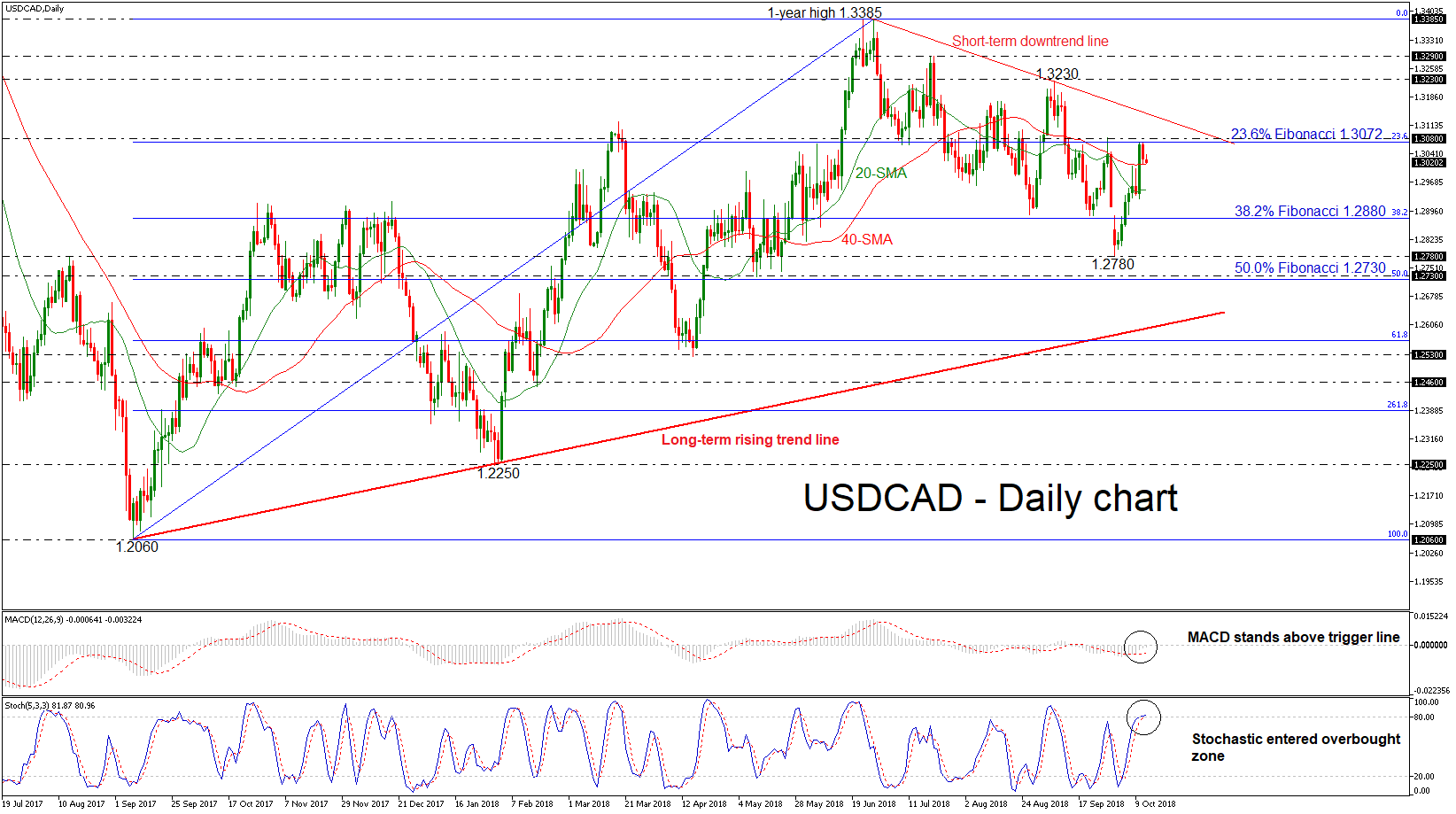

Technical Analysis – USDCAD rally eases below short-term downtrend line

USDCAD has eased back down again after finding resistance at the 23.6% Fibonacci retracement level of the upleg from 1.2060 to 1.3385, around 1.3072. The price is paring some of the previous days strong gains and remains in a short-term bearish bias, despite that it stands above the 20- and 40-simple moving averages (SMAs) in the daily timeframe.

However, the technical indicators are suggesting for a possible upside movement as the MACD oscillator is trying to surpass the zero line and moves above the trigger line, while the stochastics holds in the overbought zone with weak momentum.

In case of an upward attempt above the 23.6% Fibonacci and the downtrend line, dollar/loonie would likely meet resistance at the 1.3230 barrier. A break above this line would send prices until the 1.3290 resistance level, achieved on July 19. Further gains would push the market until the one-year high of 1.3385.

On the other side, a drop below the SMAs, immediate support is being provided by the 38.2% Fibonacci mark of 1.2880, which is acting as major obstacle for the bears. If prices dip below of this area, the next support would likely come from the latest bottom of 1.2780 and then could hit the 50.0% Fibonacci around the 1.2730 barrier, taken from the low on May 11. A drop below the 50% Fibonacci level would signal the start of a deeper bearish phase, challenging the longer-term rising trend line again.

Regarding to the bigger picture, the bullish outlook remains intact as USDCAD stands above the ascending trend line, which has been holding since September 2017. The short-term negative movement would be erased if the price surpasses the downtrend line.

Author

Melina joined XM in December 2017 as an Investment Analyst in the Research department. She can clearly communicate market action, particularly technical and chart pattern setups.