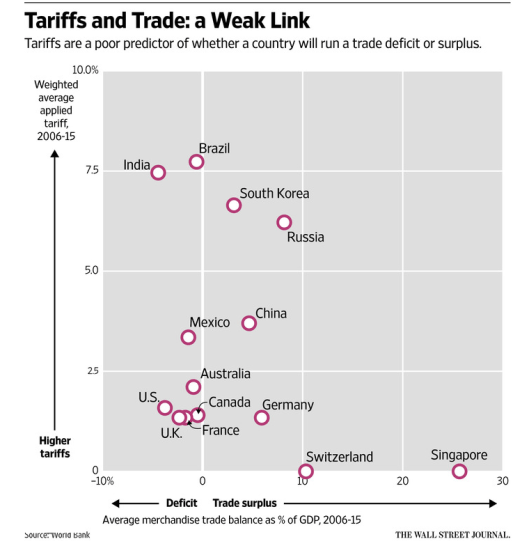

Tariffs: A Poor Predictor of Trade Surplus or Deficit Flows

President Trump believes in bilateral trade negotiations, with tariffs, if necessary, to cure alleged imbalances. House speak Paul Ryan is on board with a Border Adjustment Tax (BAT) proposal.

Wall Street Journal writer Greg Ip says Deficits Are a Flawed Guide to Unfair Trade.

At least one of the positions is wrong.

"President Donald Trump seems to be spoiling for a fight with some of America’s biggest trade partners. The problem is how he judges victory. “I’m trying to find a country where we actually have a surplus of trade as opposed to a deficit,” Mr. Trump groused last month.

The U.S. has a trade deficit because it consumes more than it produces. Lacking sufficient savings, the U.S. sells assets such as stocks, bonds or other IOUs to foreigners to finance consumption and capital spending. A trade deficit always equals an inflow of foreign capital.

This deficit arithmetic isn’t controversial; the dispute is over what causes it. Mr. Trump and Peter Navarro, director of his National Trade Council, blame unfair trade, arguing that other countries are cheating in the global trade arena. His critics say it’s the appeal of the U.S. as a destination for investment.

Both arguments are an oversimplification. Trade deficits and capital inflows result from a combination of U.S. and foreign saving, consumption, and investment behavior, much of it benign but some of it not.

Mr. Trump’s argument implies there should be some correlation between protectionist barriers and the trade balance. There isn’t. Brazil and India are highly protectionist yet run persistent trade deficits because they save less than they invest. Conversely, Germany, and Switzerland have low tariffs yet run persistent trade surpluses because of their high saving relative to investment.

In the past, Chinese currency intervention and tight controls on capital inflows kept the yuan artificially cheap and its trade surpluses inflated. Brad Setser of the Council on Foreign Relations says Taiwan and South Korea have held down their currencies via currency intervention and by encouraging domestic investors to buy foreign assets and discouraging foreign investors from buying domestic assets.

These actions are legitimate cause for complaint. Yet finding an effective deterrent has eluded previous presidents and it’s not clear what Mr. Trump can do differently. Punishing China for manipulating its currency makes less sense now that China is trying to prop it up, rather than push it down as in the past.

Mr. Trump might use deficits to pick the wrong fights. Mexico runs a trade surplus with the U.S. Mr. Trump seems determined to fix it by renegotiating the terms of the North American Free Trade Agreement and slapping tariffs on companies that outsource production to Mexico.

But Mexico runs a trade deficit with the world as a whole. The U.S. would be attacking a country that on net is reducing the world’s excess of saving, not contributing to it. If the economic and diplomatic damage weren’t enough, that’s one more reason for the president to be careful about how he picks his battles."

Bilateral Nonsense

Ip is correct about many things, especially Mexico. It’s more than a bit ridiculous to propose Mexico rebalance with the US when such a tactic would increase Mexico’s overall imbalance.

Were Mexico to react the same was as Trump proposes, Mexico would raise tariffs with the rest of the world. But have tariffs helped Inia or Brazil? Any country?

A global trade war would undoubtedly start if deficit countries all took to tariffs as the cure.

Undervalued Yuan?

Talk of an undervalued yuan is nonsense. China is acting to strengthen its currency.

Trump ought to be happy about that. He isn’t. And if China removed capital controls and floated the Yuan, the yuan would likely crash.

Japanese Savings

IP notes “Japan’s high-saving workers fueled its trade surplus; as those workers have retired and spent their savings, the surplus has disappeared.”

That’s not quite accurate. The Japanese government squandered every bit of Japanese savings and much more, building bridges to nowhere in a foolish endeavor to defeat deflation.

Consumers vs Jobholders

IP notes “When another country subsidizes its exports and restricts imports, it benefits American consumers at the expense of domestic factory workers.”

In other words, the US benefits and the other country loses. Does it make sense for everyone in the US pay dramatically more for cars, clothes, food, electronics, etc to save a few thousand jobs?

Of course, not. Standards of living rise when more goods are available at cheaper and cheaper prices. Thus, the entire notion of “fair trade” to force up prices is ridiculous.

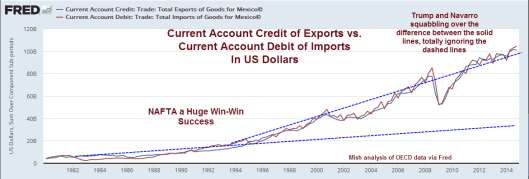

Don’t Blame NAFTA

Trump and Navarro moan about NAFTA causing a loss of US manufacturing jobs. If anything, NAFTA stabilized or increased US manufacturing jobs for six or seven years thanks to an increase in bilateral trade.

The demise of US manufacturing jobs started in June of 1979, long before anyone could blame either Mexico or China.

US Balance of Trade in Goods with Mexico

Goods Trade with Mexico

It’s impossible to make a realistic case that NAFTA hurt the US.

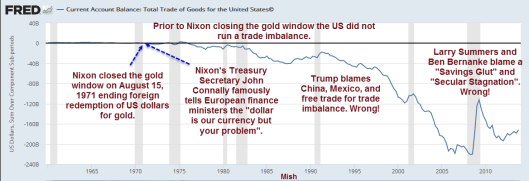

Effective deterrent

Ip says “Finding an effective deterrent has eluded previous presidents and it’s not clear what Mr. Trump can do differently.”

Actually, it’s quite simple. The trade imbalance mess and a whole array of associated problems started when Nixon closed the gold window.

Explaining Balance of Trade

The seeds of trade imbalances were sewn in 1971 when Nixon closed the gold window. The trade deficit rose, then skyrocketed.

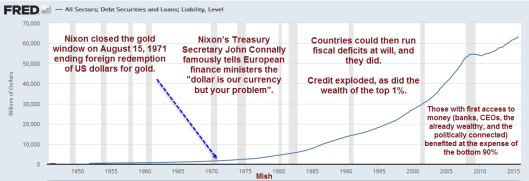

Total Credit Market Debt Owed

Following Nixon closing the gold window on August 15, 1971, credit soared out of sight to the benefit of the banks, CEOs, the already wealthy, and the politically connected.

Confusing Savings With Monetary Printing

One final place IP goes wrong pertains to savings imbalances. It’s a huge mistake to confuse monetary printing with savings. Let’s start with a proper definition of savings:

Savings = production – consumption.

The entire notion of a “savings glut” based in dollar terms is nonsensical.

Every country on the planet is spending far more than it takes in. Central banks print monetize the debt to make up the difference. That cash, printed out of thin air, gets deposited and is widely referred to as “savings”.

The system is so distorted, it’s impossible to measure the pool of real savings. But we can say the system sure has been good for the 1% and especially the 0.1% who have amassed most of the world’s monetary wealth.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc