Structural weakness in the shadow of solid job gains

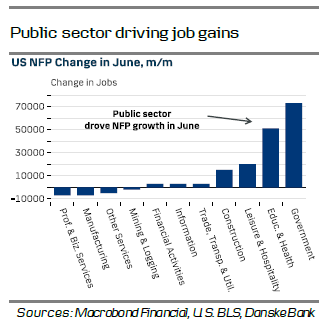

US labour market conditions have remained solid, with June’s jobs report exceeding expectations for the third consecutive month. Nonfarm payrolls rose by 147k (cons: 110k), and May’s figures were revised up to 144k. The unemployment rate dropped to 4.1% (cons: 4.3%), partly driven by a decline in the participation rate from 62.4% to 62.2%. However, decomposing figures reveals headwinds, as half of the NFP growth stemmed from the government sector (first chart). This was mirrored in the ADP report, which surprised to the downside with a reduction of -33k private sector jobs.

Wage pressures remained moderate, with monthly growth momentum in average hourly earnings slowing to just 0.2% m/m SA (prior: 0.4%). The average workweek was shorter, which might indicate that businesses were reducing hours amid economic headwinds.

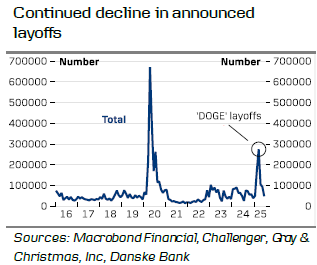

The May JOLTs report was solid, with job openings ticking higher to 7.8m (prior: 7.4m), exceeding expectations. Involuntary layoffs declined modestly, but hiring was also a little slower. The Challenger report also showed a continuing decline in planned layoffs by US firms, returning to the levels prevailing before the surge in public sector layoffs during the first half of the year (second chart). Continuing claims for unemployment insurance have edged somewhat higher over the past weeks, but remain low in historical context.

Leading indicators present a mixed picture. The Conference Board’s consumer confidence index saw a broad-based decline to 93.0 in June. Even if perceptions of current job availability remain in positive territory, consumers are feeling more pessimistic about future business conditions and employment prospects. The NFIB Small Business Optimism Index remained steady in June, highlighting reduced uncertainty among businesses.

While the US labour market keeps showing resilience amidst headline job gains, underlying structural weaknesses persist. Firms appear to scale back hiring, and at the same time, slowing immigration is constraining labour supply growth (third chart). As long as the number of layoffs remains low, the Fed can afford to remain in a wait-andsee mode. But as rising tariff costs put pressure on firms’ margins, we expect labour markets to generally cool towards the fall.

Fed Chair Powell emphasised a still-solid labour market in his recent testimony before the Senate, while noting the Fed continues to closely monitor unemployment trends for any signs of potential weakening. The latest Jobs Report caused markets to erase nearly all bets for a July rate cut, with markets now anticipating the Fed to ease monetary policy twice instead of three times in 2025. Current pricing is well aligned with our view as well, as we continue to forecast the next Fed cut for the September meeting, followed by quarterly cuts until the policy rate target reaches 3.00-3.25%.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.