Strategy: Risk is building of higher US yields

Jackson Hole symposium takes centre stage

For the next couple of months we expect the ECB and Fed to set the tone in the global fixed income market given that a range of important policy meetings are coming up.

The ECB will have to decide if the economic recovery that delivered positive growth for the 17th quarter in a row is strong enough to allow for a slower pace of QE purchases or even an end to the purchases when the programme runs out at end-December. Or if the sudden appreciation of the euro that has shaved tenths off the already modest 2018/2019 inflation forecasts means that fulfilment of the inflation target has become even more difficult to reach for the ECB.

The Fed will have to decide when to implement the announced reduction of the SOMA portfolio (quantitative tightening) and importantly decide whether the rate hikes will continue in light of the tight labour market or rather if it is time to announce a pause given the quantitative tightening and ongoing low US inflation data.

Therefore the market will scrutinise any central bank comments from the upcoming Jackson Hole symposium and especially whether Draghi and Yellen will unveil their plans for the autumn. That said, Reuters this week rep orted from "ECB sources" that Draghi will not deliver a "p olicy message" at Jackson Hole this y ear. But who knows, the market has been surp rised before desp ite what anonymous "ECB sources" ap p arently have said to various media.

Risk is growing of a US-led fixed income sell-off

This week we published our monthly Yield Outlook. Basically we argue that 10Y bond yields in Germany, Scandinavia and the US will remain in a close range around the current level for the rest of 2017 though with small upward pressure. However, in 2018, the picture looks set to change. We think the ECB will have started tapering, the Fed will be on course to deliver further rate hikes and very little is priced into the US curve.

However, we stress that risks to our forecasts are that the drivers we see for higher yields in 2018 materialise much earlier than we forecast.

The ECB might put more weight on the better economic data and argue that an extension of the QE programme is unnecessary . The ‘lack' of eligible bonds might also force the bank to end the programme earlier than we expect. If the programme is not extended or scaled back quickly in 2018, it will tend to steepen the yield curve. It is also worth keeping an eye on Sweden. Higher inflation and an already high ownership share by the Riksbank make it unlikely that the Swedish QE programme will be extended into 2018.

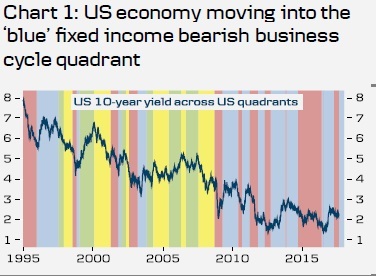

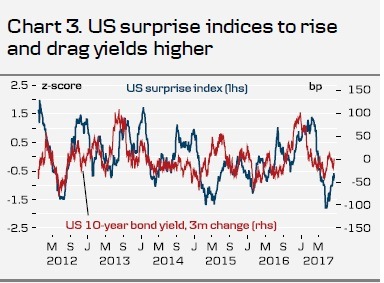

In respect of the US market, the risk of a fixed income sell-off this autumn might be even bigger. First of all our business cycle model, Macroscope, is predicting that the US economy will re-accelerate in the coming months. This is contrary to market consensus, where forecasters - according to Bloomberg - in general expect a modest moderation in growth in Q3 and Q4 compared to Q2. According to the Macroscope model, the acceleration will move the US economy into the so-called ‘Blue' quadrant (acceleratin g growth) that historically has been associated with higher yields and negative returns for US Treasuries (see chart 1). If we see an acceleration in the economy, we should also expect the US Surprise index to move higher and drag yields along with it (see chart 3).

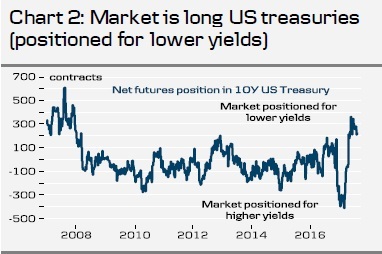

Secondly, we are in a situation where the market has dramatically changed its positioning from being ‘stretched short' US 10Y treasury to being ‘stretched long' US 10Y treasuries according to the CFTC/IMM data (see chart 2). Hence, the market might be caught on the wrong foot if we see the predicted growth acceleration and it pushes yields higher. When the market is caught wrong-footed it often leads to exaggerated movements. For more see IMM Positioning Update, 14 August.

Finally, we should not forget about the Fed. We still forecast that the Fed will make an announcement on quantitative tightening at the next meeting in September and hike for the third time this year in December This is a view that is increasingly at odds with market pricing especially after the June FOMC minutes showed that the FOMC seems to be more concerned about the inflation outlook than previously expected. But given our Macroscope prediction for US growth, we believe the Fed will look through the low inflation and continue to focus on the tight labour market. In that respect it should be noted that the market is only pricing around a 40% probability of a December 2017 hike. An acceleration in the economy should make a December hike more likely.

An important question is which part of the US yield curve would be exposed if we see a more pronounced bond sell-off. We argue that the 5Y segment in particular could be sensitive to a re-pricing of Fed expectations, whereas longer maturities should see continued support from foreign investors looking for a yield pickup that is not found in either European or Japanese fixed income markets. Hence, if we see a US-led fixed income sell-off this autumn we should expect a flatter 5y10y curve in the US. The effect on Europe could be different. The ECB is still keeping a relatively tight leash on the 5Y point, whereas the 10Y point could be pushed higher.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.