Strategy: Goldilocks in risk assets?

Global equity markets and other risk markets continue to perform well, supported by what looks like a ‘goldilocks' scenario for risk assets:

-

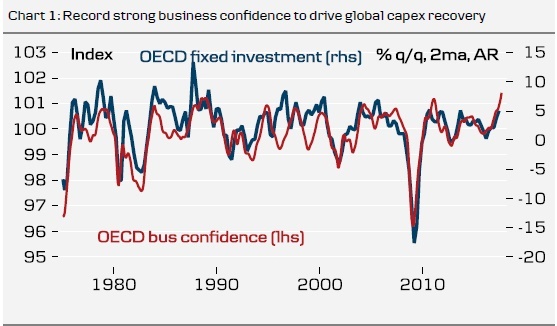

Synchronised global recovery. All regions of the world are participating in the global recovery currently as growth is robust in the US, euro area, China and Emerging Markets outside China. This is reflected in record high OECD business confidence that is set to drive an investment boom across the world (see Chart 1). The global rebound has ignited a double-digit expansion in profits due to rising demand and growth in producer price inflation.

-

Few global imbalances. Although the global recovery is maturing, there are still no significant imbalances that require any adjustment period. A recession tends to follow a period of overinvestment and/or overconsumption. We do not see this happening in the US or Europe. In China, one could argue that investment levels are too high but we believe the government can sustain this for another three to five years.

-

Subdued core inflation keeps central banks in check. While producer price inflation has picked up, it has not spilled over to consumer price inflation pressure. Core inflation is generally low, which is keeping the central banks on a cautious normalisation path.

-

Low return on safe assets. The low rate environment continues to drive a search for yield in risk assets. Lower long-term neutral policy rates increase discounted cash flows of future profits and thus justify higher equity price/earnings ratios.

-

Low tail risks. The risk picture is muted, with North Korea being the main risk. A US-China trade war is also not on the radar this year as was feared previously.

Author

Allan von Mehren

Danske Bank A/S