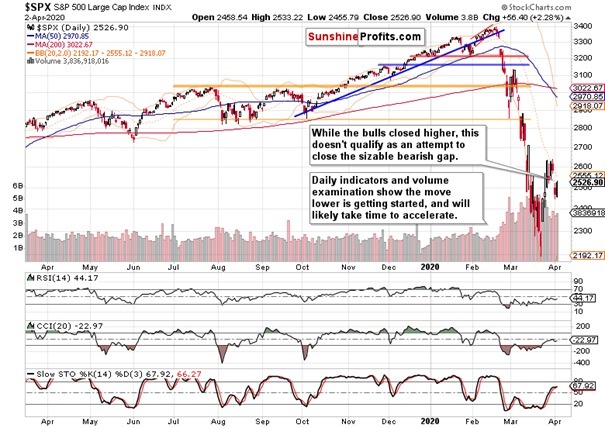

Stocks hanging by the fingernails?

After Wednesday’s slide, the S&P 500 moved higher yesterday. While the move itself hadn’t surprised us as we’ve earlier called for a pause in the downswing, the question is whether we can expect some more upside shortly.

Long story short, that’s unlikely. Let’s open today’s analysis with the daily chart examination.

Considering Wednesday’s bearish gap, stocks have retraced a measly part of the preceding decline. Let’s recall our Wednesday’s observations:

(…) Stocks closed near the daily lows on Tuesday, and did so on higher volume than was the case on Monday. Another point speaking for the bears is that yesterday’s upswing attempt was again soundly rejected. And still, the daily indicators are increasingly and tellingly curling lower.

After Thursday’s session, the daily indicators are overall positioned more bearishly than the day before, lending credibility to the claim of yesterday’s session being merely a pause in the downswing. The bearish gap continues to support the sellers, and we certainly expect the downside move to continue over the coming days.

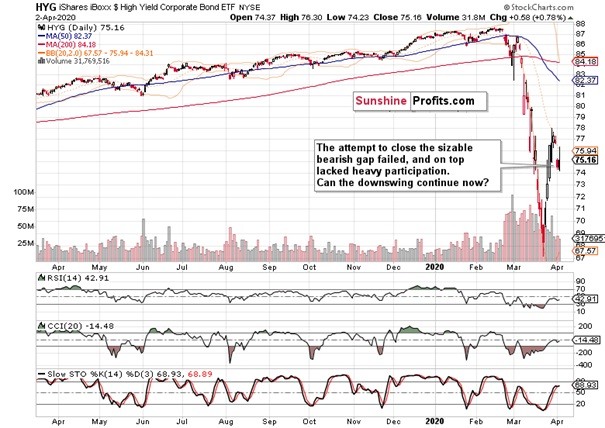

But doesn’t yesterday’s action in the high-yield corporate debt (HYG ETF) constitute a fly in the ointment? After all, the intraday move made us issue this intraday Alert yesterday after the regular Stock Trading Alert was published:

(…) Stocks not merely paused, but also slightly recovered during today’s session so far to trade slightly below 2500 currently. Yet it’s the corporate debt market that is the reason behind this intraday Alert. It recovered and the bulls attempted to close yesterday’s sizable gap. Despite their failure and HYG trading close to its yesterday’s closing prices, stocks are trading higher than they were yesterday – in line with the discussed need to pause in their downswing.

However, should HYG continue its recovery attempts, that wouldn’t be without consequences for the S&P 500. While we continue to think that the stock downswing will carry on in the coming days, it makes sense to tighten the trade position’s parameters and improve its risk-reward ratio – please see the trading position for full details.

The exact position details are reserved for our subscribers. Let’s quote from our yesterday’s regular Alert first as it explains why the debt market is key to stocks:

(…) Comparing the magnitude of yesterday’s downswing shows that stocks are a bit ahead in the sliding game. Unless HYG declines more meaningfully today, stocks are likely to take a short-term pause as they have declined more profoundly yesterday. The emphasis here goes to short-term (which implies that any potential upswing certainly isn’t going to be a tradable opportunity) – unless we see a turnaround in the debt market, any potential stock upswing doesn’t really have legs.

Now, we’ll take a joint look at the HYG action that made us cautious:

The upswing ran farther than expected, and while the odds remain stacked against its possible repetition, it pays to be reasonably suspicious and conservative in one’s trading decisions. After all, we’re in it for the long run and in order to help people fulfill their many dreams.

Summing up, the bears enjoy the upper hand as can be seen on both the weekly and daily charts. The renewed downswing is underway, and lower S&P 500 (and SPY ETF) values are ahead. The daily indicators, high-yield corporate debt market and fundamental prospects of more coronavirus pain and its reflection in market prices mean that our open and increasingly profitable short position remains justified.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.