Stock market illusions part 1

The stock market has performed considerably well since the Global Financial Crisis of 2008. It has also had a tremendous bounce back since the selloff back in March. Many associate the stock market’s performance with the economy. Despite the S&P 500 creating new all-time highs several different times since the end of 2008, this notion could not be further from the truth, as the economy has struggled to recover from the 2008 recession, let alone the recession that began in March of this year (we’ll get more into this in part 2). But, before we do that, let’s take a deeper dive into the stock market’s performance over the last twelve years and what has been its driving force.

There have been two main themes since the end of 2008: first, the Fed’s introduction of Quantitative Easing (QE) which has been used on and off and second, low interest rates. First let’s look at QE, which is when the Fed “prints” money and injects it into the economy. Mainstream media has been writing about how successful this has been for years, mainly because the Fed tells them it’s successful and they believe it, no questions asked. I believe that QE actually suppresses liquidity rather than adds it to the system, but I will leave that for another time. The point is, the mainstream believes QE works and when it comes to financial assets, particularly stocks, that’s what matters. If most investors believe QE to work and then act based on that belief, it becomes a self-fulfilling prophecy. In other words, if people think that QE is going to boost the stock market and it causes them to buy stocks, then the stock market rises, regardless of what QE actually does or doesn’t do.

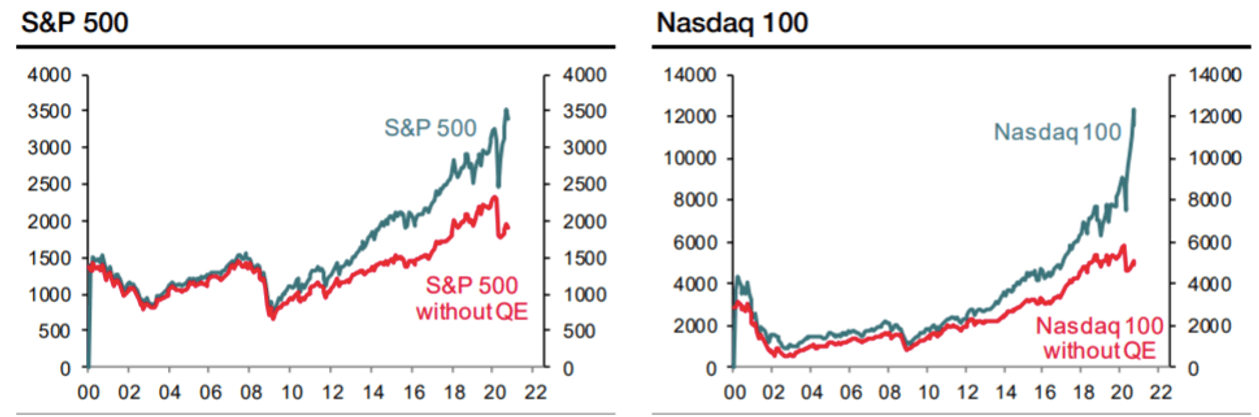

If we take a look (below) at a chart provided by Societe Generale, we can see the actual performance and projected performance of the S&P 500 and Nasdaq 100 with and without QE from the end of 2008 to present time. There is a huge gap between where these indices are and where they may have been if it wasn’t for QE. This gap widens even further post-March 2020 selloff. The rise in the indices after March has been extremely sharp, creating new all-time highs. Without QE, the projected post-March 2020 would be a recovery of barely halfway from where the indices sold off in March. If the projections are anywhere near accurate, it makes it clear that QE has played a major role in the strong performance of the stock market since March, as well as over the last twelve years.

The other piece to this puzzle is the low interest rate environment we have been in since the end of 2008. While low rates are NOT stimulus (I talk about that here) like the mainstream believes, it has certainly helped boost financial assets, particularly stocks and real estate. Interest rates fall because money is tight, as banks and investors get out of risky assets and into safe, liquid ones, like Treasuries. When money is tight banks are only willing to lend to the most creditworthy borrowers, because financial conditions do not warrant risk-taking. So, despite low rates, only those who are creditworthy are able to borrow – the wealthy. The wealthy own the majority of stocks and real estate. It is no wonder that since the end of 2008 stocks and real estate have moved exponentially higher. We have a low interest rate environment that has been accompanied by on and off QE. If those that buy stocks (the wealthy) believe that the Fed is going pump liquidity into the market, boosting it higher, all the while interest rates are low, what are they going to do? They are going to borrow cheap money and buy stocks and real estate, driving prices higher, regardless of the conditions of the real economy.

Low interest rates help financial assets more than they do the real economy. Again, low interest rates tell us that money is tight and only the most creditworthy will be able to borrow from banks. So, cheap rates are benefiting those (the wealthy) that are less likely to spend that money into the real economy – purchasing everyday goods and services. The wealthy are more likely to use that money to buy stocks, real estate, and luxury items like boats, artwork, etc. Because of that, low rates only really benefit financial assets, which is another reason why they are not stimulative in the real economy, despite what the Fed wants us to believe.

QE and low interest rates have been the clear drivers of stocks post-GFC. They aren’t the only factors, but have certainly been major factors in driving the stock market higher. The Fed would like you to believe that the stock market has been booming due to economic growth over the years, but a quick look at a few economic indicators tell us otherwise. That is what I will cover in part 2, how the stock market has been disconnected from the economy since 2008 and how the stock market is NOT the forward looking mechanism many believe it to be.

Author

Ryan Miller

Ryan Miller Trading Economics

Ryan Miller received a Bachelors Degree in History from William Paterson University. Through his studies of U.S. history, he developed an interest in the implications the financial markets have on the economy.