Stock collapse risk grows

There is a confluence of forces at play in the global macro-economic and strategic space that is impacting every citizen of the world at the moment.

No one can escape the distortions to food and energy prices from the Ukraine conflict. Which are not yet over and face increased uncertainty in coming months. The world has not yet recovered from the Covid supply-chain shock, and there has been increased turbulence in this regard in China and elsewhere.

There is no doubting the permanent slowing of China’s economy and the immediately intensified risk there, from the unwinding of their development and property bubbles.

Coming on top of all this, is the making of a truly tremendous crisis, perhaps an economic armageddon, as western central banks religiously adhere to a 1960’s dated playbook in how to address the current global inflation tsunami.

Firstly, inflation was never ‘ ransitory', and we said so in real time over a year ago. Now, upward inflation/wage spirals are becoming ever more self-evident. Particularly in the USA, but also in countries like Australia too.

With consumers, businesses, and investors all reeling from the fatigue of Covid and supply chain dislocations, the uncertainty and fear surrounding war in Europe, which may be about to intensify as Putin mobilises, they are now intensely faced with aggressive interest rate hikes by their respective central banks.

There are problems everywhere, but they are particularly acute in the USA, Europe and the UK.

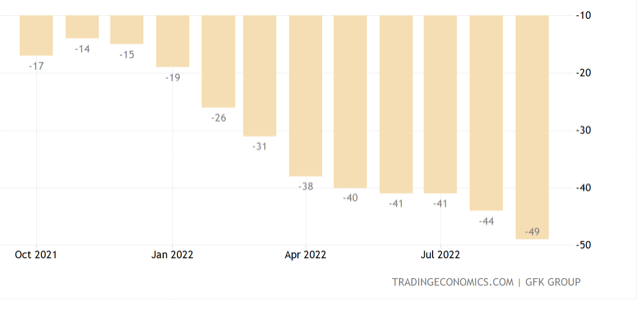

The latter two have the additional challenges of energy supply disruption leading to restrictions during the coming winter? High prices for food and energy, fear over war in Europe, on-going supply chain disruption, likely energy restrictions in times of severe cold, and on top of all that, the EU and BoE continue to hike interest rates. Has the BoE not considered the two charts below. Consumer confidence is in crisis and central banks are aggressively hiking?

There is little prospect in the economies of Europe, the UK, and also the USA as natural gas prices are still double that of a year ago, of there being any respite to an intensifying and complex decline in these economies.

High employment, when employers cannot find workers, only points to economic dysfunction. Not to strength, as many economists erroneously believe. Europe and the USA are heading into recession, and perhaps we should be talking about the ‘D” word more often. Depression.

Stock markets of the USA, Europe and Australia can collapse, if, as seems to be the case over the past few weeks, investors belatedly begin to recognise these risks and price such scenarios into their investment plans.

'Run for the exit’, could quickly become the dominant investment theme of the next several months.

Economic crisis is part of the reason I remain bullish the US dollar. As it is still perhaps mistakenly perceived to be a safe-haven destination. Gold may yet have its day, if the overall economic down-turn accelerates.

At the start of 2022, I forecast a 6-18 month correction in the US stock market of 20% to 30%. I also at the same time, highlighted the further risk scenario of a decline over three to six years. Which could be in the magnitude of 40% to 50%.

Investors cannot afford to look away from their screens for a moment.

With geo-political tensions rising, and central banks hiking aggressively, there is no telling how severe this economic down-turn could become.

Author

Clifford Bennett

Independent Analyst

With over 35 years of economic and market trading experience, Clifford Bennett (aka Big Call Bennett) is an internationally renowned predictor of the global financial markets, earning titles such as the “World’s most a