Still a soft landing?

S&P 500 wasn‘t fooled by sizable government hiring skewing NFPs, and neither was Nasdaq. Its performance showed what matters – it‘s rate cut odds, and two 2024 cuts being priced in with the two-day heavy selling in Treasuries reversed while the dollar is being dumped.

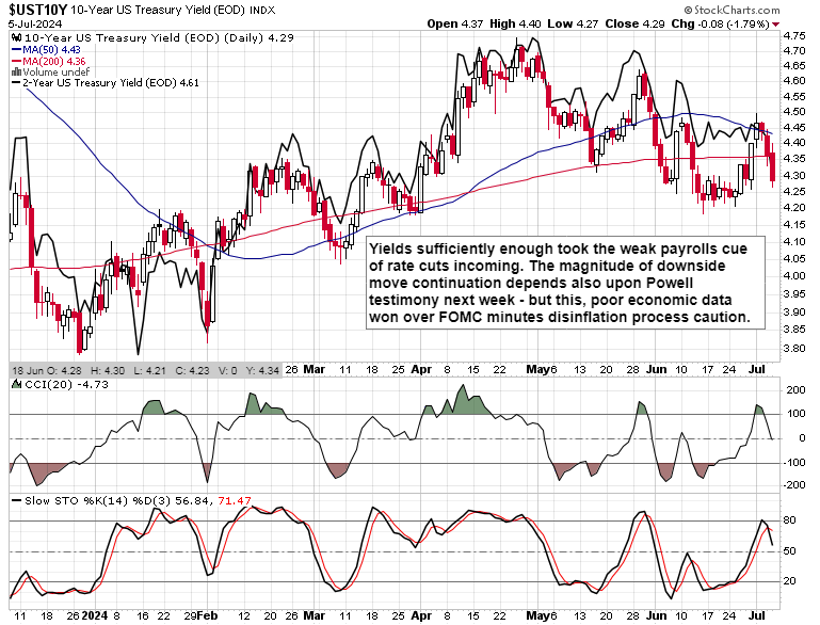

You knew it all from my live NFPs commentary and also about the importance of synchronized global easing – see the very extensive Friday‘s analysis. With the wealth of underwhelming data this week, culminating in the (private, look at private) non-farm payrolls after manufacturing and services PMI – resulting in the odds of the Fed not cutting in Sep dipping to 27% only.

Remember also that my worry had been what kind of (equals how temporary or shallow) the deflationary whiff is going to be. Yes, next week we‘re getting (bank earnings and) both CPI and PPI, and they‘re still to underscore the disinflationary trend. But what is weakening economic growth together with falling inflation? Deflationary whiff is what‘s hanging in the air. Forget for a moment that if we get more of the downward revisions of Friday‘s kind, recession could get retroactively declared to have started before spring 2025.

Is it an issue for the stock market? To drop a couple of clues that I would go on to develop in the premium sections for individual markets, think about where bonds are headed, whether commodities are coming back, and the same applies to Bitcoin following its Friday‘s flush. What did I say about international stocks? Does China look to you as a buy or are you selling here? Look at Nasdaq market breadth, short vs. long end of the curve, and USD as well.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.