Sterling volatility breaking the consolidation of pensive markets [Video]

![Sterling volatility breaking the consolidation of pensive markets [Video]](https://editorial.fxstreet.com/images/Markets/Currencies/Majors/GBPUSD/iStock-688526532_XtraLarge.jpg)

Market Overview

There is a sense of anticipation that has built up across major markets as consolidation has crept in. The major mover right now is sterling, which is like an excitable puppy, trading with significant volatility as it jumps up and down. The EU/UK negotiators have been working hard for several days to get some sort of text ready for the EU Council to consider, and apparently the “foundations” are there. Michel Barnier said last week, “where there’s a will, there’s a way”, so markets are on tenterhooks. However, time is running out for a deal this week and sterling is slipping this morning. Suggestions are that the unionist party in Northern Ireland, the DUP, will not support the deal when it is put to Parliament (probably on Saturday). It is interesting to see that the euro is holding on to its recent positive performance, but it would also suffer should there be an impasse in Brussels/Parliament. Broad risk appetite has been a beneficiary too recently amid the elevated Brexit deal prospects, with yen and broadly US dollar underperformance. However, this could all turn on a sixpence though today. Although Gilt yields and Bund yields have been higher on the Brexit story, Treasury yields have been struggling recently. A worrying decline in US Retail Sales is certainly something that could now play on the minds of Treasuries traders. The US consumer has been doing the heavy lifting with US growth, and if sales start to decline consistently, then this could usher the Fed into more of a dovish cycle.

Wall Street had a bit of a quiet session yesterday, with a mild decline on the S&P 500 by -0.2% to 2990. US futures are again a little cautious today -0.1%. Asian markets were mixed overnight, with both Nikkei and Shanghai Composite almost dead flat. In Europe, there is a slip back for DAX futures (-0.4%), whilst FTSE futures (+0.2%) are being supported by an early decline on sterling. In forex, the GBP decline is the big move, but it is interesting to see AUD stronger after the Australian Unemployment numbers showed the headline rate a shade lower than expected at 5.2%. In commodities, gold and silver are fluctuating around the flat line, whilst oil is stumbling to give back yesterday’s rebound gain.

The economic calendar for the European session is focused on the final of this week’s major UK data. UK Retail Sales (ex-fuel) is at 0930BST and is expected to fall by -0.1% in the month of September (having fallen by -0.3% in August) but this would mean the year on year data would improve to +2.8% (from +2.2% in August). The US data begins with the Philly Fed Business index at 1330BST which is expected to slip back to a still positive +8 in October (from +12 in August). There is also US Building Permits at 1330BST which are expected to drop back to 1.32m in September (from 1.42m in August) and Housing Starts expected to drop back to 1.32 (from 1.36 in August). Weekly Jobless Claims are expected to remain around recent levels, with 215,000 (a shade higher from 210,000 last week). The EIA Oil Inventories are a day delayed this week and are at 1600BST, with crude stocks expected to again be building by +2.7m barrels (2.9m barrels last week), with distillates in drawdown by -2.2m barrels (from -3.9m barrels last week) and gasoline stocks in drawdown by -1.4m barrels (-1.2m barrels last week).

There are more Fed speakers today, with Michelle Bowman (voter, leans hawk) at 1900BST, whilst Charles Evans (voter, leans dove) at 1900BST and John Williams (voter, centrist) at 2120BST.

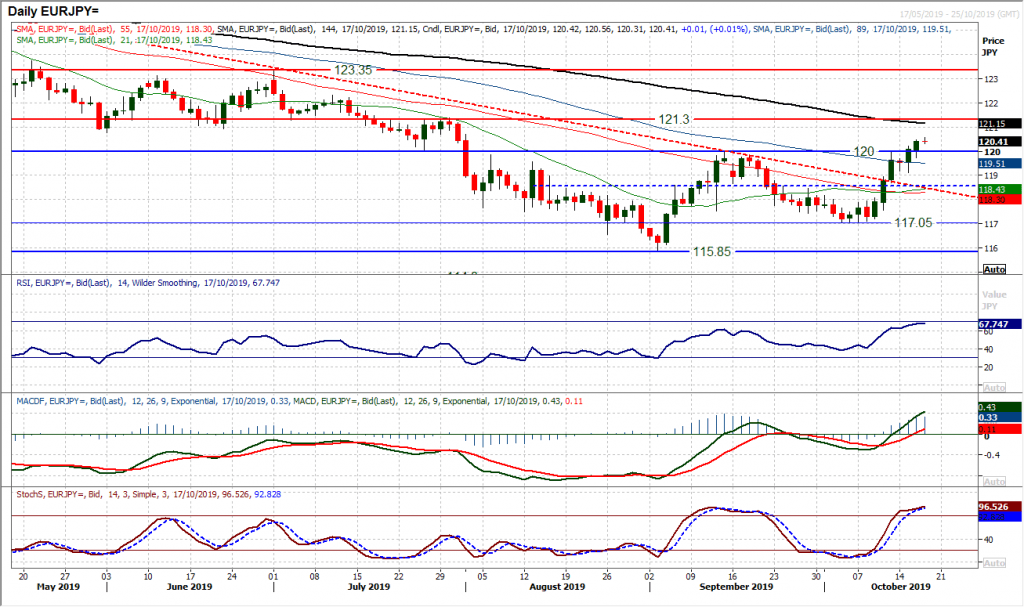

Chart of the Day – EUR/JPY

A risk positive market makes for a weaker yen but positive signs for a Brexit deal are benefitting the euro too. Subsequently the outlook for EUR/JPY has improved significantly recently. Resistance at 120.00 has been a key pivot and a barrier for the past few months. However, yesterday’s latest strong bull candle was a second (confirmatory) closing breakout, taking the pair to an 11 week high. The multi-month downtrend was broken last week and now clearing 120.00 on a decisive basis means that the bulls are finally building some traction in a new positive trend. This has been a crossroads moment that the euro bulls are now pushing through. Momentum indicators are positively configured with RSI in the mid-60s, whilst MACD lines accelerate above neutral for the first real time since April and Stochastics are strong. This points to buying into weakness now. There is a burgeoning run of seven successive higher daily lows now, meaning the support at 119.75 is a key near term gauge and 119.75/120.00 is a near term buy zone. The hourly chart shows 119.10 as the first real higher low and key support. A consistent close above 120.00 opens further recovery to 121.30.

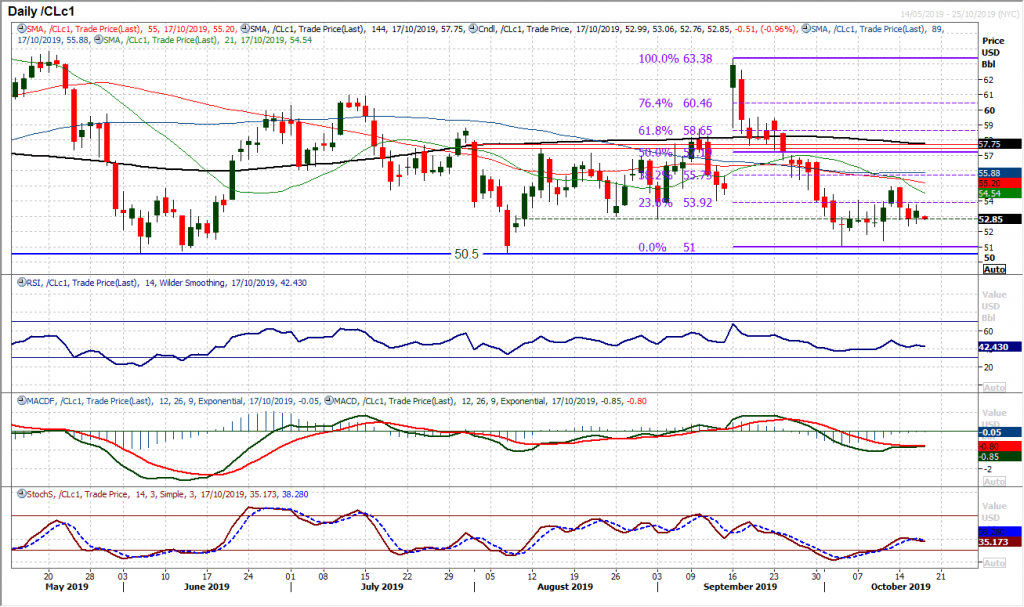

WTI Oil

The renewed selling pressure has just eased in the past 24 hours or so, with the daily chart showing a small positive candle. This sees the market again forming a consolidation around the old August/September lows at $52.85. For about a week earlier in October the market seemed to gravitate around $52.85 and again this seems to be a consolidation area. Momentum indicators on the daily chart are holding ground now rather than showing any real sense of direction. This is similar to the hourly chart where neutral configuration has formed. It seems to be that WTI is a market waiting for a catalyst now. A mini range has come between $52.50/$53.75in the past few sessions and hourly momentum has been lacking conviction. A close either side of this mini band could provide some idea of direction. Key support remains $50.50/$51.00, with the bull failure at $54.90 a key resistance now.

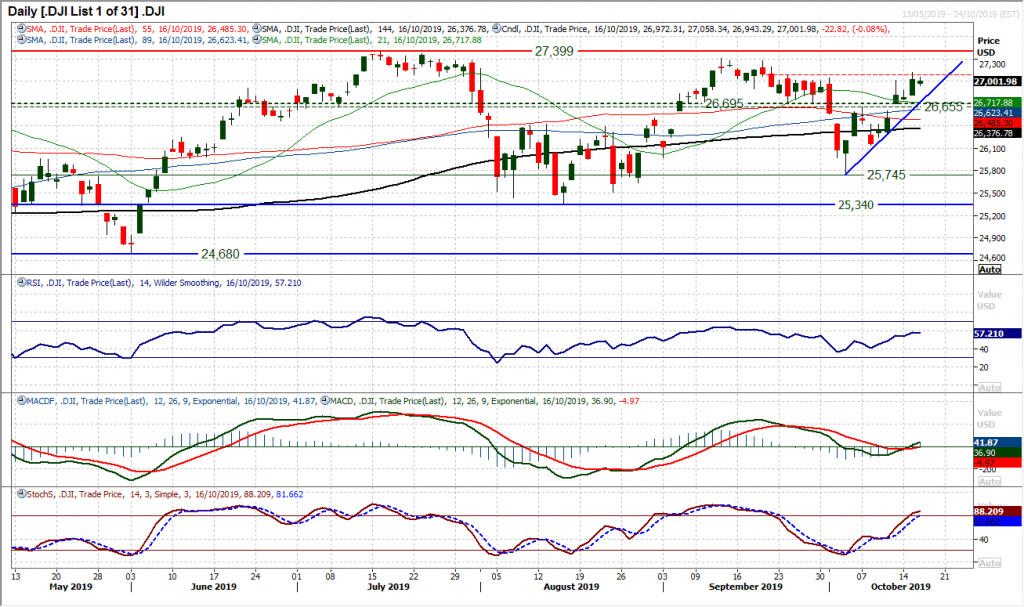

Dow Jones Industrial Average

A slight pause for thought for the bulls as the Dow closed marginally lower last night. However, this has done little to change the current positive outlook. The uptrend of the past two weeks is holding firm and is now rising today at 26,835 which is safely above the 26,655/26,695 medium term pivot band support. There is a continued improving configuration for momentum, with RSI in the high 60s, MACD lines beginning to edge above neutral and Stochastics edging above 80. The only minor caveat is that the old late September highs (27,045/27,080 remain a basis of resistance. With the intraday failure at 27,120 on Tuesday, this means a band of resistance 27,045/27,120 now. This needs to be cleared on a closing basis to open the all-time highs again, at 27.399. We still look to buy into weakness for what is likely to be a test of the highs.

Author

Richard Perry

Independent Analyst