Sterling Steady Pre-Brexit Talks

Last week saw a plethora of bad economic news stateside, starting with continued weakness in inflation, consumer confidence, housing and manufacturing. The Fed followed their script and removed the expected amount of stimulus on the assumption that inflation and the U.S economy will improve.

This week should be much quieter on the central bank and economic fundamental front with only the Reserve Bank of New Zealand (RBNZ) announcing its monetary policy decision (June 21) – expected to maintain at +1.75%. In the U.S, flash June PMI surveys will give investors their first look at this month’s and Q2 end data. North of the border, Canada releases its May consumer price data and April’s retail sales.

Note: With the loonie (C$1.3242) on such a tear of late and with confidence growing in the Canadian economy, the data will be watched carefully for implications to Bank of Canada (BoC) policy.

Among other events, investors will be focused on the start of formal Brexit negotiations.

Note: Chicago Fed President Charles Evans and Fed Bank of New York President William Dudley are both due to speak in New York Monday. They are the first of a slew of Fed appearances scheduled for this week including Vice Chairman Stanley Fischer and Governor Jerome Powell.

1. Global equity markets start the week higher

Financial markets were unshaken on news a vehicle had rammed into a crowd outside a mosque in north London overnight in another suspected terrorist attack.

In Japan, the Nikkei Stock Average closed up +0.6%, with a softer yen (¥111.03) aiding the move and this despite Japan reporting its first trade deficit since January. The broader Topix index jumped +0.6%.

In Hong Kong, the Hang Seng Index gained +1.2% after its first weekly decline in six-weeks. The Shanghai Composite Index rose +0.7%.

Down-under, Australia’s S&P/ASX 200 Index rose +0.5%.

Note: MSCI will announce this week whether it will approve Chinese-listed stocks in its global benchmarks. The +$6.8T ‘onshore’ market is the world’s second largest and accounts for +9% of global stock value – the decision is expected Tuesday after the bell.

In Europe, indices are trading sharply higher with the French CAC slightly outperforming after a comprehensive victory for French President Emmanuel Macrons party in the parliamentary elections.

U.S stocks are set to open in the ‘black’ (+0.3%).

Indices: Stoxx 600 +0.75% at 391.5, FTSE +0.6% at 7510, DAX +1.0% at 12875, CAC-40 +1.0% at 5316, IBEX-35 +0.9% at 10859, FTSE MIB +0.2% at 20989, SMI +0.3% at 8994, S&P 500 Futures +0.3%.

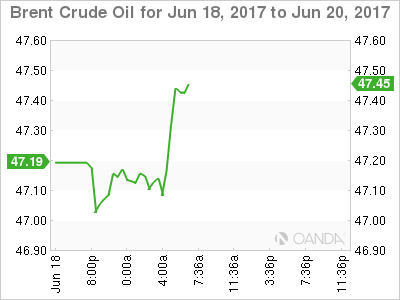

2. Oil slips as U.S rigs rise, gold lower

Oil prices are lower overnight, weighed down by an expansion in U.S drilling that has helped to maintain high global supplies despite OPEC’s initiative to tighten the market by cutting production.

Also, signs of faltering demand are also weakening global sentiment.

Brent crude futures are down -16c at +$47.21 per barrel, while U.S West Texas Intermediate (WTI) crude futures are down -19c at +$44.55 per barrel.

Note: Prices for both benchmarks are down -14% since late May, when OPEC formally extended its pledge to cut output by -1.8m bpd for an extra nine months.

Data out Friday afternoon in the U.S showed another week of rising active U.S oil-drilling rigs, bringing the count to +747, the most since April 2015.

Even at such low price levels, questions on the U.S ‘shale’s’ ability to keep profitable are being asked.

Data also shows that supplies from OPEC also jumped last month, driven by recovering output from Libya and Nigeria, which were exempt from cuts due to unrest that had hindered their output.

Gold has hit a four-week low ahead of the U.S open (down -0.2% at +$1,251 an ounce, up from an earlier +$1,248.63, its lowest since May 24) as the dollar held firm and the market waits for comments from a the Fed’s Evans and Dudley this morning. Prices are being supported by the start of Brexit talks in Europe.

3. Global yields little changed

Yesterday, France’s legislative elections confirmed an outright majority for French President Emmanuel Macron’s centrist La République en Marche and its centrist ally.

Note: President Macron’s “En Marche” party tool 361 out of the 577 seats in the National Assembly, while Marine Le Pen’s National Front party took at least 6-7 seats.

There was little reaction to the election in government bond markets. The spread between France (OAT’s) and Germany’s 10-year Bund yields tightened slightly, to around +0.35 bps.

Note: The spread had blown out during the country’s presidential campaign, becoming a key measure of political risk for investors and rising to as wide as +0.78 bps.

The yield on U.S 10-year notes backed up +1 bps to +2.16%, while Aussie benchmark yields were flat at +2.41%.

Elsewhere, U.K 10-year gilts have rallied +2bps to +1.04%, while those in Germany rose +1 bps.

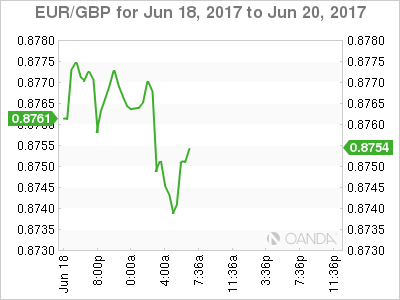

4. Pound steady ahead of Brexit talks

GBP (£1.2805) is firmer across the board as the BoE turned increasingly ‘hawkish’ last week – less willing to look through rising inflation. The BoE’s Financial Policy Committee (FPC) are expected to discuss ending the Term Funding Scheme (TFS) at a meeting this week. Fixed income dealers are speculating that this could pave the way for a rise in interest rates much sooner than had been previously priced in.

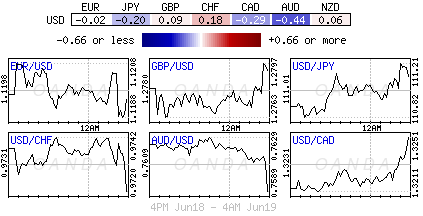

USD/JPY is higher and holding atop of the psychological ¥111.00 level. Aside from last week’s Fed statement, the yen has come under pressure attributed to some political uncertainty in Japan – PM Abe is expected to change up his cabinet in the next few weeks amid approval rating decline (+49% approval rating).

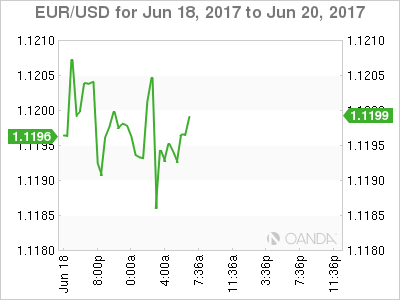

Late Friday, data from the U.S. Commodity Futures Trading Commission showed investors are taking long positions on the EUR once again (+79,053 more long than short contracts in the week to June 16), the largest long position since 2011. The ‘single’ unit is little changed, straddling the psychological €1.1200 handle.

Update: Moody’s has cuts ratings on Australia’s Big Banks on Housing Concerns – A$0.7595

5. Japan’s May trade deficit a surprise

Data overnight saw Japan May Trade Balance register its first deficit in four- months – -¥203B vs. + ¥43B e – the components were mixed with exports missed expectations while imports beat.

A Finance Ministry official noted it wasn’t uncommon for Japan to post a deficit in May because many manufacturers shut down factories during the “Golden Week” holidays, which limits exports.

The market has shrugged off the report as the exports data in Japan continues to reinforce the growth story for domestic economy.

Note: Japan’s exports jumped +15% for May y/y, the biggest rise since January 2015, marking the sixth consecutive month of increases, however, the figure came in lower than an +18% increase expected by the street.

Author

Dean Popplewell

MarketPulse