Sterling looking to hold key breakout ahead of UK wage growth

Market Overview

As geopolitical tensions surrounding Syria have just gone off the boil the market is looking to get back to trading off fundamentals rather than knee-jerk newsflow. It was interesting to see therefore that although Treasury yields ticked higher, the dollar was coming under renewed pressure yesterday. As the US yield curve continues to flatten (2s/10s spread now down at 45 basis points), the market was returning to a negative stance on the dollar. Although the trade tensions rumble on in the background and are also a key factor to keep in mind, it was interesting to see Chinese growth data beating expectations overnight. China GDP for Q1 2018 was higher than expected at +6.8% (+6.7% exp, +6.8% last) and points to a continuation of a soft landing. Risk appetite will be mixed on the news that the economy shows continued signs of reorienting with China Industrial Production dipping to +6.0% (+6.2% exp, +7.2% last) whilst China Retail Sales improved to +10.1% (+9.9% exp, +9.7% last). Equity futures are higher In Europe and the US. With Cable pushing to multi-year highs this morning, sterling traders will be focusing on the prospects for a May Bank of England rate hike with the UK wage growth this morning; whilst euro traders will be considering the deterioration in Eurozone data as the German ZEW is expected to show a negative reading for the first time in 20 months.

Wall Street rebounded well on the feeling that a geopolitical escalation in Syria was less likely, driving the S&P 500 +0.8% at 2678. Asian markets have been mixed in response to the Chinese economic data with the Nikkei a shade higher at +0.1%, whilst European markets are mixed to slightly higher in early moves, once more with the DAX outperforming FTSE 100 on an up day. In forex, there is a mild trend of dollar weakness continuing, whilst the commodity currencies are a touch weaker today on the China data. In commodities there is a basis of support for gold with the dollar weakness, whilst the selling pressure on oil has so far been contained this morning.

The UK labour market is in focus for traders this morning, with UK Unemployment announced at 0930BST which is expected to remain steady at 4.3% (4.3% last month). However the big focus in the announcement will be with the wages, with UK Average Weekly Earnings Growth (ex-bonus) which is expected to further improve to +2.8% (from +2.6% last month). The German ZEW Economic Sentiment for April is at 1000BST and is expected to turn negative for the first time since July 2016 to -1.6 (from +5.1 last month). Into the afternoon, US Building Permits are at 1330BST and are expected to tick up to 1.32m (from 1.30m last month), with Housing Starts at 1.26m (from 1.24m last month). US Industrial Production is at 1415BST and is expected to grow by +0.4% for the month (+0.9% improvement last month) with Capacity Utilization improving to 77.9% (from 77.7% last month) which would be the best level since March 2015. There are two Fed speakers today with Randy Quarles (voter, centrist) at 1500BST and Raphael Bostic (voter, mild dove) at 2240BST.

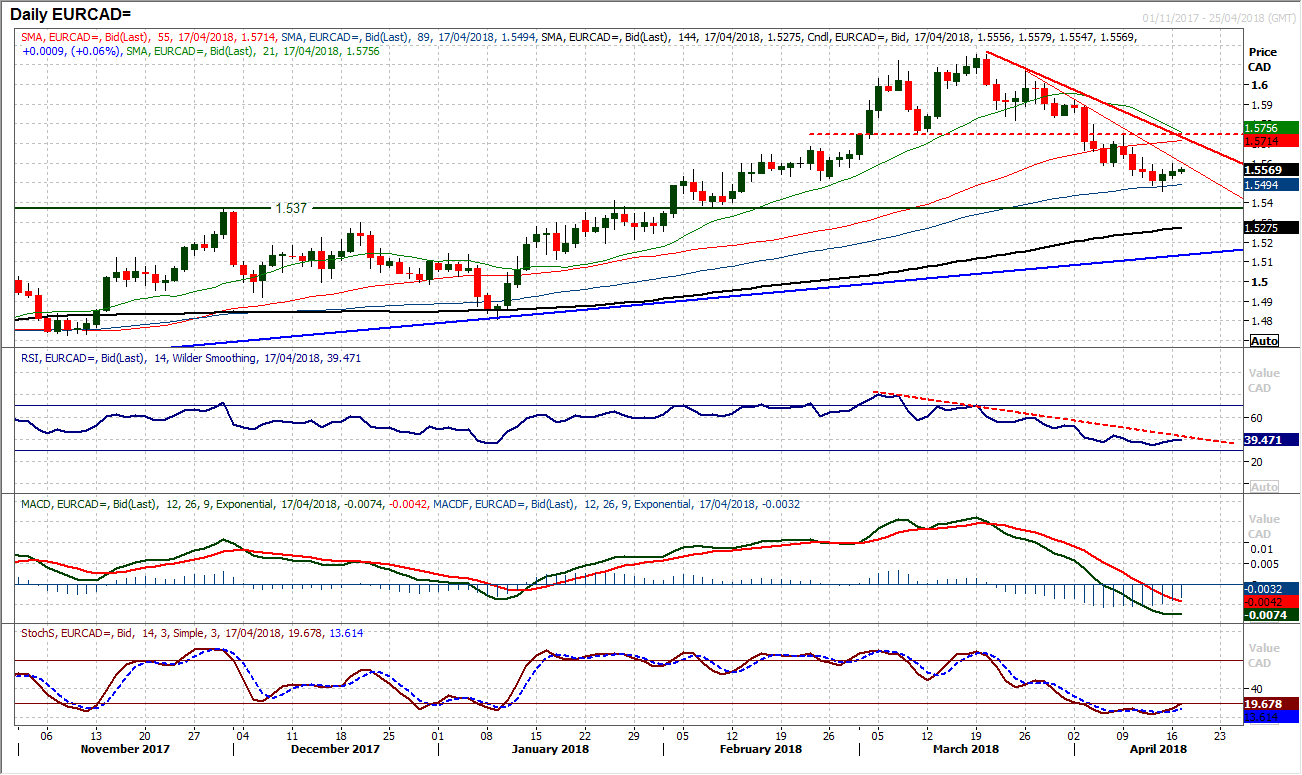

Chart of the Day – EUR/CAD

The mild bout of strength seen through the euro in the past couple of sessions could now give another opportunity to sell EUR/CAD. The market has been trending lower for the past four weeks with the trend seemingly accelerating. This is reflected in the trend lower on the RSI, whilst the MACD and Stochastics lines are all negatively configured. The reaction of the pair to this pick up in the last couple of sessions could now determine the near to medium term outlook. Since the top pattern completed below 1.5760 to imply a retreat to imply 1.5400 the market has posted a succession of lower highs and lower lows. Although the first key lower high is at the neckline of 1.5760 there is now a band of resistance between 1.5590/1.5760. This still looks to be a rebound within a multi-week downtrend. A sharper three week downtrend comes in around the 1.5590 resistance today and although a breach would suggest a minor recovery, the overhead supply built through the recent corrective phase is still likely to weigh on the rebound. Another lower high (within the four week downtrend which today comes in at 1.5730) can be expected somewhere between 1.5590/1.5760. Rallies are now seen as a chance to sell with Friday’s low at 1.5455 likely to be retested on the way to the target and likely retracement to the 1.5370 medium term pivot support.

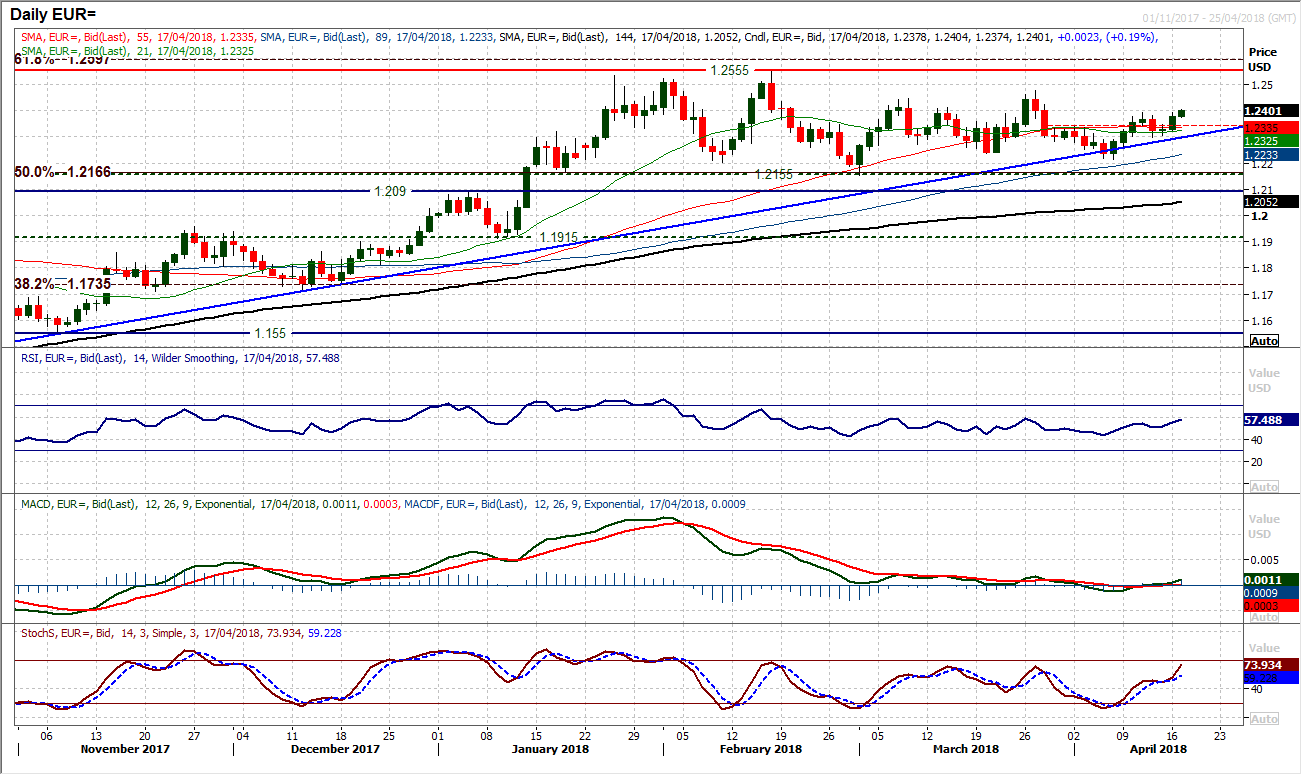

EUR/USD

The positive candlestick that added just shy of 50 pips on the day has just given the pair a slight bull bias once more within the medium term range. The move has pushed back above the moving averages and seen the momentum indicators tick slightly higher again. The initial resistance of last week’s high at $1.2395 is being tested and the market is rising in the upper half of the $1.2155/$1.2555 three and a half month range. A move above (especially with a close above) $1.2395 would open the March high of $1.2475. This improving outlook is also reflected on the hourly chart and intraday corrections are now being bought into. There is initial pivot support at $1.2345 and a higher low at $1.2300. However it is also important to point out that moves into the $1.2400s in March continually failed and although the technical picture may have picked up a touch in the past two sessions, the bulls still find upside traction hard to maintain.

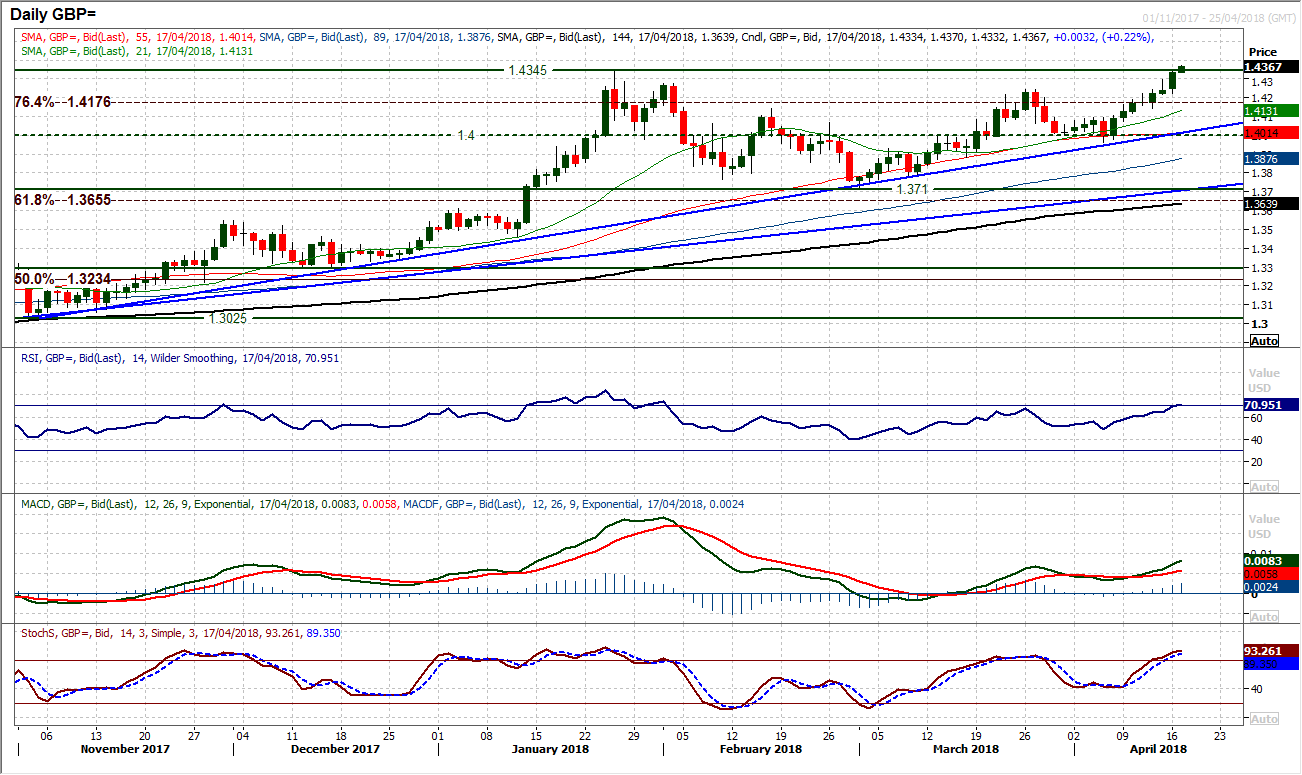

GBP/USD

Cable closed yesterday’s session at $1.4335 which was the highest closing price since 23rd June 2016, the day before Brexit. The move has also been maintained with initial gains this morning to move to an intraday multi-year high too. The momentum remains strong in this run higher and it certainly looks as though the market is busy pricing in a rate hike from the Bank of England at the next meeting in May. Looking at the RSI around 70, this is also well positioned and although seemingly stretched, perhaps not so in a strong trend (whilst the January strong trend spent around two weeks with the RSI over 70). The reaction to the key data points in the next couple of days could be key for the trend though. Today, UK wage growth will drive volatility and is the first big test with the market so strong. Initial support for a correction comes at the $1.4245 whilst there is a basis of support on the hourly chart around $1.4100. The hourly chart shows a strong uptrend channel which is supportive around $1.4260/$1.4280 today. Weakness into support is still a chance to buy. Continued moves above will find little real resistance until $1.5000 area.

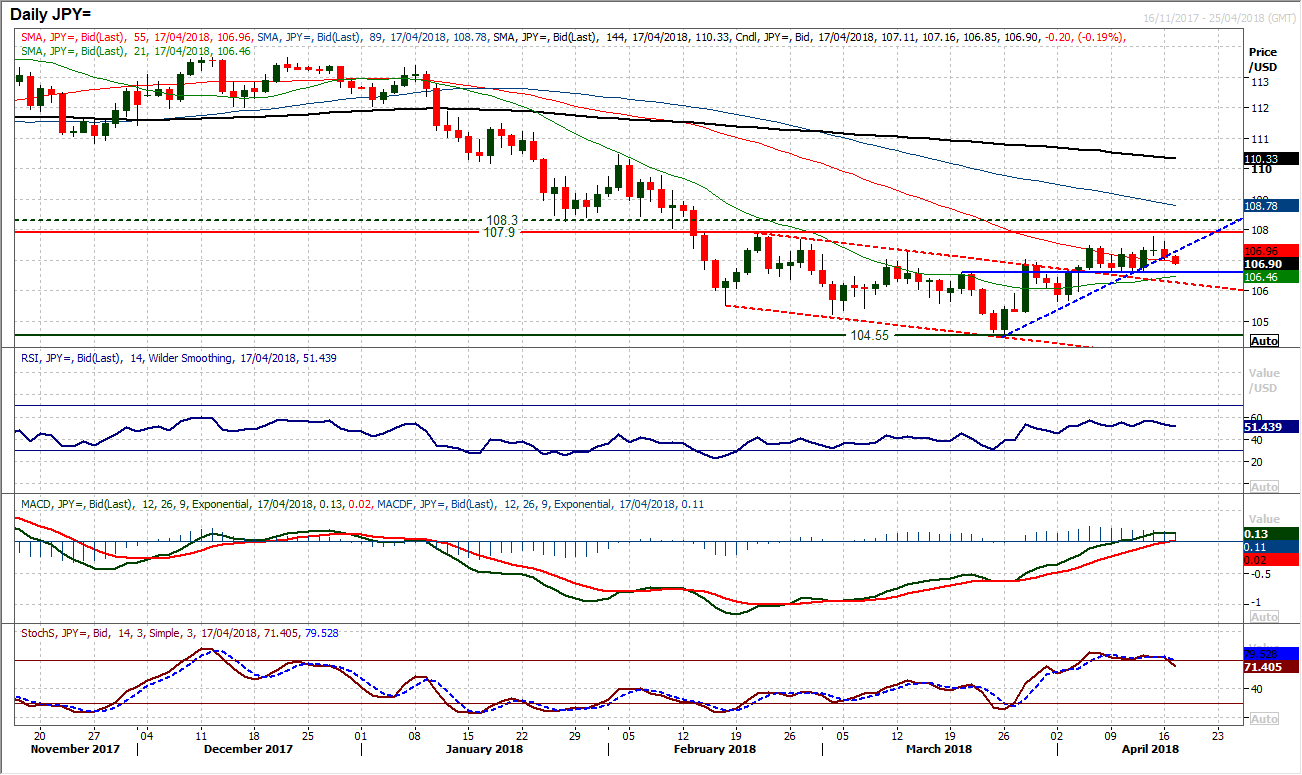

USD/JPY

Over the past week or so the bulls have made little ground and the impetus in the recovery has gradually waned away. Friday’s attempt to regain the initiative drifted back into a doji (denoting uncertainty), whilst yesterday’s negative candle is being followed up by early losses today. The uptrend of the past three weeks is being broken today, whilst momentum indicators are rolling over. The most concerning signal would be the Stochastics which if closed around here would be signalling a near term sell signal. However, whilst the support at 106.60 remains intact then the sellers would not be in control and this run would have to simply be seen as a consolidation rather than renewed pressure. Price moves are key to the development of the outlook now. Resistance remains strong between 107.50/107.90 but there is a floor at 106.60. The hourly chart reflects this ranging configuration, but with lower highs of the past couple of sessions a drift back towards 106.60 is becoming increasingly likely.

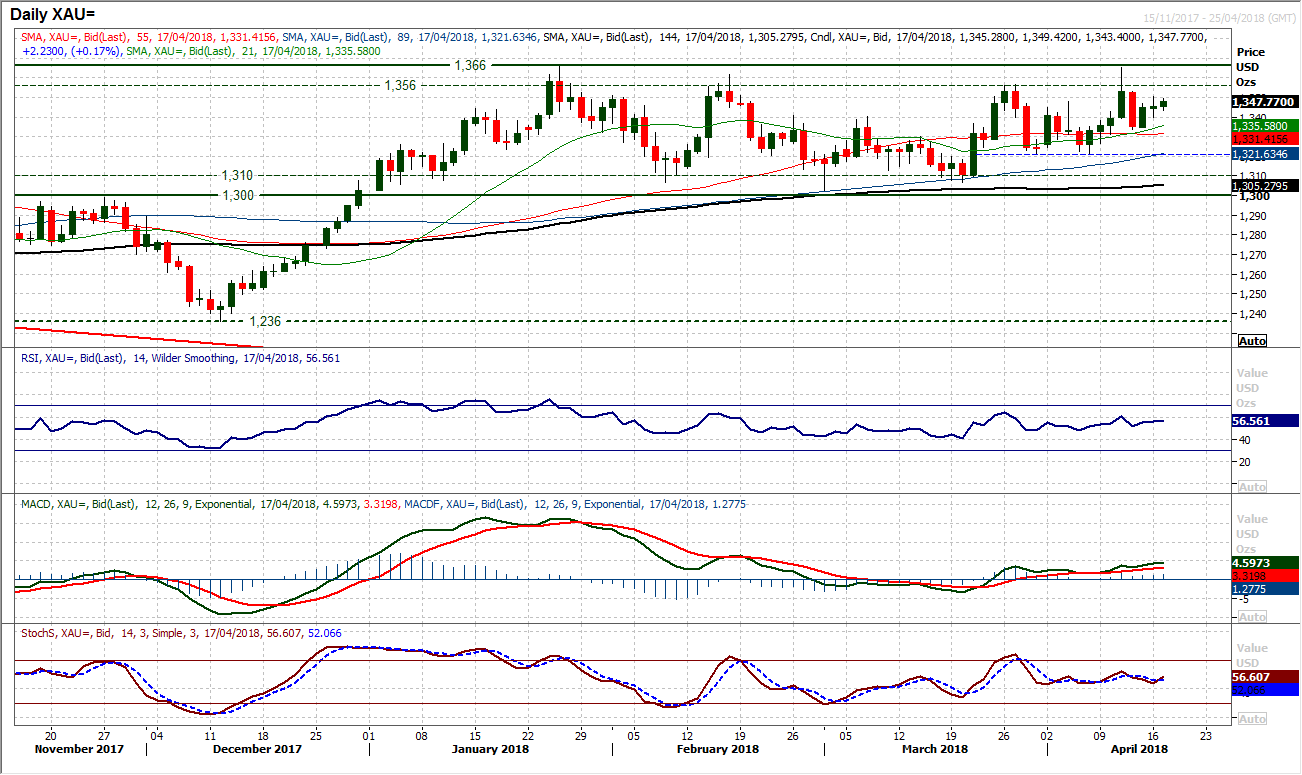

Gold

Although gold still has a mild positive bias there is still little upside traction that the bulls can sustain. Yesterday’s marginal positive candle followed by early consolidation today reflects this. The support at $1333.50 is a step above the mid-range support now in place at $1321 and trading above the moving averages lends a positive stance to the market which is reflected in RSI, Stochastics and MACD lines all marginally above neutral. However the bulls need to generate momentum to challenge the overhead resistance band $1356/$1366 and for now this is a struggle. The hourly chart shows initial support at $1340 from yesterday’s low.

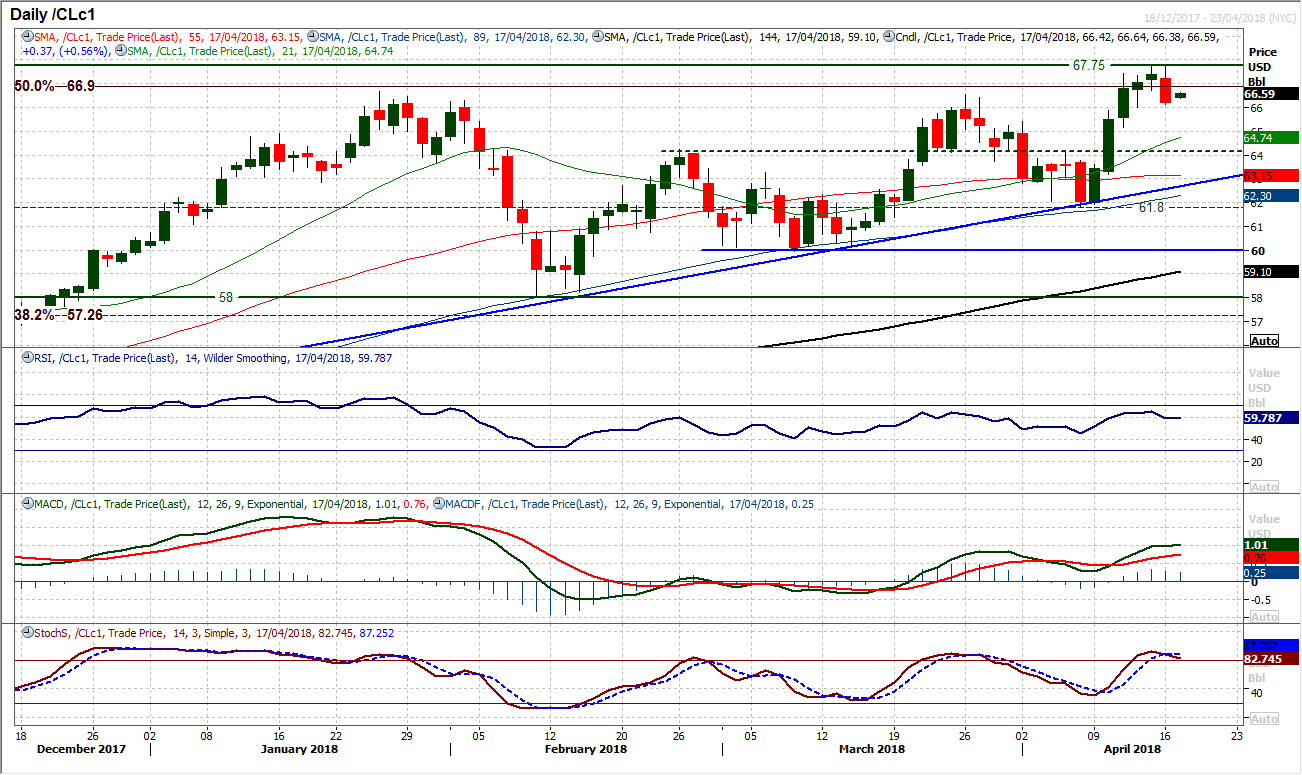

WTI Oil

The near term outlook for the continued push higher is questionable in the wake of the negative candle formed yesterday. However it was interesting to see that even though the impetus may have been lost from the rally, the selling pressure is failing to progress this morning. The initial resistance remains at $67.75 which is now preventing a continued move into multi-year highs and the close back below $66.65 is a disappointment. However the hourly chart shows the bulls holding up fairly well still and the market seems to be more in consolidation. The hourly chart also shows the importance of near term support at $66.00 as a move below would complete a small top and imply c. $1.75 of correction, which would be exactly back to the previous pivot band $63.75/$64.25. Corrections do though continue to be seen an opportunity and with the strength of the bull trends though this would be a chance to buy.

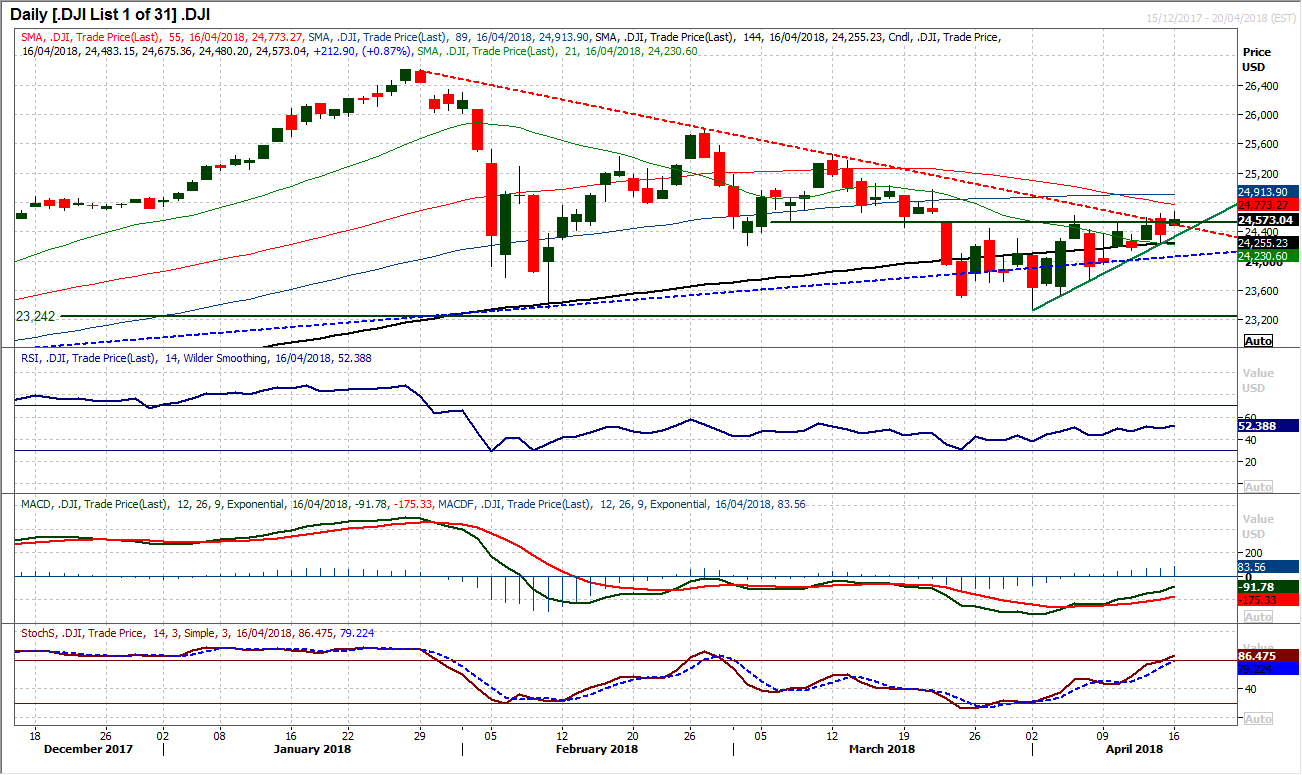

Dow Jones Industrial Average

Corrections in continue to be bought into as the pressure on the six week pivot range 24,450/24,650 continues to build. This also means that the resistance of the now eleven week downtrend continues to be tested and is increasingly close to yielding. The momentum of the two week recovery uptrend is building and if the market can close above 24,620 (but ideally above 24,650) then the bulls would be looking at a near term breakout. This would be a three week closing high which open the next resistance at 24,978 but also begin to bring the March high at 25,450 back into focus again. Momentum is increasingly positively configured with the MACD and Stochastics pushing strongly higher and the RSI building above 50. The hourly chart shows the importance of higher lows an 24,244 is the first basis of support now.

Author

Richard Perry

Independent Analyst