Steeper EUR curves from both sides

We see the landing point of the European Central Bank at 1.75%, reaching that level by mid-2025, but the path towards this may be bumpy. From the back end, EUR swap curves will feel upward pressure from higher UST yields, especially in the second half of 2025. Our forecast is therefore a further steepening of curves, more so than forwards imply.

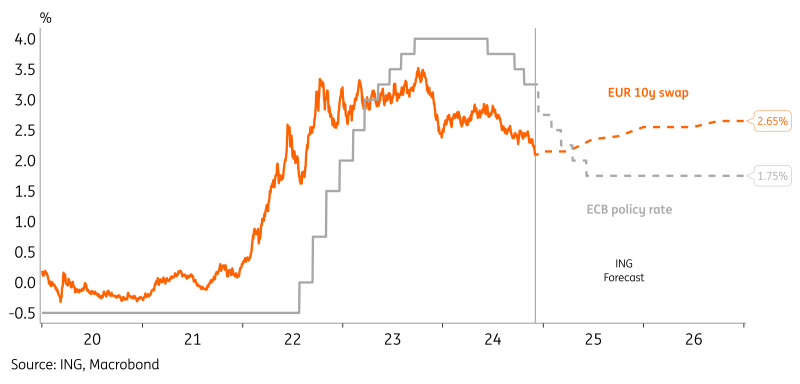

A bumpy ride down to the ECB’s landing zone

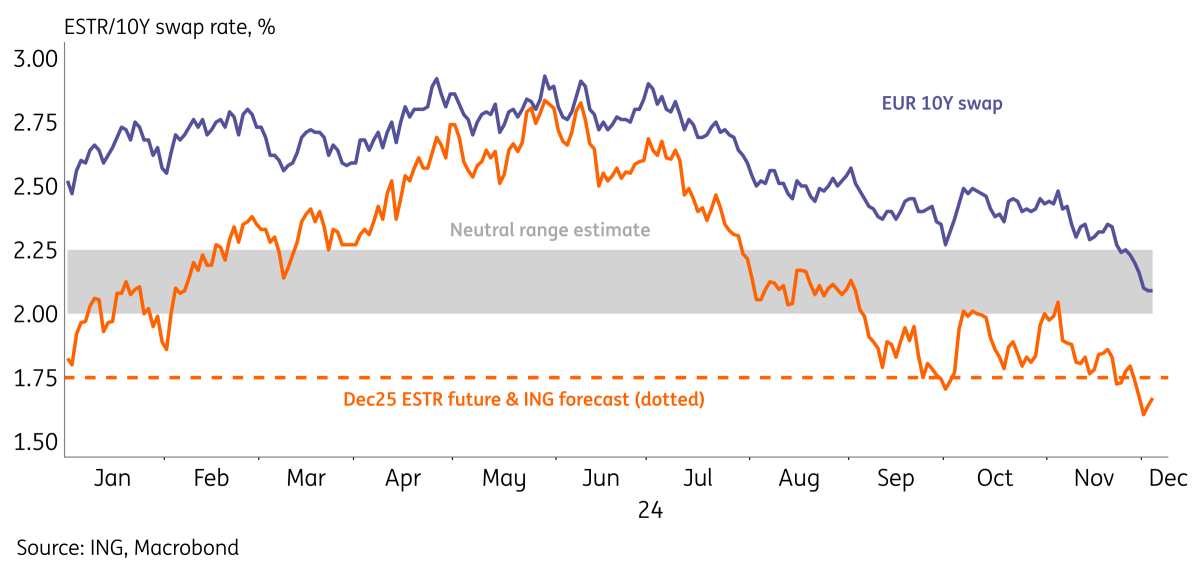

The key theme for EUR rates this year will be the ECB’s easing cycle, whereby the projected landing point will drive much of the moves. Throughout 2024, the 10Y swap rate was strongly driven by the market's expectation of where the ECB would settle in 2025. We think the ECB will cut just below our neutral range estimate of 2-2.25%, leaving us with a policy rate of 1.75%, in line with current market pricing.

The ECB’s willingness to ease supports an endpoint just below neutral

The path to reaching that terminal policy rate could be a bumpy one, as we see plenty of risks that may materialise. On the downside, we see recession worries and Trump-triggered trade tensions as the key risks. The ECB’s communication has turned more dovish as we enter 2025 and markets will thus be quick to turn any headwinds into more easing expectations. As an upside risk, we still have stubborn inflation numbers. In particular, wage growth could pose a challenge to the ECB.

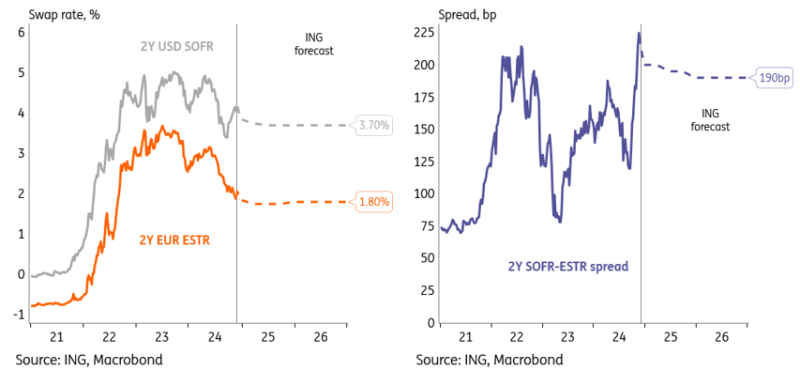

The 2Y EUR swap rate should find a floor at 1.75% in 2025, but we could see frequent undershoots as risk sentiment is challenged. The correlation with US rates on the front end of the curve should be less going forward and therefore we expect the USD-EUR 2Y swap spread to remain close to 200bp throughout the year.

Diverging outlooks means 2Y USD-EUR OIS spreads can remain wide

Our fair value of 10Y rates is above current levels

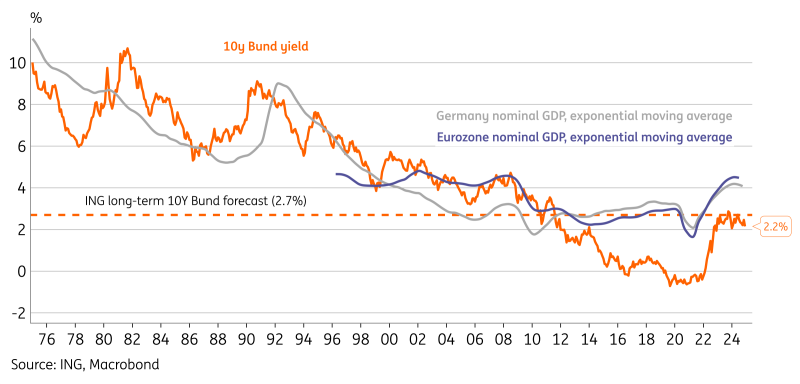

The 10Y swap rate should start settling closer to its long-term fair value as the ECB normalises monetary policy. As a very rough anchor for the fair-value estimate, we can look at the historical relationship of government bond yields with nominal trend growth. When plotting smoothened nominal GDP growth for Germany over a longer horizon, we can see a close alignment with the 10Y Bund yield. Since the introduction of the euro, eurozone GDP shows a better fit.

Fair value of 10Y rates as a function of trend nominal GDP growth

Based on our outlook on nominal growth, we think that 2.7% as the fair value of the 10Y Bund yield is justified, which is well above the current 2.2% level. When taking into account the Bund swap spread (more on that later), these estimates should roughly correspond to the 10Y swap. In our view, the period of low rates before Covid-19 was an exception rather than the new norm. Going forward, we see more political willingness to provide economic support through fiscal measures and we have structural drivers of inflation, including demographics, deglobalisation and decarbonisation. In effect, the return to the zero lower bound with QE is unlikely.

Steeper curves as part of the normalisation process

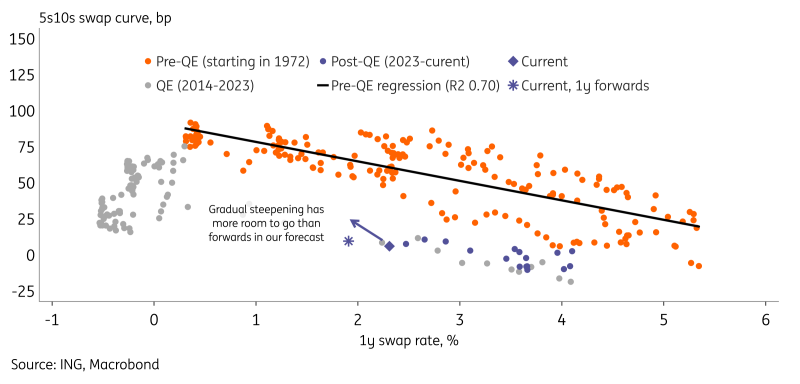

Curves have started steepening going into the ECB’s easing cycle and we think there is room for more. The inverted 2s5s and 10s30s remain an anomaly in historical terms and a normalisation of policy should help these into positive territory again. When looking at what forwards are pricing in, the 2s5s are expected to disinvert in 2025. Further out on the curve less movement is priced in, but we think markets are underestimating steepening potential here.

We see various structural drivers for steeper EUR curves in 2025. Firstly, supply pressures will remain high as QT continues and we foresee another year of high government bond issuances. Secondly, UST yields are expected to see significant upward pressure throughout 2025 and especially the back end of the EUR curve is still tightly linked to such global factors. Lastly, for longer-dated swaps, i.e. 30 years and beyond, we see lower structural demand from Dutch pension funds due to the upcoming reforms, which could put upward pressure on 10s30s.

Structural drivers should help curves steepen more than forwards

The risks to our baseline are tilted towards lower rates

Our baseline scenario sees the ECB settle at 1.75% and the 10Y Bund yield rise to 2.7% by year-end. We go into 2025 with fragile risk sentiment and the eurozone economy hasn’t bottomed out yet. That combination may lead markets to increase the chance of a return to a secular stagnation regime. One in which the ECB may have to cut to 1% or beyond, whilst QT is put on hold or even replaced by QE. If markets decide this is the path of least resistance, then the whole yield curve would grind lower and the 10Y Bund yield would find itself below 2%. That’s the downside risk case for rates.

On the other hand, the fight against inflation is not over and with wage growth still going strong, we could also imagine a scenario in which the ECB will not go into expansionary territory in 2025. Consumption-driven growth could pick up in mid-2025, as also predicted by the ECB, whilst trade tensions with the US may only materialise later in Trump’s presidency. In this case, the terminal ECB rate could reprice somewhat higher limiting the downside to rates.

In our baseline, 10Y EUR swap rates are dragged higher by the US

Read the original analysis: Steeper EUR curves from both sides

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.