Special FED day

Here we are. Today the FOMC will announce its decision on the interest rates at 19:00 GMT. And, to go straight to the point, this is possibly the last chance to trigger the long-awaited Christmas rally that could lead the major US indexes YTD performance in the green territory again.

As we have been reiterating in our reports, we have a bearish view on the stock markets going forward in 2019, and whatever the decision this afternoon this will not change our view. The world economy is on our opinion heading to a slow down whose magnitude is well beyond the forecasts published by the major world financial institutions which already revised their numbers to the downside as opposed to previous 2018 quarters. I am afraid that such revision to the downside will be reiterated in the quarters to come and the financial markets will follow suite.

Since Q1 we have been warning that the anticipated three interest rate hikes in 2018 would most probably be four. And the reasoning was basically based on the extremely expansive policies implemented by the Trump administration, namely the corporate tax cuts, which were put in place in an economy which was already in a very good shape, posting very good macro data and with an unemployment rate at a multi-decade low. The impact of such measures was obvious to us, leading to the risk of the economy overheating towards the end of 2018 and therefore forcing the FED to act aggressively to prevent such a scenario.

All the above still stands, and the consensus is for the forth 2018 rate hike to take place this afternoon., even if some discordant voices have emerged in the last hours. The latest movement of the stock market, the bond market and of commodities like Oil, are sending warrying signals to investors.

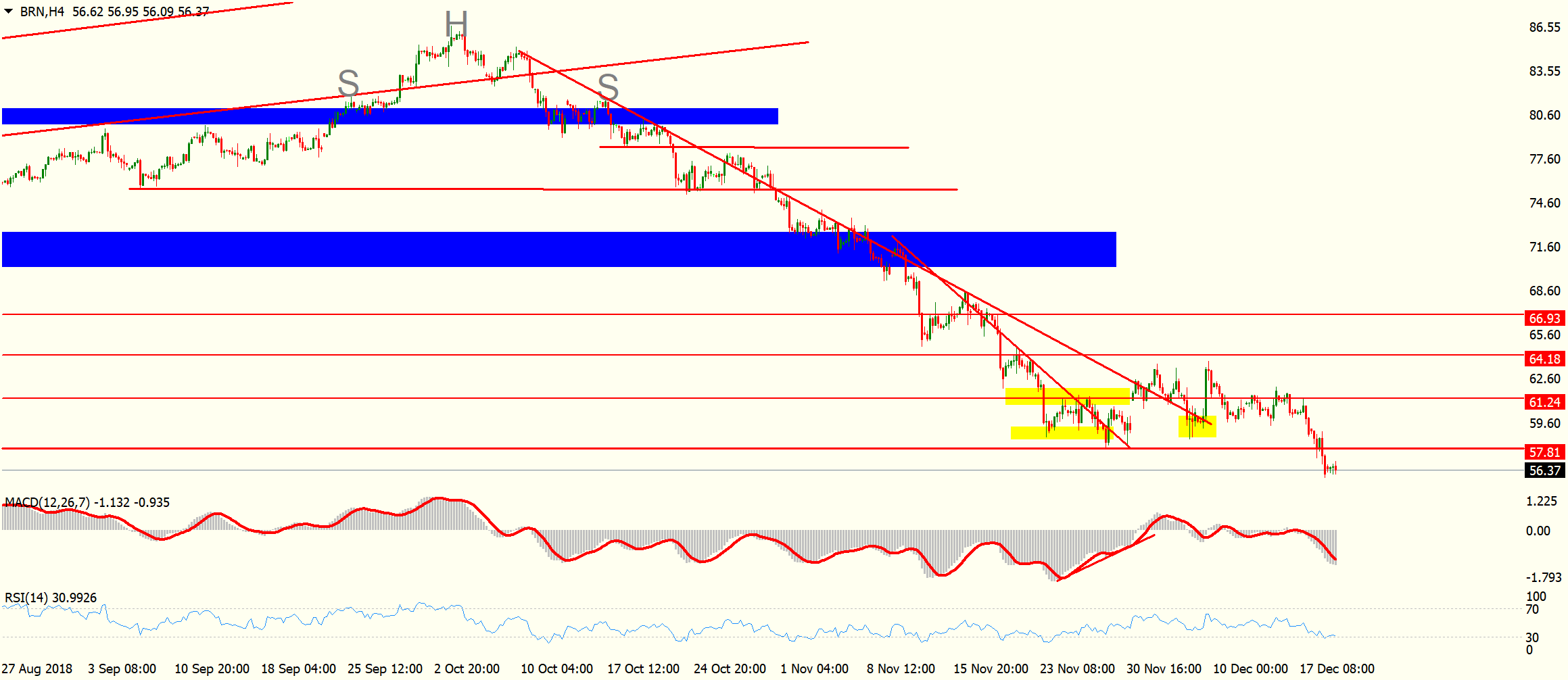

As you might remember, we underlined the yield curve inversion on short term maturities and the possibility of Oil prices to continue their downside movement notwithstanding the production cuts decided by OPEC earlier this month.

Here is the Brent chart for your reference:

It is all reflected in the stock market prices. Last week was yet another negative one: --1.2% on the week on the DJIA, which brings the performance YTD to -2.5%. Same situation with the S&P500 and the NASDAQ: -1.3% weekly, -2.8% YTD and -0.8% weekly, +0.1% YTD respectively. The Russel 2000, which we mentioned to be a clear indicator if the future expectation of the institutional investors: -2.52 weekly, -7.1% YTD.

The week started in negative territory, with some sort of a rebound only today.

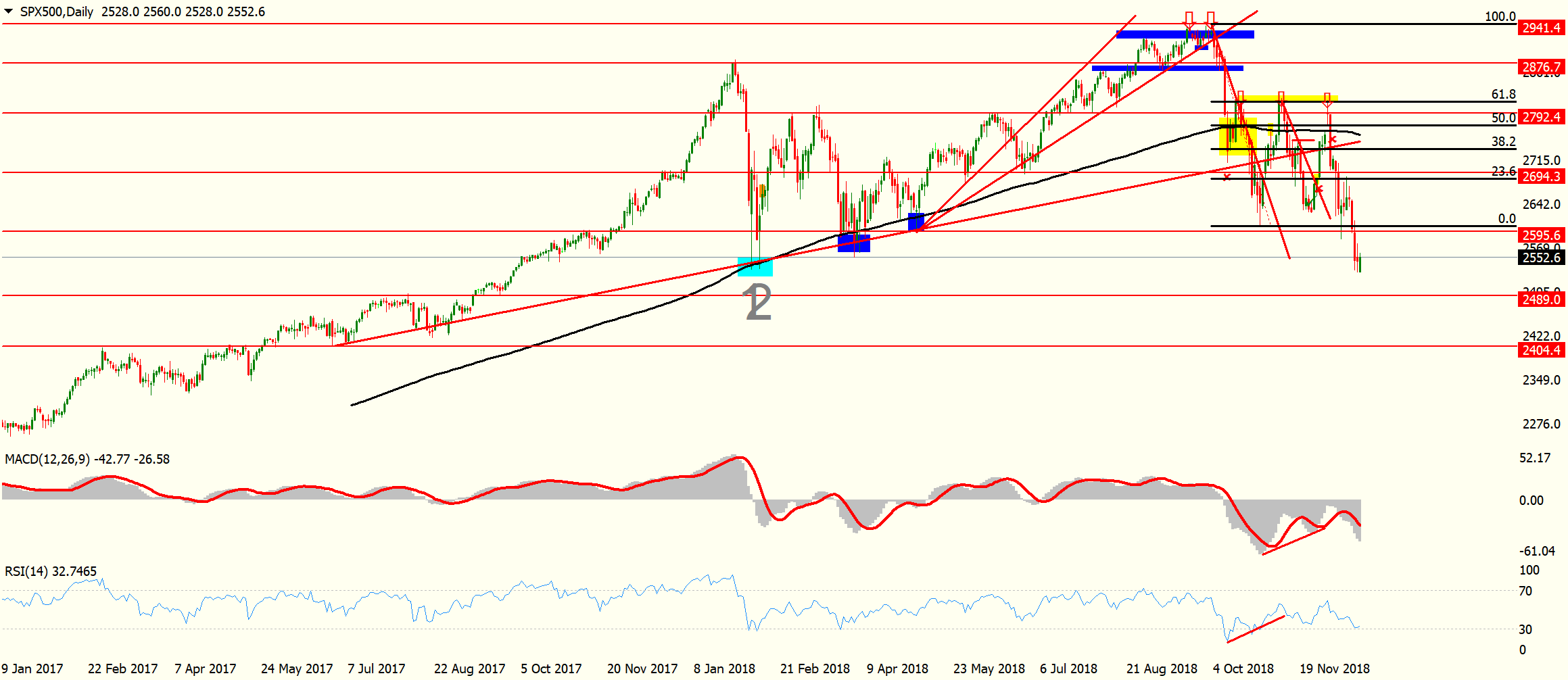

Here is the situation on the S&P500:

The situation is not good for this index (but the DJIA and the NASDAQ really do not look that different). That double top was successfully tested and the base of the rectangle broken. That means a theorical target at 2400 points!

The delicate situation, along with President Trump pressure on the FED to avoid raising rates, has shifted some analyst’s view toward a pause in rate hiking starting the upcoming FOMC meeting.

While it is true that in general terms rates being kept at the present level should be good news for the stock market, it is also true that such a move could also be signalling a loss of confidence on the FED side on the future course of the economy, thus triggering an opposite reaction from investors that might think to trim their exposure reducing the equity stake of their portfolio.

I still think that, short term volatility aside, the tendency is to the downside, as I believe a stronger than expected slowdown will impact the Global Economy. As I said in my interviews with mainstream media, there is a finite number of bad news markets can sustain, especially after an exceptionally long period of monetary stimulus that is now fading away, and that mark has probably been passed.

One of the outcomes of this meeting could be that of confirming the rate hike while presenting a more dovish stance on the future moves. That could calm the market towards the year’s end and have a bearish impact on the Greenback.

In its situation against the Euro, the USD could lose ground as a result of such stance by the FED, that could be amplified if there will be a confirmation of the rumors regarding the latest version of the Italian budget being accepted by the EU officials, which would avoid the infraction procedure to be triggered, easing the standoff which has been ongoing since September.

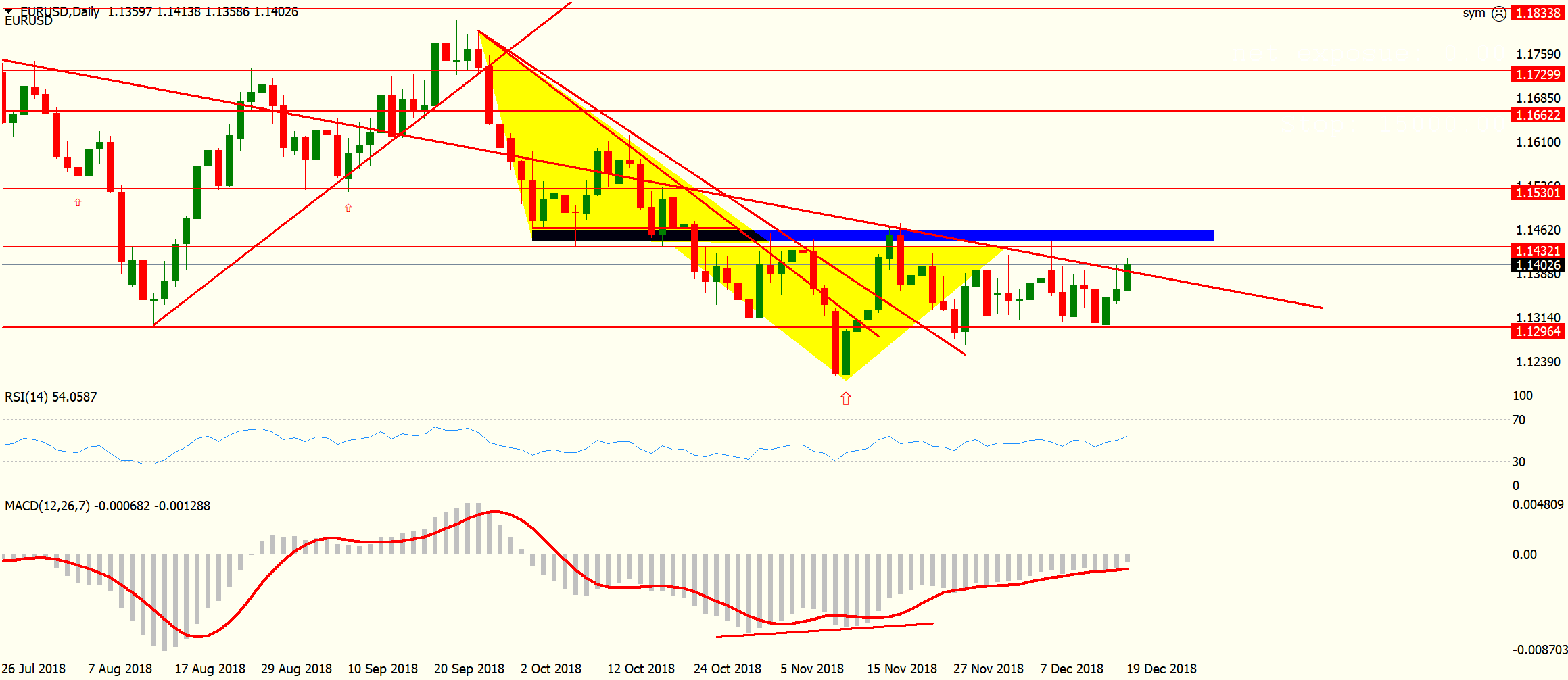

Here is the situation with the cross:

We are again in a situation in which indicators are signalling a possible revers, and the in the eve of the FED announcement investors are pricing in the possibility of an USD being impacted negatively by Powell’s statement.

We are a few hours away from the announcement.

Brace for volatility and manage your exposure appropriately!

Author

Roberto d´Ambrosio

Alpari Research & Analysis Ltd

Roberto has over 15 years’ experience in Financial Services starting as a proprietary trader.