S&P 500: A bounce up coming?

Stock bulls remain on the sidelines as money continues sloshing around and Wall Street awaits the latest updates on U.S. inflation.

Fundamental analysis

The Consumer Price Index today is expected to show a +0.2% increase for April, following a +0.6% jump in March. Since last July, CPI increases have averaged a gain of +0.3% a month, bringing the year-over-year increase up too +2.6% in March. That's expected to jump to +3.6% in the April read.

Keep in mind, last year's comparison numbers reflect huge pandemic-induced declines for everything from restaurants and hotels to auto insurance and medical care.

In addition, energy costs, which factor into almost all consumer goods, were sharply lower last year. Inflation pressures coming from the labor market side of things continue to fuel headlines, as well.

The Labor Department's JOLTS report yesterday showed job openings reached a new record high of 8.1 million at the end of March after climbing by +600,000 during the month.

Fed Chair Jerome Powell and other officials have said repeatedly that the current trend of price increases is a limited phenomenon, attributable largely to the base effect from last year's lockdown as well as lingering pandemic impacts to supply chains and labor markets.

A big worry is that these inflationary pressures last longer than anticipated and begin driving up analyst inflation expectations, which could in turn lower the outlook for both earnings and economic growth.

Most on Wall Street have targeted the Federal Reserve's September meeting for officials to begin making a case for tapering back its asset purchases. However, some analysts think "taper talk" could come as soon as June, particularly if inflation continues to run above the Fed's target rate of +2% and we see a rebound in job gains.

Several Fed officials are scheduled to speak today including Federal Reserve Vice Chair Richard Clarida. On the earnings front, highlights today include Compass, Sonos, Tencent, and Wendy's.

The U.S. Energy Information Administration (EIA) is also set to release its weekly Petroleum Status Report today, which will likely draw extra attention following the shutdown of the Colonial Pipeline. The company says it is back in "full operational control" but doesn't anticipate being back online until the end of the week. From then, it will take about 15 days to get gasoline from refining hubs on the Gulf Coast to the East Coast, while jet fuel and diesel take approximately 19 days. There are already reports of gas stations running out of supplies, partially due to consumers rushing to fuel up ahead of anticipated shortages.

The pipeline runs from the Texas Gulf Coast to the New York metropolitan area. The states most dependent on the pipeline include Alabama, Georgia, Tennessee, and the Carolinas, but the shock is also being felt further north into states like New York and even Vermont. One Washington, D.C.-area fuel distributor told reporters that “catastrophic” shortages are looming.

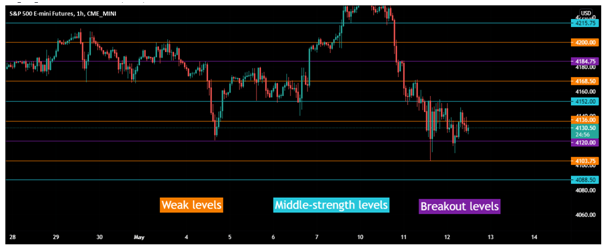

Technical analysis

Despite the recent sell-off, we don’t have any swing signals in SP500. Based on weekly closing, I will publish a more detailed outlook. For today the neutral zone is 4120 - 4184.25. Middle strength level within this zone - 4152, weak levels - 4136 and 4168.25.

If price sustains below 4120, look for 4104 (weak level), 4088 (middle-strength level), and 4072 (weak level). Holding above 4184.25 should be considered a bullish breakout. In that case, look for 4200 (weak level) and 4216 (middle-strength level). The reminder mentioned levels should offer support/resistance before you consider a trade. Also, I want to pay your attention to extremes in panic selling indicators that might indicate a coming bounce up.

Author

Inna Rosputnia

Managed Accounts IR

Inna Rosputnia is a stock and futures trader, portfolio manager and financial analyst that has been in the trading industry for the last 12 years.