Solid US eco data to end corrective bond gains?

Yesterday's trading session on core bond markets resembled the one on Monday. Risk sentiment on stock markets continues to be hesitant with main indices having trouble to reach fresh highs on a daily basis the way they did in October/early November. Add the fact that both the German (-0.25%) and US 10-yr yield (1.94%) failed to take out resistance levels and the two-day corrective bull steepening is a fact. There's nothing better-than-expected German Q3 GDP data (0.1% Q/Q; avoided technical recession) could do to change that. German yields fell by 1.7 bps (2-yr) to 6.6 bps (30-yr) on a daily basis. Changes on the US yield curve varied between -4.5 bps (2-yr) and -6.7 bps (30-yr). Peripheral yield spreads vs Germany widened rather significantly for a second straight session: Italy (+13 bps), Greece (+11 bps), Portugal (+7 bps) and Spain (+6 bps). Asian stock markets gain up to 1% this morning with China (-0.5%) underperforming. The German Bund and US Note future lose ground. Moves in Japanese government bonds also suggest an end to the correction of past days. Most recent US-Sino trade comments were more upbeat with White House economic advisor Kudlow saying that negotiations were coming down to the final stages.

Today's eco calendar heats up in the US with October retail sales, October industrial production and the November Empire Manufacturing Survey. Retail sales will hijack most attention. Consensus expects 0.2% M/M growth in the headline number, which might be overrated because of dwindling car sales. However, the report should be able to pass the 0.3% M/M consensus bar for the core reading following flat growth in September. Overall, we believe that US eco data should underpin the hypothesis that US economic data will start to recover and the Fed's case that three rate cuts are sufficient. It should help put and end to core bond's corrective rally. Risk sentiment on stock markets remains a wildcard. Our base scenario still expects phase one of the US-Sino trade deal to be sealed before the end of the year.

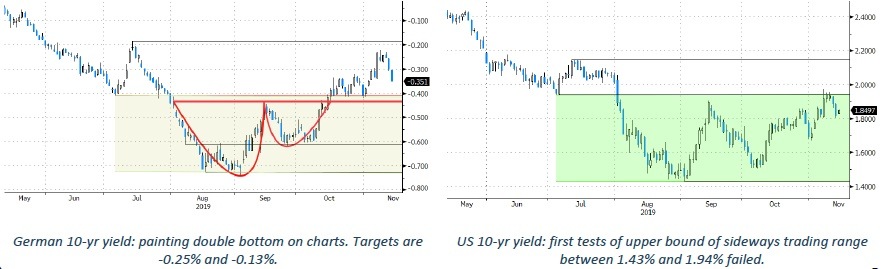

Technically, the German 10-yr yield and US 10-yr yield both rebounded away from August lows following ECB/Fed September policy meetings. The German 10-yr yield broke above -0.41% resistance as geopolitical uncertainty diminished, improving the technical picture. Targets of this double bottom formation are -0.25% and -0.13%. The 38% retracement level of the Oct-Aug decline stands at -0.24%. The US 10-yr yield trades in the 1.43%-1.94% sideways trading channel. Recent tests to take out 1.94% failed, causing corrective return action lower.

Author

KBC Market Research Desk

KBC Bank