Silver's squeeze has unwound, but the shortage has not

Silver's late-2025 squeeze has quietly unwound, and the vault rebuild looks like the bull case breaking, but the sixth straight annual shortage beneath it all hasn't budged

Silver sits near $60 an ounce as I write this, after a sharp correction that has cut its price roughly in half since January. The metal is down about 51% from the January 29 high of $121.62 and roughly 15% below its end-2025 close near $71, even though it remains well above where it traded a year ago. The move has been monetary at its core: a hawkish Federal Reserve under new chair Kevin Warsh and a dollar pushing to one-year highs. The 2026 Iran war weighed on silver rather than lifting it: the inflation it drove kept the Fed hawkish and the dollar firm, and a higher expected rate path raises the cost of holding a metal that pays no yield, the reverse of the safe-haven bid a war is assumed to bring.

Underneath the price, a quieter story has been unfolding in the warehouses. Through late 2025, the defining feature of the silver market was a paper-versus-physical squeeze: exchange inventories were draining, the cost to borrow physical metal spiked, and headlines warned of a delivery crisis. That stress has now broadly resolved across the Western trading hubs. The natural reading is that the physical bull case has broken along with it.

In Golden Meadow®’s Silver Catalyst Newsletter, the lens I apply is structural rather than week-to-week, and the structural picture has not moved the way the price has. The vault rebuild is real, but it is not the same thing as the shortage ending.

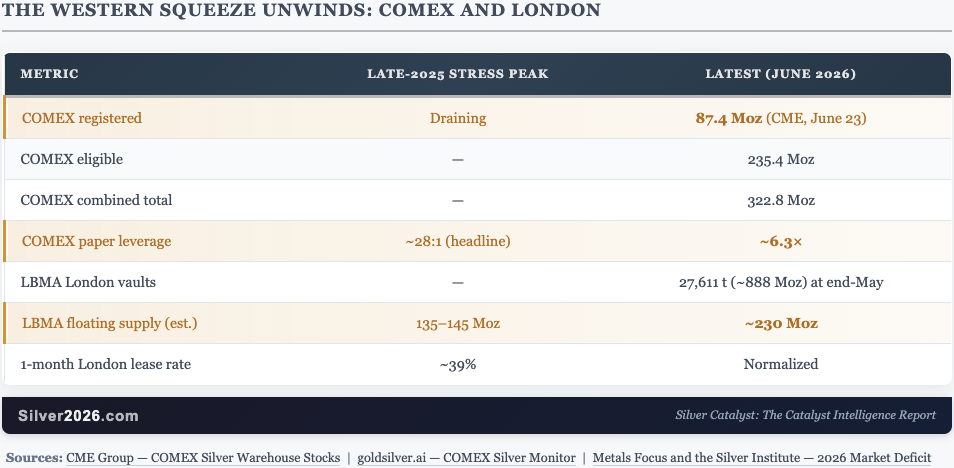

The western squeeze has unwound

Start with COMEX, the New York futures exchange that publishes its warehouse data every day. Registered silver, the metal actually pledged against futures contracts and available for delivery, has rebuilt to 87.4 million ounces as of June 23, up from near 82 million earlier in the month. Eligible silver, the larger pool that sits in approved vaults but is not pledged for delivery, stands at 235.4 million ounces, for a combined total of 322.8 million ounces. The deliverable pool is expanding, not draining.

The mechanism matters, and the latest report spells it out. The single-day jump in registered metal on June 23 came almost entirely from a reclassification of roughly 1.2 million ounces out of eligible and into registered, not from new bars arriving at the vault. Owners are moving existing metal into deliverable status ahead of the July delivery cycle. That signals supply readiness, but it is not fresh metal entering the system.

The leverage picture has normalized in parallel. At the height of the late-2025 stress, commentators cited a paper-to-physical ratio of roughly 28 to 1, implying 28 ounces of futures claims for every ounce of deliverable metal. Live monitors now put that figure near 6.3 times, a fraction of the dramatized headline. In plain terms, the futures market is nowhere near as thinly covered by deliverable metal as the squeeze narrative implied.

London tells the same story. The London Bullion Market Association reported its vaults holding 27,611 tonnes, roughly 888 million ounces, at the end of May, a small monthly increase. More importantly, the floating supply, the portion of London metal not already committed to exchange-traded funds and long-term holders, has rebuilt toward 230 million ounces from the 135 to 145 million ounce trough at the October 2025 stress peak. The one-month lease rate, the cost to borrow physical silver, spiked toward 39% at the height of the squeeze and has since normalized. When that borrowing cost falls back to ordinary levels, it means the scramble to source physical metal has eased.

Sources: CME Group — COMEX Silver Warehouse Stocks | goldsilver.ai — COMEX Silver Monitor | Metals Focus and the Silver Institute — 2026 Market Deficit

What this means to Silver investors

The honest read is that the unwinding of the squeeze removes one of the cleaner near-term arguments for higher silver prices. A market where vaults are draining and lease rates are spiking carries an obvious urgency. A market where vaults are rebuilding and lease rates are calm does not. Saying so plainly is a matter of credibility.

But the squeeze was never the structural case for silver, and the two should not be confused. A short squeeze is a stock problem, a temporary shortage of metal in the right place at the right time. The deficit is a flow problem: every year, the world consumes more silver than it produces. For 2026, Metals Focus and the Silver Institute project a market deficit of 46.3 million ounces, the sixth consecutive annual shortfall. Visible inventories can rebuild for a stretch even while that deficit runs, because above-ground stock can be reclassified, relocated, or drawn down slowly. The squeeze left. The deficit did not.

The physical tightness has not gone away either. It has only moved east. While Western inventories rebuild and retail premiums in the United States collapse toward spot, physical silver in Shanghai continues to command a premium of roughly 10% or higher over the Western benchmark. That divergence survived the global price correction, which points to genuine physical tightness in the East rather than a leftover feature of the late-2025 squeeze.

For an investor, the takeaway is to separate the two clocks. The near-term clock is set by the Fed and the dollar, forces that move every rate-sensitive asset and have little to do with silver's own supply and demand. The longer-term case for silver rests on the structural deficit, the rigidity of mine supply, and the persistent Eastern premium, none of which the vault recovery has touched.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Przemyslaw Radomski, CFA

Gold Price Forecast

Przemyslaw Radomski, CFA (PR) is a precious metals investor and analyst who takes advantage of the emotionality on the markets, and invites you to do the same. His company, Sunshine Profits, publishes analytical software that any