Silver's Mexico problem: A fifth of supply, reviewed every year

Washington declined to renew the trade deal covering Mexico, the country that mines a fifth of the world's silver, and the pact now goes to review every year instead of being locked in for another sixteen, without a single ounce moving.

Silver trades near $57 today, unable to crack $60 as US airstrikes on Iran run into a fifth day and the Strait of Hormuz stays closed. The metal is down roughly 20% from where it closed 2025, near $71, and it sits about 53% below the all-time high of $121.62 set on January 29, though it remains up roughly half from a year ago. Against gold near $4,030, the gold-silver ratio is about 71. The route from a Middle East war to a lower silver price is not the obvious one. It runs through inflation: higher oil revives price pressure, a Federal Reserve that may have to stay hawkish lifts real interest rates, and silver, which pays no interest, gets sold. This is a monetary story, not a verdict on silver's own supply and demand.

Underneath that price, the structural picture has not changed. The market is on track for its sixth consecutive annual deficit, forecast at 46.3 million ounces for 2026 by Metals Focus and the Silver Institute, meaning the world is set to use more silver than it produces for the sixth year running. What moved in the last two weeks is the policy wrapped around that supply. Two things happened in Washington, neither of them about silver, and both touch the ground silver comes from. This is the kind of development the Silver Catalyst newsletter I publish through Golden Meadow® tracks issue by issue, and it is worth reading against how silver has traded in 2026.

Washington puts North American trade on a yearly clock

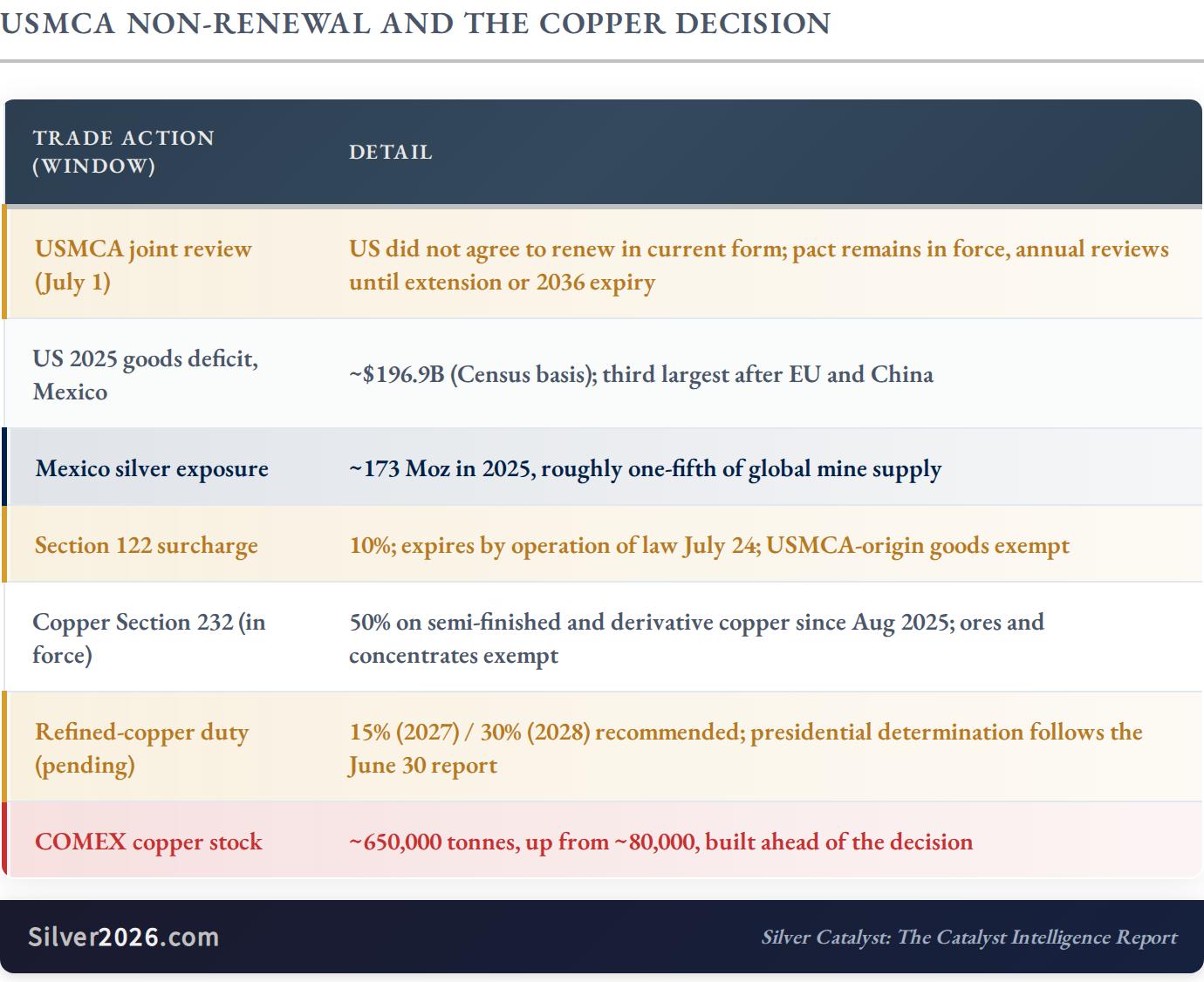

On July 1 the three governments held the first mandatory joint review of the USMCA, the North American trade agreement, on its sixth anniversary. The review asked one question: would all three confirm an extension for a further sixteen years? The United States said no. In the words of US Trade Representative Greer, it "did not agree to renew the USMCA in its current form." Mexico and Canada both supported extending it.

It is worth being precise about what that did and did not do, because the headlines were louder than the event. Nothing expired. The agreement remains fully in force and its own terms run to July 1, 2036. What the refusal triggered is the fallback written into the treaty: instead of a settled sixteen-year extension, the three parties now hold a joint review every year until they either agree to extend or the agreement lapses in 2036. The extension remains available at any time if all three sign off. So exporters did not lose access; they lost certainty. And the bargaining is live, with Washington pressing for stricter rules of origin and a further round with Mexico set for the week of July 20.

Greer tied the refusal to the agreement's shortcomings and to US trade deficits with the two countries. He attached no figures to it. The official data do: the US goods deficit with Mexico ran $196.9 billion in 2025 on a Census basis, behind only the European Union and China.

For silver, the address matters more than the arithmetic. Mexico is the world's largest silver-producing country, at 172.9 million ounces in 2025 according to Metals Focus and the Silver Institute, ahead of Peru at 130.6 million and China at 112.8 million. Against global mine production of 846.6 million ounces, that is roughly one ounce in five. Putting that jurisdiction's trade terms on a yearly cycle closes no mine and cancels no shipment. It does mean the largest single slice of the world's silver now sits under a question reopened every twelve months instead of every sixth year.

A second clock runs alongside it. The 10% import surcharge imposed under Section 122 in February reaches its 150-day statutory ceiling on July 24 and expires automatically, since only Congress can extend it. Properly claimed USMCA-origin goods were exempt from that surcharge in any case, which is exactly why the agreement's status is worth watching: an exemption is only as durable as the framework behind it.

The Copper decision that has not been made

The second development reaches silver through a side door, and it has not actually happened yet. Roughly three-quarters of the world's silver is never mined on purpose. It surfaces as a byproduct of digging for copper, lead, zinc, and gold, which makes copper policy into silver policy at one remove.

Since August 2025, semi-finished copper products and copper-intensive derivatives have carried a 50% tariff. Copper ores, concentrates, cathodes, and anodes, which are the forms byproduct silver actually travels in, were deliberately left out. The same proclamation directed Commerce to report on the domestic copper market by June 30, 2026, so the President could determine whether to impose a phased duty on refined copper of 15% from January 2027, rising to 30% from January 2028. That report has now fallen due and the decision sits with the President. It is genuinely contested: a duty on refined copper protects domestic refiners while raising costs for every US manufacturer that buys the metal.

The market has not waited for the answer. COMEX copper inventories have climbed from roughly 80,000 tonnes to about 650,000 as traders moved metal inside the tariff wall ahead of the decision.

Sources: USTR — Greer Statement on USMCA Joint Review | White House — Proclamation 10962, Adjusting Imports of Copper Into the United States | BEA — US International Trade in Goods and Services, Annual 2025 | Trade Law Counsel — Section 122 Surcharge Sunsets July 24 | Congressional Research Service — Section 232 National Security Tariffs on Copper Imports | TradingKey — COMEX Copper Inventories Hit Record | Metals Focus and the Silver Institute — World Silver Survey 2026

What this means to Silver investors

Start with what did not happen, because it is most of the story. No ounces were removed. The USMCA is in force, Mexican silver still crosses the border, and an annual review is a process change, not a tariff. The refined-copper duty has not been decided at all, and the copper measures that do exist specifically exempt the ores and concentrates that carry byproduct silver. This is a change in the terms silver travels under, and for now only a possible one.

What it does is add friction and a standing risk premium to the ounces the market most needs, on top of a balance that is already short. That is worth watching precisely because it is slow. There is no announcement day for it and no headline saying supply fell. It shows up as a wider gap between where silver is mined and where it is used.

The honest counterweight deserves full weight. The survey itself expects Mexican production to return to growth in 2026, after falling three years running, including a 5% drop in 2025. So the jurisdiction now under the annual clock is the one part of supply that may actually improve, and trade friction and mine output are different things. The first does not automatically damage the second.

Where it lands is alongside the rest of the policy squeeze. In Issue #19, I discussed the split between a rebuilding New York vault and a rising Shanghai premium, with Beijing narrowing its export valve at the same time. Put them together and the supply chain feeding a 46.3 million ounce deficit is being handled at both ends by governments, for reasons that have nothing to do with silver and cannot be undone by its price. None of this points to a level on the chart, and I would be wary of anyone who says it does. The longer-term case for silver rests on a structural deficit and a supply base that cannot easily grow, and policy keeps adding to the cost of reaching that base.

Want free follow-ups to the above article and details not available to 99%+ investors? Sign up to our free newsletter today!

Author

Przemyslaw Radomski, CFA

Gold Price Forecast

Przemyslaw Radomski, CFA (PR) is a precious metals investor and analyst who takes advantage of the emotionality on the markets, and invites you to do the same. His company, Sunshine Profits, publishes analytical software that any