The markets are getting crazy

Both gold and oil are trading down in the last days. Oil prices are behaving as if the Iran-US peace deal is still possible, while gold is falling due to the Fed's rather hawkish stance. However, investors’ behavior is fully illogical. In this article, I will explain why.

Three scenarios

If any form of the US-Iran peace deal is likely in the near future, then oil prices should fall further, dragging down inflation and making the Fed and other central bankers dovish. If that happens, both gold and silver prices should be soaring, not falling.

If there is no peace deal in the near future, given the latest conflict outbreak, which is my base-case scenario, then oil should be trading much higher. This should make central bankers hawkish, thus pressurizing precious metals' prices in the near future.

However, another scenario is well possible as well, namely that of the 1970s coming back in the near future. The decade was marked by high oil prices; stagflation—high inflation and unemployment; higher interest rates; and soaring prices for precious metals. There are at least two similarities to the current situation. The 1970s inflation was due to oil shortages caused by the 1973 Arab oil embargo and the 1979 Iranian Revolution. When Paul Volcker took office in 1979, the Fed drastically raised the interest rates, thus provoking a severe recession. A similar situation might be about to happen now.

The US-Iran deal is highly unlikely in the near future.

There have been discussions that Israel and Iran would eventually reach a compromise. However, it is very hard to force the sides to the deal, namely Iran and Israel, to fulfill all the conditions. There are indeed important questions that it is impossible to reach a compromise on. The first and foremost is the nuclear enrichment that Iran cannot abandon and Israel cannot accept. Then, there are Lebanon attacks on Hezbollah carried out by Israel that Iran cannot accept. Also, Iran insists on reparations Iran also demands that Israel and the US pay reparations. by Israel and the US. The US and Israel find this condition humiliating and would never agree to it.

Why gold would soar anyway

So, based on what I have mentioned above, the peace deal is highly unlikely, which is great for the oil prices but horrible for inflation statistics.

But even though the situation should pressurize the gold prices in the near future, in the long run, this should lead to an even more brilliant rally in the mid-to-long term. Higher rates lead to economic downturns the way it was in 2008. The Fed had to take unprecedented measures to get the economy going. This obviously involved excessive money printing, which lifted the gold prices. The same situation should repeat itself now.

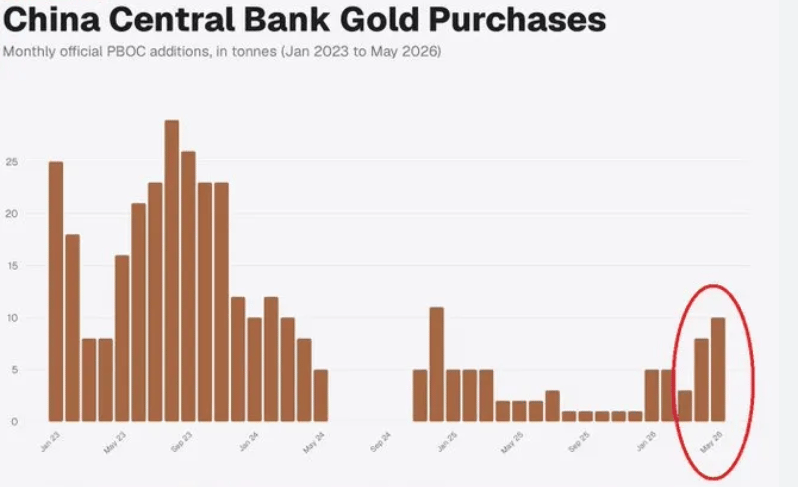

Moreover, central bankers are actively buying gold, most notably the People's Bank of China. In fact, the People's Bank of China has reached two-year record highs in terms of gold purchases. China’s central bank has been raising its gold purchases for 20 consecutive months. As reported by VN Express, China’s central bank raised its gold reserves for a 20th straight month in June, adding 480,000 troy ounces, or 14.93 tonnes, as Beijing continued diversifying away from US dollar assets.

Source: Global Markets

Moreover, gold has stopped being a purely conservative lower-risk asset. And it does not even matter how much it costs right now. It is now an essential part of the global financial system like the US dollar or US Treasuries. It is one of the most essential components of central bankers’ foreign reserves because it does not depend on governments’ liabilities and protects central bankers’ portfolios from geopolitical tensions and fiat currencies’ devaluation. Official institutions are raising their gold holdings to move away from US dollar-denominated assets. Given geopolitical tensions, sanctions risks—think of Russia or Iran—and high government debt, bullion is an important part of global foreign reserves. Also, there is a strong de-dollarization trend. Emerging economic blocs like BRICS are raising their exposure to gold to reduce their reliance on Western financial hegemony. For central banks and financial institutions, gold is a preferred reserve asset thanks to its crisis performance and the fact that it is a universal store of value.

Risks to my base-case scenario

Higher inflation and higher rates obviously suggest lower prices for precious metals for longer. However, higher rates for longer mean higher chances of a coming recession, easier monetary conditions, and, therefore, higher gold prices in the long run.

The AI frenzy when investors buy high-tech companies because of their participation in the AI revolution is far from over. In the hope that the US-Iran conflict is over, speculators rush to buy the high-tech sector, while they ignore the real assets, namely companies operating in less fashionable sectors as well as precious metals.

Conclusion

In my view, the more gold and silver prices fall, the more intelligent investors should buy. Given all the fundamentals, the gold and silver prices’ correction seems to be temporary in nature. If the US-Iran conflict ends in the near future, the Fed is likely to become less hawkish, which is bullish for precious metals. But if the war does not end in the near future, it would likely provoke a recession, thus forcing the Fed to ease in the longer run.

Author

Anna Sokolidou

Independent Analyst

A research analyst, a freelance finance writer and an economics teacher looking for interesting investment opportunities. I have been investing for years. I am mostly interested in writing about commodities, precious metals and large corporations.