Sell on the rumor, buy on the news

Outlook:

We get May CPI this morning that will be followed by a flood of stories about this price being influenced by tariffs and that price being influenced by bad weather and other blather. In the end, what determines inflation is consumer demand, and as far as we know so far, the tax inherent in tariffs has yet to hit consumer sentiment in this manner. The headline CPI is likely the same 2.0% y/y as in April or a little lower. See the chart.

The CPI outcome makes us no wiser about the Fed’s attitude because the Fed doesn’t look at CPI. It looks at the PCE deflator. Evidently there is some argument going on about whether the Fed targets the headline PCE deflator or the core version. We have to go look it up sometimes ourselves to check press reports, and overnight, so did Marc Chandler, who is getting testy about it (and quite rightly, too). The document is from 2012 (and amended Jan 2019) and contains this statement.

“The Committee reaffirms its judgment that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve’s statutory mandate. The Committee would be concerned if inflation were running persistently above or be-low this objective. Communicating this symmetric inflation goal clearly to the public helps keep longer-term inflation expectations firmly anchored…”

If you want to quibble about something, make it the “annual change”—does that mean monthly change annualized or change year-over-year?

The public and no doubt some financial market experts are relatively clueless. The WSJ reports inflation expectations are falling among investors and the public on account of the forecasted global slowdown. The 10-year breakeven shows expected inflation at 1.7% from 2% in late April. Really? Is that the right way to measure expectations and can you say anything even remotely useful about a one-month change in a 10-year measure? (Well, no.)

To get even more ridiculous, there is a department at Barclays named “inflation-linked strategies.” That’s what the WSJ reports, no kidding. The head of that department says “investors’ bets that the Fed will cut interest rates late this year are merely preventing inflation expectations from declining faster.”

Bottom line, nearly all the talk about inflation and inflation expectations, whether by the financial community or the public, is poppycock. Even the best economist cannot estimate future inflation until we know the extent of the tariffs and when they will be applied and to what. If the economists can’t figure it out, the public can hardly be expected to know anything at all about inflation. After all, the public is still being told by the White House they are not the ones paying the tariff. Of course they do not have an informed opinion.

Broadly speaking, tariffs will raise prices but a drop in energy prices, if it persists because of a global slowdown, might offset, if not fully. Somebody with input-output tables might be able to cook up a proper estimate of future inflation, but as far as we know, nobody is doing that, or if they are, they are not telling the rest of us. So, if we can’t say anything intelligent about inflation over the next 6-12 months, how can we forecast what the Fed will do? Easy—it’s not really looking at inflation, or public survey-based inflation expectations. It’s listening with one ear to the finance guys in “inflation-linked strategies” departments and with the other ear to the White House.

In other words, the Fed is likely to promise a rate cut in July at the June meeting, buying time. Maybe they will know the tariff outcome by July. Realistically, that’s the best anyone could do. The FT reports “The implied odds of at least one quarter-point reduction to the Fed’s benchmark rate now sits at 98 per cent, with two or three quarter-point cuts being the most likely scenarios, according to CME Group calculations based on fed funds futures. Pimco, the world’s biggest bond manager, said on Tuesday evening that, while it does not expect the Fed to act when it meets next week, it may slash rates by 0.5 percentage points in July if “downside risks to the economy escalate”. “In a worst-case scenario, where tensions between the US and China are not at least scaled down before or during the G20 meeting in late June, the Fed could cut rates as early as the July meeting,” said Tiffany Wilding, Pimco US economist. “If this risk scenario comes to pass, we wouldn’t expect Fed officials to wait for the economic data to confirm declining US growth — if they do, they could risk a more meaningful shock to economic activity.”

For the FX market, the question is whether the dollar recovers once that rate cut is fully priced in—sell on the rumor, buy on the news.

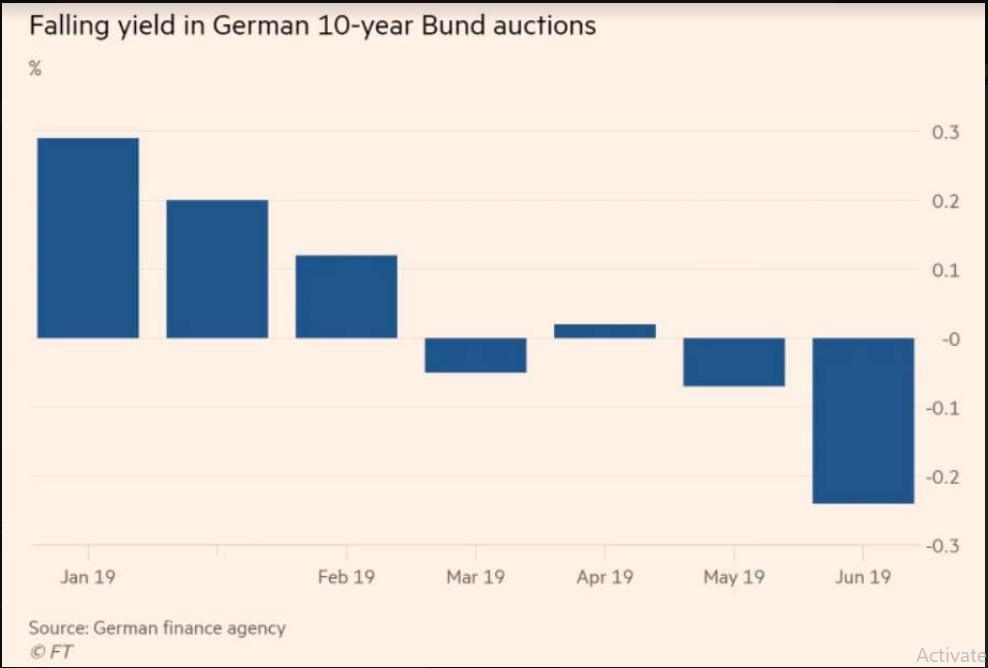

The Fed is probably running scared. Not because of the menace of possibly getting fired at any moment, but because there is a point of no return and Trump could be pushing us toward it. We say it’s at the zero bound. The Fed has only 2.25-2.50% to play with in Fed funds, which may seem like 8-10 rate cuts of 25 bp each but in practice is far fewer. Consider that Germany sold 10-year Bunds at a yield of -0.24%, the lowest ever and far below -0.07% only in late-May. How fast it fell!

The FT reports “The negative yield suggests investors who purchased the debt are guaranteed to sustain a loss if they hold it to maturity.” Nobody wants this paper. Buyers are buying only because they have to in order to meet their mandates.

The US also has a certain number of investment managers who must buy some government paper whether they like it or not, but a bigger number of people for whom owning US Treasuries is optional. Germany sees little drop in amounts sold even at the worst return ever, but remember, one of the holders in the ECB. The US could see a far bigger drop. See the Bund chart. This is what the Fed is afraid of.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a free trial, please write to [email protected] and you will be added to the mailing list..

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat