Second wave fears hit risk sentiment

Asian markets moved lower overnight and European bourses are pointing to a weaker start, as fears of a second wave of coronavirus infections drag on risk sentiment. As the number of covid-19 cases in Beijing jump and the US reports 25,000 new cases a day, investors are waking up to the threat of a second wave and the damage that it could cause to the global economic recovery.

24 US states, including the likes of Texas, and California are reporting a rise in cases. Some states such as Florida and Arizona are reporting a record rise in cases as the lockdown measures are eased. This weekend China closed the largest wholesale food market in Beijing and placed the surrounding neighbourhood in lockdown following 50 new cases in the capital.

These statistics are making investors acknowledge the high probabilities of a second wave of infections. The global economic recovery is very fragile, the overriding fear is that a second lockdown would mean additional economic paralyses and more dire economic consequences, pouring cold water over any hopes of a quick recovery.

The reality is that without a vaccine a full recovery is unlikely. Drawing comparisons with the Spanish Flu, a century earlier, the flu returned for four waves, infecting a third of the world’s population before eventually petering out. Whilst a second wave will be easier to manage given policy experience, volatility in the markers could well be with us for a while yet.

Chinese data disappoints

Data from China has done little to revive risk sentiment. Chinese industrial production rose 4.4% in May yoy, falling short of expectations of 5%. Retail sales fell -2.8% adding to signs that domestic demand in the world’s second largest economy remains weak.

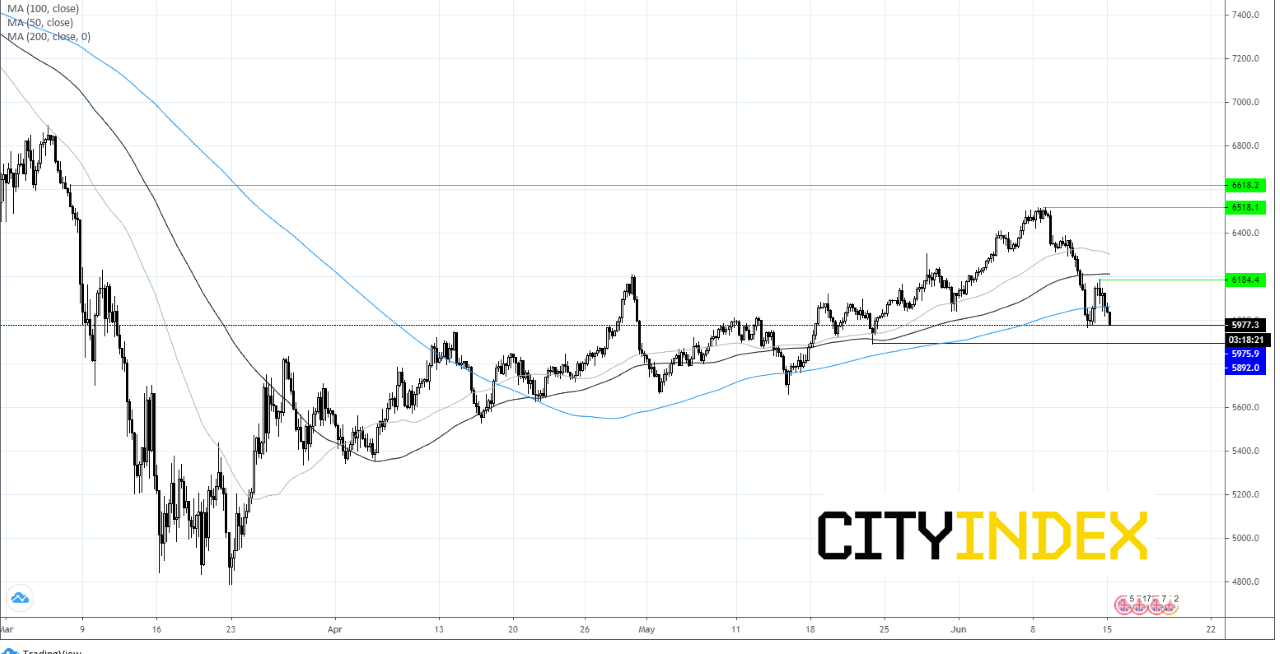

FTSE lower even as shops re-open

Despite a move higher on Friday, US and European stocks lost ground across the previous week. Risk aversion means investors are selling out of riskier assets such as stocks, at the start of the week. The FTSE, which plunged over 5% in the previous week is looking to extend those loses by around 1% even as shops reopen today for the first time in almost 3 months and data shows house prices ticked higher in June thanks to pent up demand from across the lockdown period.

Traditional safe haven gold rallied 2.6% across the previous week, its best weekly gain in 10 weeks are investors are once again turning cautious. Gold is consolidating those gains around $1725, falling away fom the overnight high of $1734.

Looking ahead

There are plenty of tests for the markets this week, with Powell testifying before Congress, the BoE rate decision and the European Union summit, in addition to a barrage of data including UK labour market figures, inflation and retail sales. A positive spin by Jerome Powell after last week’s warnings could overshadow second wave fears.

Oil tumbles

Oil is down 4% at the star of the week, extending losses of 8.3% from the previous week. The rebound in oil is starting to look shaky as fears mount over a second wave of covid-19 infections hitting demand for fuel. The recovery in oil was going to be a drawn-out move, fears of a second wave will mean that any recovery in oil demand will be even longer than initially thought. An OPEC meeting on Thursday to discuss ongoing cuts and compliance with cuts will keep oil on traders’ radar.

Author

Fiona Cincotta

CityIndex