Second and third waves are coming: Developed nations fall back on their lockdown playbook

The daily rate of global coronavirus has hit a new high of 106,000. Whilst the likes of Italy, Spain and Britain get things under some degree of control, elsewhere it's not looking so good. Of course, the economic effects of the pandemic have very little correlation with the disease, but the response by governments to lock down. The worry is second and tertiary waves are coming, and developed nations fall back on their lock down playbook. It's far from over.

Markets remain choppy as investors play the waiting game, whilst oil prices have risen again as inventory data painted a bullish picture. PMIs from Europe this morning show improvement but coming off an exceptionally low base in April. Germany's services PMI jumped from 16.2 to 31.4. France's rose from 10.2 to 29.4. It's a step in the right direction, but remember how these PMIs are calculated – respondents can only answer if the state of their industry is better, worse or the same as the month before. Contraction is still the state of play. Overnight data showed Japan's exports down 21.9%, the worst decline since 2009; whilst South Korean exports also plunged.

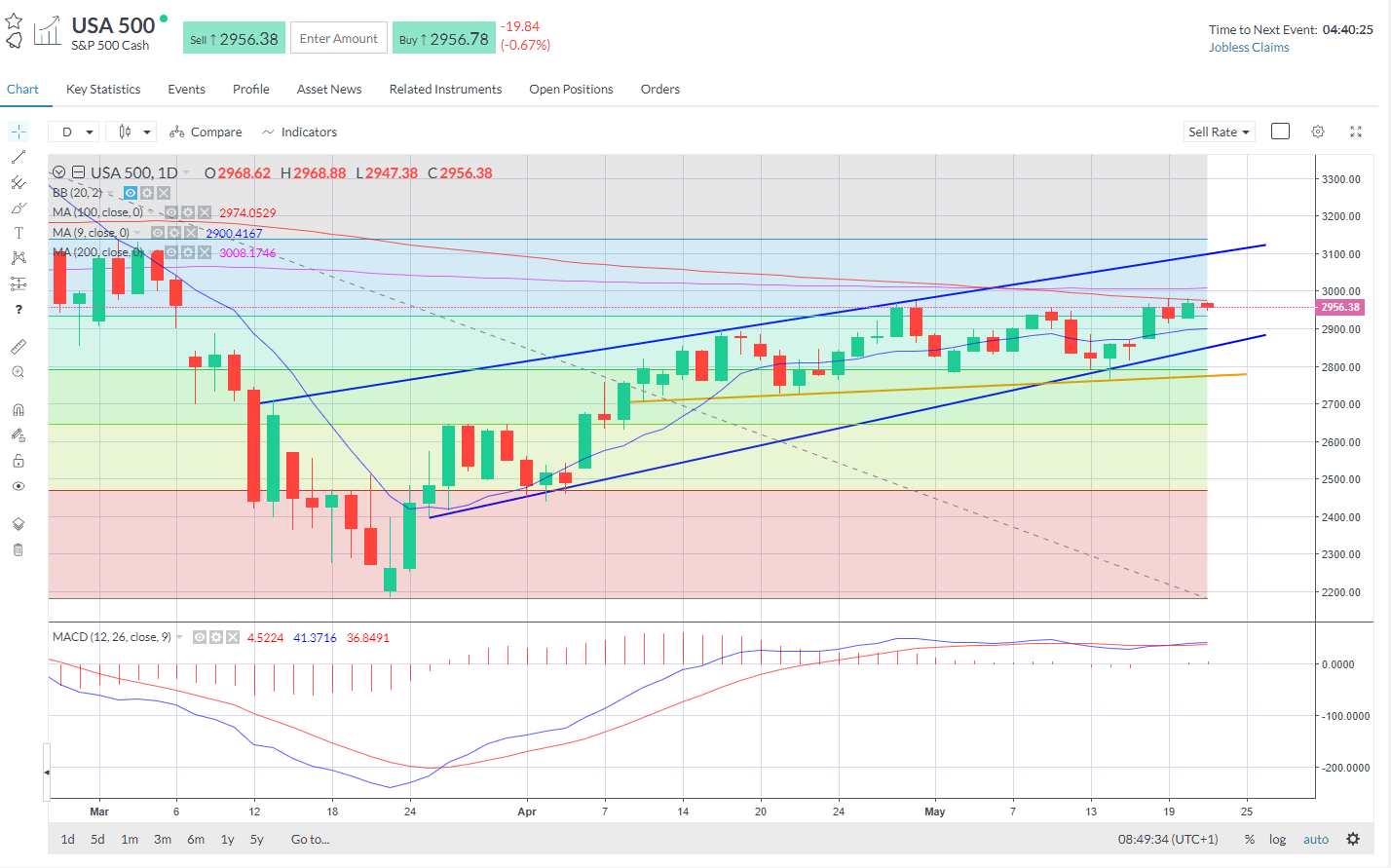

Stocks rose yesterday but eased back today as Asian trade data worried investors. The S&P 500 hit its best intra-day level since March 6th at 2980 (2985 on March 6th was the high), closing at 2971 vs the close of 2972 on that day. The 200-day simple moving average sits just above but the 100-day line has provided the topside resistance for the last two sessions. Futures indicate a lower open. The FTSE 100 rose 1% on Wednesday but handed back the gains at the open as European stocks faded. Equity indices are near or at the top of the ranges are still posting weekly gains. The US is creeping ahead of the pack with big tech driving things – Facebook soared yesterday after it announced a new e-commerce business that could take on Amazon. The Nasdaq rose 2%, ahead of the broad market, and is up for the year and not far away from its all-time highs.

Oil prices rose firmly after a bullish inventory report from the EIA. Crude stockpiles declined by 5m barrels in the week to May 15th, against an expected build of 1.2m barrels. But it was less bullish when you dig deeper into the report. Gasoline stocks rose 2.8 million barrels vs an expected 2.1m drop. Distillate stockpiles were up by 3.8 million barrels, which was more than expected. WTI (Aug) pushed up above $34 and is looking to close the March6th-9th gap. Oil is riding higher on great-than-expected loss of output in the US. After the EIA this week predicted a sharp decline in US output next month, the concern will be that higher prices sees the taps opened again.

Andrew Bailey, the governor of the Bank of England, chose his moment well: just as he told MPs that the Old Lady is prepared to consider negative rates, a UK gilt auction delivered a negative interest rate on three-year paper. The fact that the government can get paid to borrow money shows just how much central banks have already become ‘the market' for sovereign debt. The problem is, as discussed in a recent note, getting out of a negative rate cycle is tricky and the Eurozone and Japan are hardly poster children of monetary policy success.

Minutes from the Fed's last meeting were also released yesterday and showed a willingness to look at yield curve control, and still indicated no desire to go down the negative rate path. Once you go down it, it's exceptionally difficult to get out. Moreover, it's bad for banks and the financial system and doesn't make consumers more likely to get out and spend.

Chart: SPX tests 100-day resistance

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.