Russian economy: Growth facade, behind-the-scenes crisis?

The Russian economy is showing worrying signs of fatigue. Fueled by military spending, strangled by sanctions and undermined by labor shortages, the Kremlin's economic machine is moving down an increasingly unstable slope.

Behind Vladimir Putin's triumphant speeches and flattering statistics, cracks are multiplying: galloping inflation, companies running out of steam, middle classes under pressure, and a currency... too strong to be honest.

How can a country at war, isolated from the global financial system and deprived of Western technology, achieve economic growth rates higher than those of the G7?

The answer lies as much in strategy as in illusion. And the cracks now visible may well herald a much wider crisis to come.

A facade of resilience

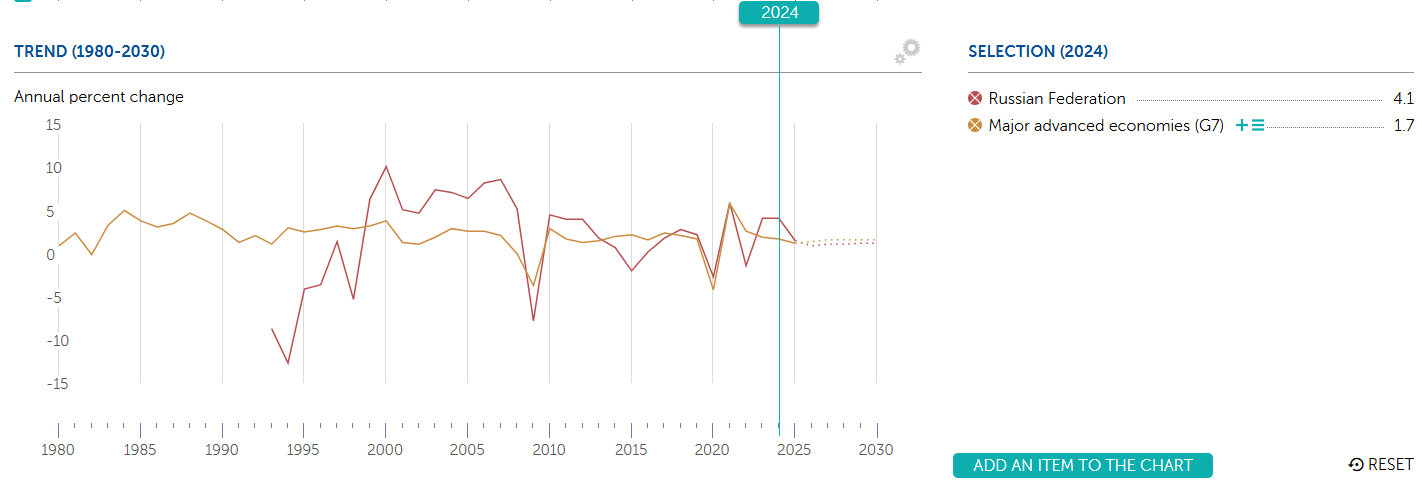

On the face of it, the Russian economy is bucking the odds. With growth of 3.6% in 2023 and 4.1% in 2024, according to CSIS, reporting data provided by Moscow, Russia would have done much better than most G7 economies.

Source: IMF

The Kremlin congratulates itself on exemplary "macroeconomic stability", record unemployment at 2.3%, reports BBC, and a Russian Ruble (RUB) among the best-performing currencies this year.

But behind the figures, the reality is quite different: this growth has been artificially inflated by a massive injection of public funds into the defense sector. It's a form of "military Keynesianism", notes CSIS in its report, with boosted salaries in the arms industries, enlistment bonuses, subsidized credits and forced investment. This dynamic proved effective to lift numbers in the first years of the war in Ukraine, but it is difficult to sustain in the long term.

"We grew for two years at a fairly high pace because unused resources were activated," said Russian Central Bank Governor Elvira Nabiullina. "We need to understand that many of those resources have truly been exhausted," she added, as reported by the BBC.

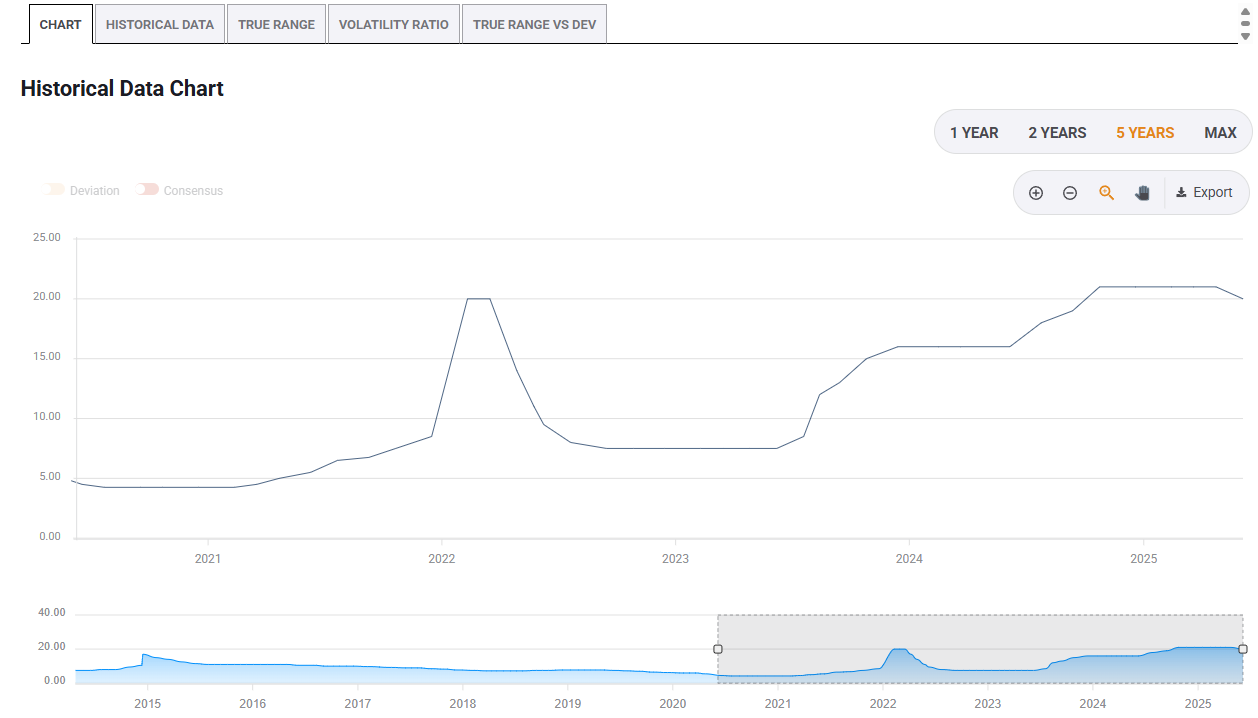

Inflation exceeded 9% in May and interest rates peaked at 21% before the first central bank rate cut in two years to 20%. Such high rates have strangled non-defense private investment.

Central Bank of the Russian Federation rates. Source: FXStreet.

As a result, civilian sectors are stagnating, business bankruptcies are soaring (up 26% in 2024, according to The Moscow Times), and consumption is slowing despite the apparent rise in incomes.

Even President Vladimir Putin, usually averse to confessions, has recognized the need to reorient the economy towards a more balanced trajectory, without putting the brakes on the war machine.

"Our most important task is to ensure the economy's transition to a balanced growth trajectory. At the same time, some specialists and experts point to the risks of stagnation and even recession. This should not be allowed under any circumstances," Putin said, according to the Kyiv Independent.

The Russian Rouble, a deceptive force

Another paradox of the Russian economy is the soaring value of the Russian Rouble (RUB). With a gain of over 40% since the start of the year, the Russian currency has become the world's best-performing currency this year, according to Bank of America, quoted by CNBC.

But this strength is not a reflection of renewed investor confidence, but rather the product of a cocktail of capital controls, high inflation, prohibitive interest rates, and a collapse in imports that is limiting demand for foreign currency. Large exporters, forced to convert their foreign currency earnings into Russian Rubles, are mechanically fuelling local demand for RUB.

At the same time, the contraction of the money supply and the hope of a de-escalation between Moscow and Kyiv have helped support the currency.

However, this solidity could soon turn against the Kremlin. Combined with falling Oil prices, it is eroding export revenues, reducing external competitiveness and weighing heavily on public finances.

Many analysts consider this rebound in the RUB unsustainable in the medium term, and predict a sharp correction if Russia were to lift its exchange restrictions as part of a possible peace agreement with Ukraine.

USD/RUB price chart. Source: TradingView

The illusion of autonomy

Sanctioned like no other nation, Russia has embarked on an "economic fortress" strategy: developing alternative payment circuits, replacing imports, diverting energy exports to China and India, and controlling capital.

But this autonomy remains partial. The energy sector, the mainstay of the budget, is faltering. Oil and Gas revenues fell by 35% year-on-year in May, according to the BBC, as the price of a barrel of Ural plunged below $50 and secondary sanctions on Russian Oil companies are beginning to take their toll.

Russia is even facing the threat of fuel shortages on its domestic market, as its refineries cut back on production.

Falling demographics

The Russian economy is also suffering from a deeper problem: the collapse of its workforce. Between mobilization, military deaths (up to 800,000 casualties in all, according to some estimates cited by the Bank of Finland Bulletin) and the mass exodus of skilled workers, Russia is cruelly short of manpower.

The shortage is estimated at between 2.7 and 3 million workers, notes Reuters, making any sustainable recovery difficult without massive migration, which Moscow is holding back out of a security reflex.

Poor attractiveness

While the Kremlin is courting the countries of the Global South to fill the void left by Western companies, the results are meagre. Foreign direct investment (FDI) is down 91% compared with 2021, according to The Moscow Times. China, despite being a strategic partner, accounts for just 0.3% of global FDI in Russia. Even the flagship "Power of Siberia 2" project, a Gas pipeline project between Siberian Gas fields and the Xinjiang region in western China, has stalled.

Geopolitical uncertainties, regulatory instability and Moscow's policy of arbitrary nationalizations are to blame. Hundreds of foreign assets have been seized or sold at knock-down prices to those close to the government, creating a general climate of mistrust.

Growth on credit

The federal budget shows a chronic deficit of 3.2 trillion rubles in the first quarter, according to Espresso, most of the National Wealth Fund has already been used up, and tax hikes are multiplying. The current model, financing the war through debt, taxes and asset redistribution, appears to have reached its limits. The IMF predicts a slowdown in growth to 1.5% in 2025 and to 0.9% in 2026.

"It's not an immediate collapse, but a slow, structural erosion, irreversible without a change of course", sums up economist Alexandre Kolyandr, as reported by The Moscow Times.

Towards a strategic impasse

Far from returning to normal, Russia is settling into a permanent war economy, to the detriment of its long-term potential. Productivity is falling, technological innovation is hampered by sanctions, and the economy is increasingly subject to political logic – loyalty to power rather than efficiency.

Barring a major geopolitical turnaround, this trajectory exposes Russia to a future of stagnation, fiscal fragility and increased dependence on a few complacent partners.

In the final analysis, the Russian economy is not collapsing, but it is bogged down in an autarkic, militarized impasse. Behind the Kremlin's shiny slogans, the figures point to an increasingly precarious dynamic.

Author

Ghiles Guezout

FXStreet

Ghiles Guezout is a Market Analyst with a strong background in stock market investments, trading, and cryptocurrencies. He combines fundamental and technical analysis skills to identify market opportunities.