‘Risk on’ theme should prevail into Nonfarm Payrolls

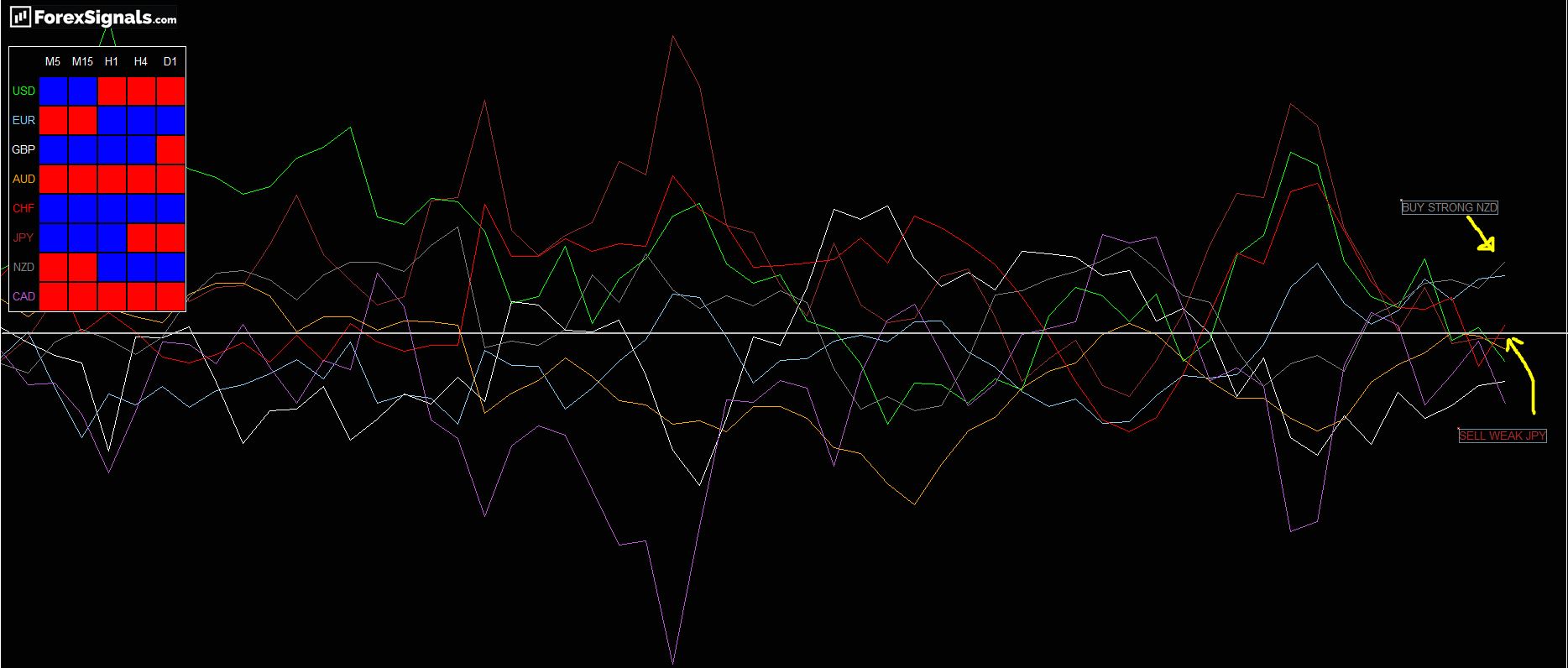

Powell kicked the USD in the gut last week with what should be considered a dovish stance on the economic outlook. Pressure had been mounting by fellow Fed members for an earlier timeline in the tapering process. Powel conceded that it was discussed that by the year-end the process would commence. However, he also reiterated that this was not an indication that higher rates would follow shortly behind. So cheap money is here to stay for longer. The stock markets have been thriving in the low-interest-rate environment which is likely to continue for the foreseeable future. Stocks higher means ‘risk on’ Risk on tends to support the high beta, commodity currencies such as the AUD, NZD and the CAD. The low yielders, the JPY and the CHF tend to get sold to fund the asset purchases. As trend followers, we like to buy strong and sell week.

The RBNZ recently surprised the markets by leaving rates unchanged against the strong expectations of a hike. A limited outbreak of Covid cases was deemed to be the underlying reason. We believe that once the current lockdowns in Australia and New Zealand ease their respective currencies will surge. Longer-term trades in buying NZDJPY, NZDCHF and AUDJPY could be the best game in town.

The biggest event this week to watch out for will be the Non-Farm Payroll numbers for August. Markets are expecting a read in the region of 650K new jobs added. Good job numbers are pretty much priced in. We believe, that unless we see a big shock to the upside, the USD will remain subdued with the bias to the downside.

Author

Andrew Lockwood

The City Traders

30 + years veteran trader registered and authorised under Financial Services Authority FSA (disbanded in 2013). Futures and Options trader on the London International Futures and Options exchange (LIFFE).