Risk-off rolls into Friday

Chip selloff deepens

I am waking up to a risk-off tape across equities this morning, with Asia-Pac shares on the ropes amid continued selling in the chip sector. Japan’s Nikkei 225 is down over 5% and on track to pencil in its worst single-day loss since March, while South Korea’s KOSPI has kept its door closed in observance of a national bank holiday.

Stateside, it was a similar picture on Thursday: red across the screen for major US equity indexes. The S&P 500 ended lower by around 0.5%, despite the majority of sectors finishing in the green, with consumer staples (XLP) the big winner on the day, up nearly 3%, and technology (XLK) unsurprisingly leading the way in losses, erasing 2.2%. In the individual names, Netflix (NFLX) took a hammering in after-hours trading, losing around 8% on lukewarm Q3 forecasts, despite printing stronger-than-expected earnings.

Hormuz tensions keep Brent bid

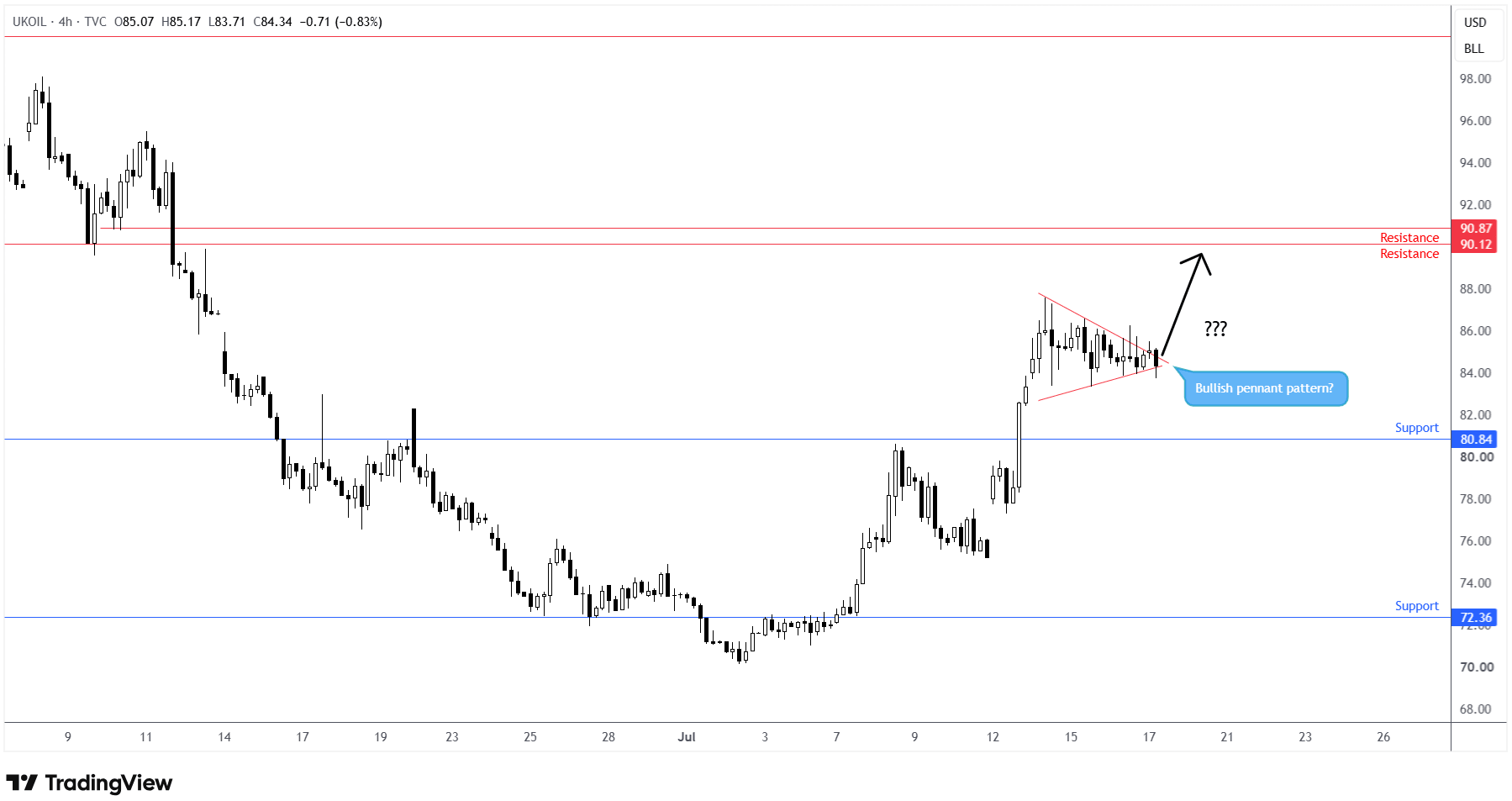

Moving away from equities, oil benchmarks remain front and centre as the US and Iran continue to trade blows. Brent crude remains around US$85/barrel and is on track to record 12% gains this week – its best performance since April. Despite the US saying the Strait of Hormuz is open for business, shipping volumes tell a different story. This will, of course, keep inflation concerns elevated for the time being.

The H4 chart of Brent crude below shows buyers and sellers squaring off between two converging lines to form a possible bullish pennant pattern, with price now at the apex. Is it brewing for a breakout higher, targeting neighbouring resistance of around US$90?

Spot gold, on the other hand, is down by nearly 3% this week. While this may seem counterintuitive given the geopolitical backdrop, I think this is largely due to rising real US yields, USD strength, and the potential for Fed hikes down the road.

FX and rates: USD steady and the Fed still watching inflation

In the FX space, the USD index ended higher yesterday, bolstered by daily support around 100.56. I find it quite something that USD has barely responded to the escalation in the Middle East, which, I would have thought, might have been enough to pull the buck higher on haven demand. On the data front, US weekly jobless filings fell to 208k (versus 217k expected), echoing a stabilising labour market, and retail sales eased amid lower energy prices.

Right now, with both June US CPI and PPI coming in softer than expected this week, this clearly offers the Fed some breathing space, hence the USD’s move lower. Should the situation in the Middle East stabilise and oil reclaim recent upside, this could be enough for the market to fade out rate-hike bets, I believe.

US Treasury yields were fairly muted yesterday, with the benchmark 10-year yield holding near 4.55%. The Fed Vice Chair Philip Jefferson recently hit the wires, and I feel his comments are worth flagging. He suggested the central bank should be prepared to raise rates again if inflation does not continue to cool, which sits awkwardly with a market that recently chopped out a fair chunk of Fed-tightening expectations.

Day ahead

On the data front, we have a slew of US releases on deck – including import prices, industrial production, and housing numbers – but I really do not see any of the reports offering market-moving impetus and they are considered tier-2 data.

We do have the July University of Michigan preliminary consumer sentiment index reading out later in the day, however, which could prove market-moving. Beyond the headline number, I will be paying close attention to the survey’s inflation expectations component – both the one-year and five-to-ten-year gauges – given how central the softer CPI and PPI prints have been to this week’s dovish Fed repricing.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,