Czech producer prices remain benign

Pricing in Czech industry remained subdued in June, despite the tangible impact of higher input prices in the early stages of the production chain. Agricultural producer prices saw an even more pronounced annual decline. Soaring prices in construction reflect ample demand and surging material costs. Consumer price stability is not under pressure.

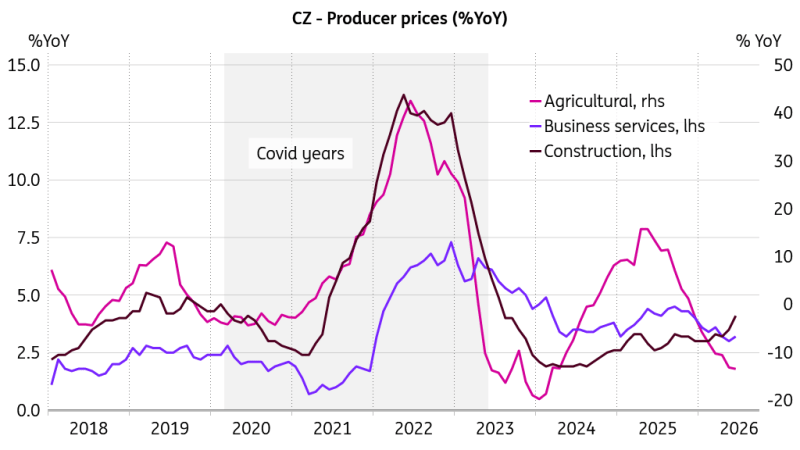

Agri prices remain in Tartarus

Czech industrial producer prices fell 0.4% month-on-month and gained by 1.3% year-on-year in June. On a monthly basis, we saw falling prices of coke and refined petroleum products, along with declining prices of food products. Agricultural producer prices dropped by 0.6% MoM, and the annual decline sharpened to 13.5%. Construction prices rose by 0.3% MoM and increased by 4.1% YoY, reflecting buoyant demand in the housing market combined with surging prices of basic materials linked to the Hormuz crisis. Prices of market services for businesses rose by 0.1% MoM and by 3.2% YoY in June. That said, annual growth in business service prices has been softening gradually from its 4.5% peak in September 2025, which is in line with our hypothesis that pricing in the services sector is becoming somewhat saturated.

Agricultural producer prices fell more sharply on an annual basis. Soaring construction prices reflect strong demand and rising material costs. Consumer price stability remains intact.

Pricing in business services has eased

Agricultural producer prices have been in annual decline since the end of 2025, with the June reading coming in below our forecast. We believe that higher energy prices will trickle down to agricultural producer pricing over the rest of the year, although the timing is uncertain due to the seasonal harvesting of vegetables and other unprocessed foodstuffs.

Limited price pressures for consumers

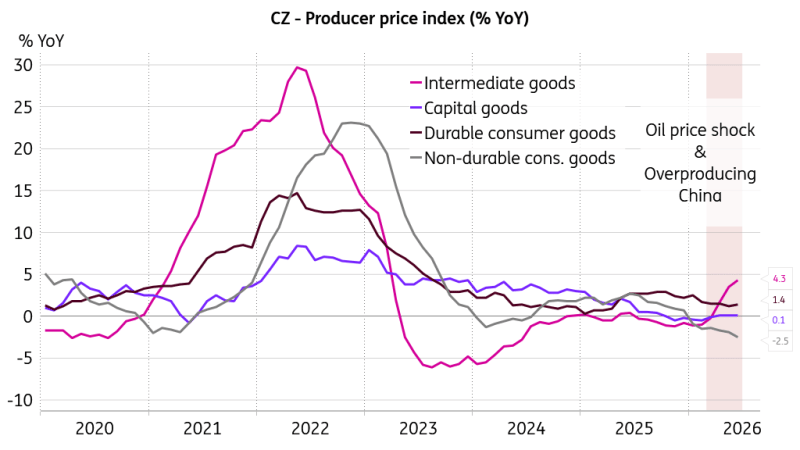

When looking at the main industrial groups, prices of intermediate goods and energy continued to grow on an annual basis in June, while prices of non-durable consumer goods declined from a year earlier. Higher energy costs are clearly tangible in the earlier stages of the production chain, while their pass-through to final goods appears somewhat limited so far. The main dampening force stems from cut-throat international competition, especially from Chinese imports sold at heavily discounted prices.

Cost pass-through to final production is limited for now

Sine ira et studio, the Czech PPI reading suggests benign price pressures for the consumer. Industrial price growth was only 0.1ppt above our forecast, while the agricultural price index came in a bit weaker than expected. We don’t see substantial threats to price stability over the forecast horizon, except for the risk of geopolitical tensions potentially getting out of hand, with profound implications for Brent crude prices.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.