Risk appetite strengthening as coronavirus trends continue to improve [Video]

![Risk appetite strengthening as coronavirus trends continue to improve [Video]](https://editorial.fxstreet.com/images/TechnicalAnalysis/Sentiment/RiskAppetite/parachute-jumping-72480495_XtraLarge.jpg)

Market Overview

Risk sentiment continues to improve as there are ongoing signs of improvement in daily death rates of Coronavirus and discuss begins to turn to exit strategies for some countries. This helped to spur renewed appetite for risk that ran strongly higher throughout the US session yesterday. Treasury yields have turned a near term corner and are continuing to driver higher today. The US 10 year yield has increased by 13 basis points now from Friday’s close. This helped drive Wall Street markets strongly higher and the legacy of +7% gains is being felt across equities early today. The dollar which has been acting as a safe haven is subsequently under corrective pressure today against all major currencies. This is true even of sterling which had an initial knee-jerk sell-off yesterday on news of Prime Minister Johnson being moved into intensive care due to breathing difficulties. The Reserve Bank of Australia monetary policy decision was reportedly in the balance but the RBA opted to maintain rates at +0.25%. This has helped the Aussie to outperform today. It will be interesting to see how long the broad positive bias lasts for major markets, but for now, risk is back on again.

Wall Street closed with huge gains as the S&P 500 jumped +7.0% into a close of 2663. US futures are also building on this move early today with gains of +1.3%. This has helped Asian markets stronger with the Nikkei +2.0% and Shanghai Composite +2.0%. In Europe, the outlook is decent early in the session with FTSE futures +1.8% and DAX futures +2.7%. In forex, there is very much a risk positive, USD negative move. The big outperformers are the commodity currencies AUD and NZD, whilst the safe havens of JPY and CHF are mild laggards within the dollar correction. In commodities, volatility on oil continues to play out with gains of +2% ahead of the OPEC+ meeting on Thursday. Silver continues to jump higher whilst gold is consolidating yesterday’s huge gains.

It is fairly light on the economic calendar today. The JOLTS jobs openings at 1500BST catch the eye as another interesting insight into the state of the labor market in the US. Job losses are huge, but what about openings? Consensus expects openings to have fallen back by over -5% in February to 6.60m (from 6.93m in January).

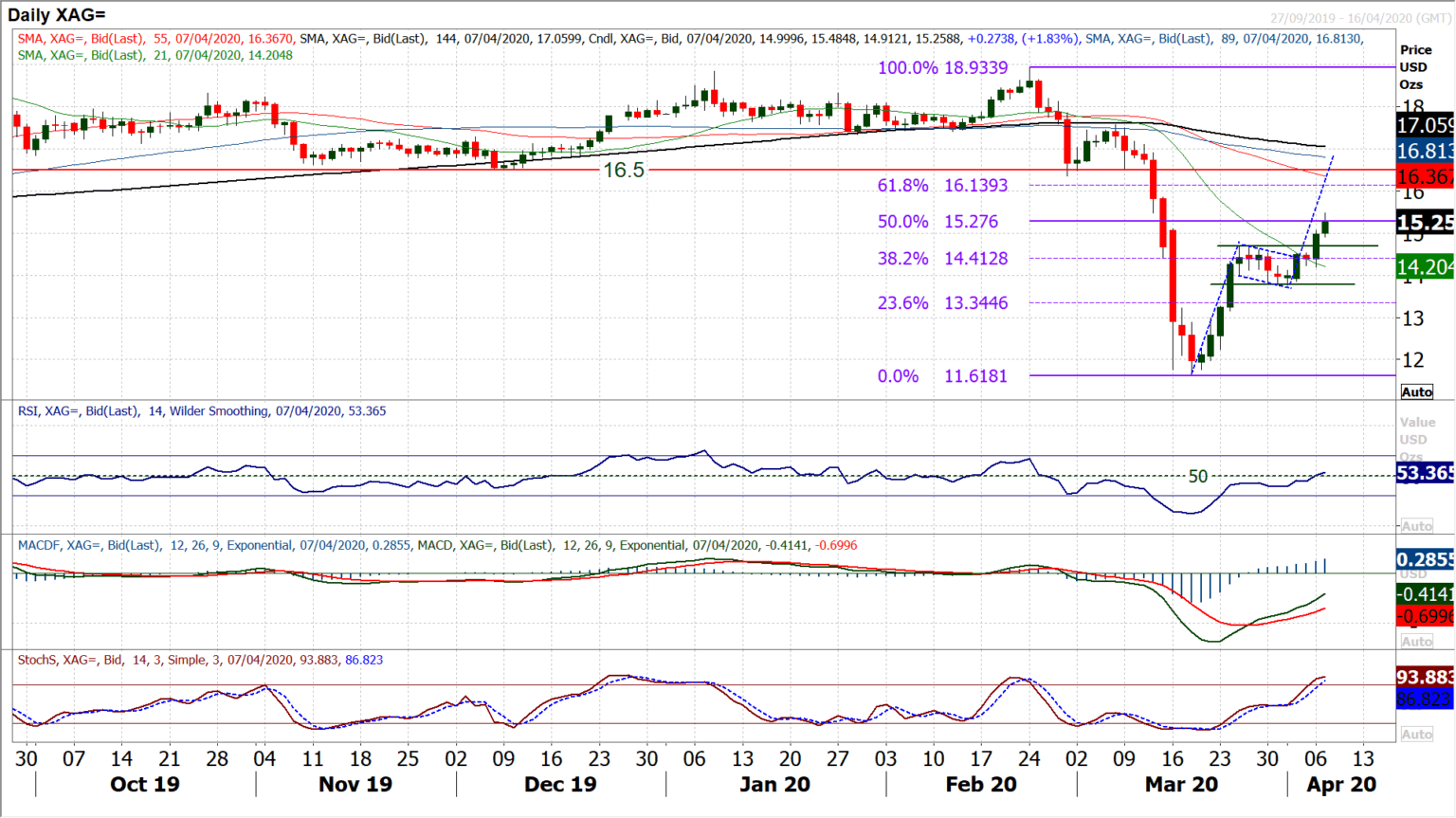

Chart of the Day – Silver

Gold broke out yesterday in a sharp move higher, but has silver matched its move? Silver has been consolidating over the past week and a half in a mini-range between $13.77/$14.70 but with two strong bull candles in the past three sessions the bulls have re-taken control. What was interesting to see that the breakout above $14.70 was initially tentative yesterday, but once the bulls got clear, the move really accelerated higher. This formed a hugely positive bull candle in a move which has continued today. This decisive close above $14.70 has completed a range breakout would imply around $0.95 of upside towards $15.65. The less conservative of the bulls would also be looking upon the breakout as that of a bull flag which would imply $17.00. Whatever the implication, the bulls are on track now for continued recovery. The next key resistance of overhead supply is now not until $16.50. Momentum indicators confirm the breakout, with an acceleration higher of Stochastics and MACD lines rising and RSI at a five week high above 50. The 50% Fibonacci retracement (of $18.93/$11.62) is around $15.28 and a potential consolidation point today, but once clear this opens 61.8% Fib at $16.14. We look to now buy into weakness with the breakout at $14.70 a great support area now. The bulls are in control whilst above $14.20.

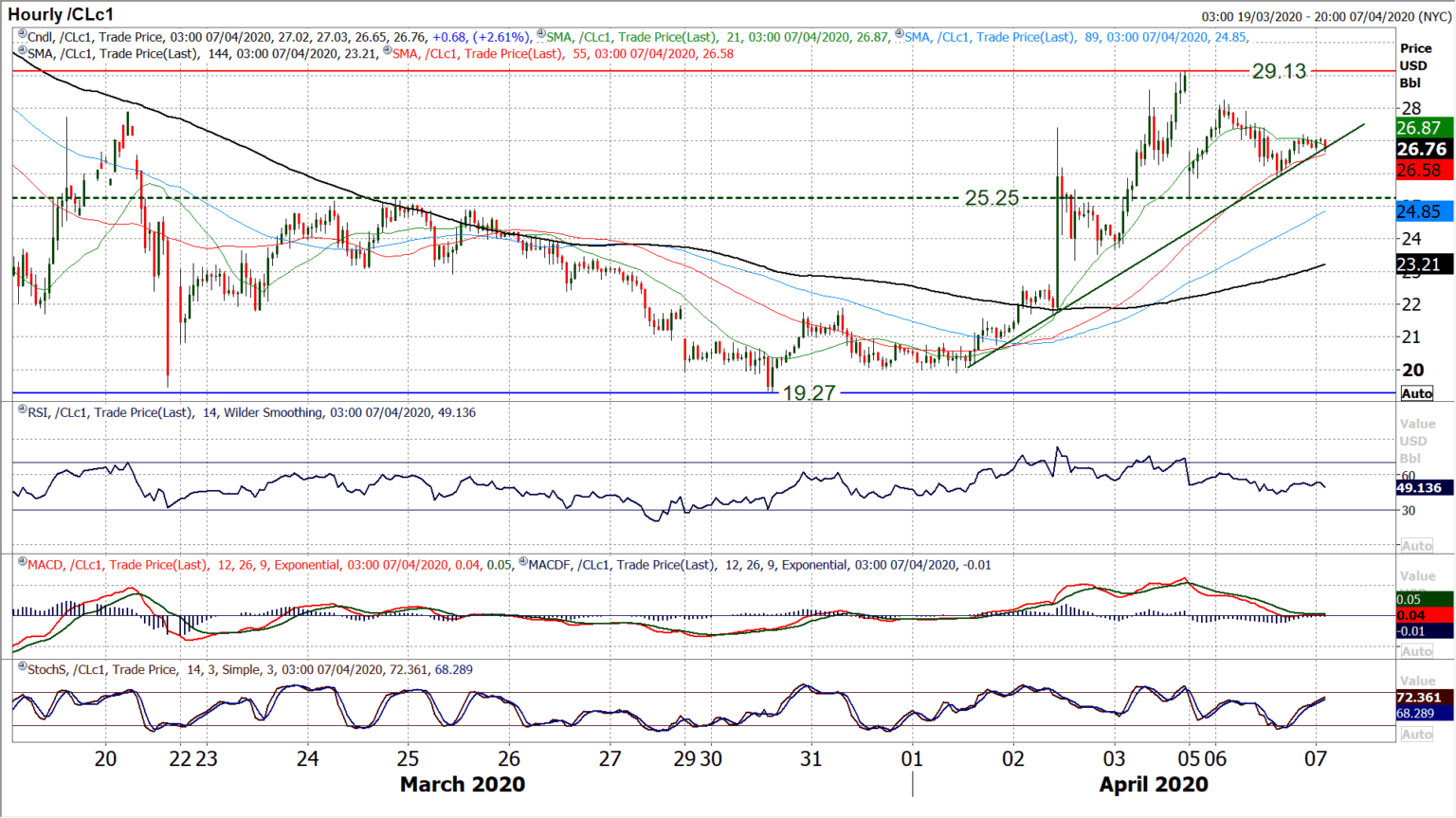

WTI Oil

With the volatile recovery of last week still bubbling away, moves on WTI remain not for the feint-hearted. Another session of intraday swings started a week sure to be packed with ongoing volatility (at least until we get a decision from OPEC+). However, an “inside day” that left a sharp close lower but a doji candlestick on a day of $3 of range reflects the near term uncertainty. The recovery is though technically on track with momentum indicators still tracking higher and the legacy of those two massive bull candles still in the market. The hourly chart shows the wild swings settling to an extent this morning, with momentum on hourly RSI and MACD beginning to stabilize around their neutral areas (c. 40/60 on RSI). Initial support is at $25.90 but the bulls would not be confident if they lost the old $25.25 pivot which is now supportive. A minor lower high comes in at $28.25 under Friday’s high of $29.13.

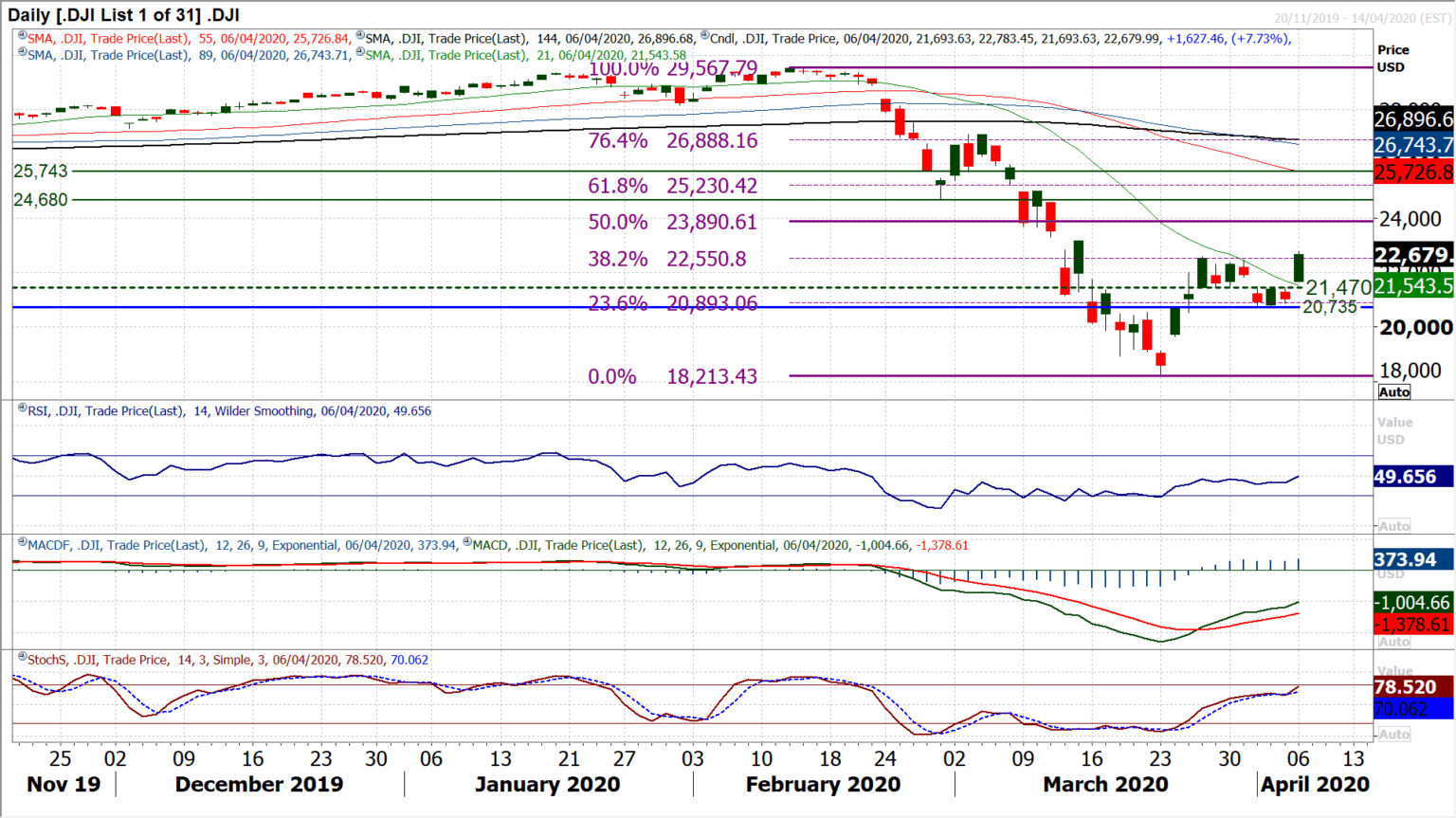

Dow Jones Industrial Average

The positive reaction of yesterday’s session could be significant on a medium term basis. Posting a hugely strong positive candlestick that saw the market breaking to a three week high has significant technical implications. First and foremost it means that the recovery is well on track. The bulls had been wavering throughout last week, but a key higher low has now been formed at 20,735 and technically this means a new bull trend formation of higher lows and higher highs. The recovery may go through ups and downs from here, but whilst the support at 20,735 is intact as the first major support, the recovery is still building. Momentum indicators confirm the breakout, with RSI at a six week high (around 50), whilst Stochastics and MACD accelerate higher. The reaction today will though be important, as after a breakout the bulls would at least look to back up this move with at least a solid session of support. The breakout support at 22,480/22,595 is the first buffer, although given an Average True Range of 1268 ticks, the intraday volatility may well take this out. So yesterday’s traded low at 21,670 is next before a pivot and breakaway gap at 21,470. These are levels the bulls will certainly look to be holding now. Moving clear of the 38.2% Fibonacci retracement (of 29,567/18,213) at 22,550 would be bullish and open 50% Fib at 23,890 as a target area. The next resistance is 23,190/23,330.

Author

Richard Perry

Independent Analyst