Risk appetite picks up after improved China inflation

Market Overview

Market sentiment has rebounded after a disappointing session yesterday. The late recovery on Wall Street came as oil rebounded into the close and the dollar is now looking to resume its trend higher. Markets are also reacting to the positive news on Chinese inflation which recovered sharply to +1.9% after four months of CPI declines and probably more significantly, the factory gate inflation (PPI) at +0.1%, turned positive for the first time since January 2012. The improved China inflation is helping risk appetite today with the yen and gold weakening, whilst the riskier Aussie and Kiwi currencies are holding up well. Equities are also looking more positive this morning. Improved risk, positive oil and renewed sterling weakness should again help to ensure FTSE 100 positive performance. The market will be focusing on today’s US Retail Sales data for another signal towards a December Fed rate hike, whilst Janet Yellen gives a speech titled “Macroeconomic Research After the Crisis” tonight at 1830BST although she is likely to tread a fairly consistent line with the recent Fed minutes which pointed towards a rate hike “soon” if recent economic trends continue.

Wall Street closed well off its lows of the day with the S&P 500 -0.3%, whilst Asian markets have been mixed to positive with the Nikkei +0.5%. European markets are positioned for early strength. Forex majors show the dollar strength is resuming with gains versus the yen and the euro whilst sterling is once again lower. Only the Aussie and Kiwi are currently managing to hold up. Gold and silver are mixed to slightly lower as the consolidation continues, whilst oil is looking to maintain yesterday’s recovery gains.

Traders will be looking out for US core Retail Sales (ex-autos) at 1330BST (+0.4% MoM expected) in addition to the preliminary reading of Michigan Sentiment at 1500BST which is expected to improve slightly to 91.9 (91.2 last). Yellen is also in focus at 1830BST.

Lucky 8 – FX Trader of the Year 2016 competition update

I am now moving on to look at a new set of Lucky 8 instruments for Week 2 of our competition that we are running throughout October. I will be giving daily updates on how the Lucky 8 instruments of the week are performing.

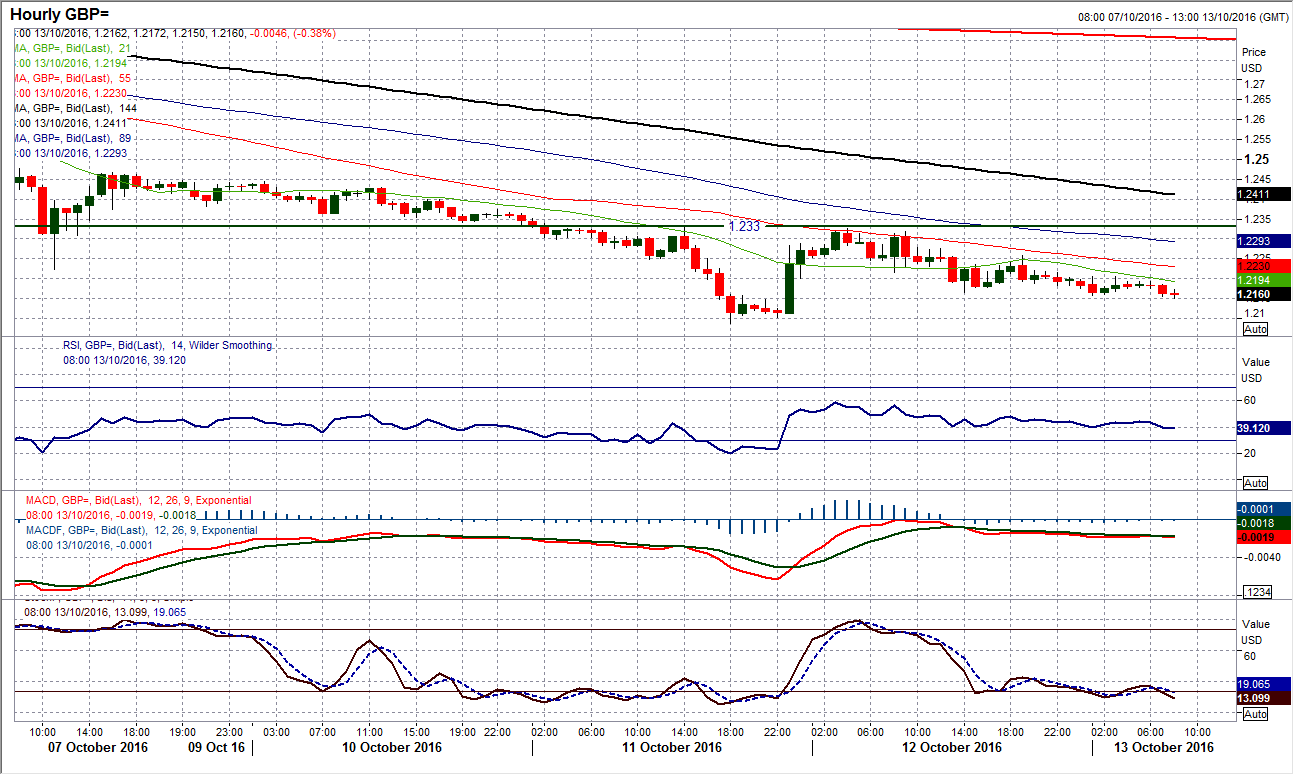

GBP/USD – With bearish configuration continuing look to use intraday rallies as a chance to sell. Yesterday’s rally peaked at $1.2270 before the bears have taken back control again early today as hourly momentum has rolled over. This is turning into a bit of a range but expect a test of $1.2130. Key resistance is at $1.2330. (See below for more detail).

NZD/USD – The consistent selling pressure has abated with a bull hammer from $0.7030 on the daily chart which could drive a near term bounce. The hourly chart shows that the bulls need to hang on to $0.7075 initial support otherwise the recovery could struggle. Back above $0.7130 reopens the rally potential.

EUR/GBP – Another pair where sterling is consolidating now Is against the euro as hourly indicators flatten. There is though still an upside risk with a higher low at £0.8995 above £0.8963. A move back above £0.9067 would reopen £0.9140.

EUR/AUD – The daily chart shows downward pressure continues on 1.4530, with bearish momentum and a series of lower highs in the past week. The hourly chart shows an initial bounce today but the resistance 1.4575/1.4620 is now a basis of resistance for the next sell-off.

USD/ZAR – The consolidation following the rally looks to be turning into a retracement drift as lower highs have been posted in the past couple of days. The rally off 14.10 needs to now hold, but with the hourly momentum indicators in neutral configuration the market is increasingly ranging. Resistance at 14.39 holds the range.

FTSE 100 – The corrective move on the FTSE has seen the index retreat back to a key basis of support. There is a band 6928/6955 which are a series of old highs back from the late summer that are now supportive and these held yesterday with a bounce from 6930. The bulls now need to break back above the 7000 resistance to regain some confidence in the medium term bull run.

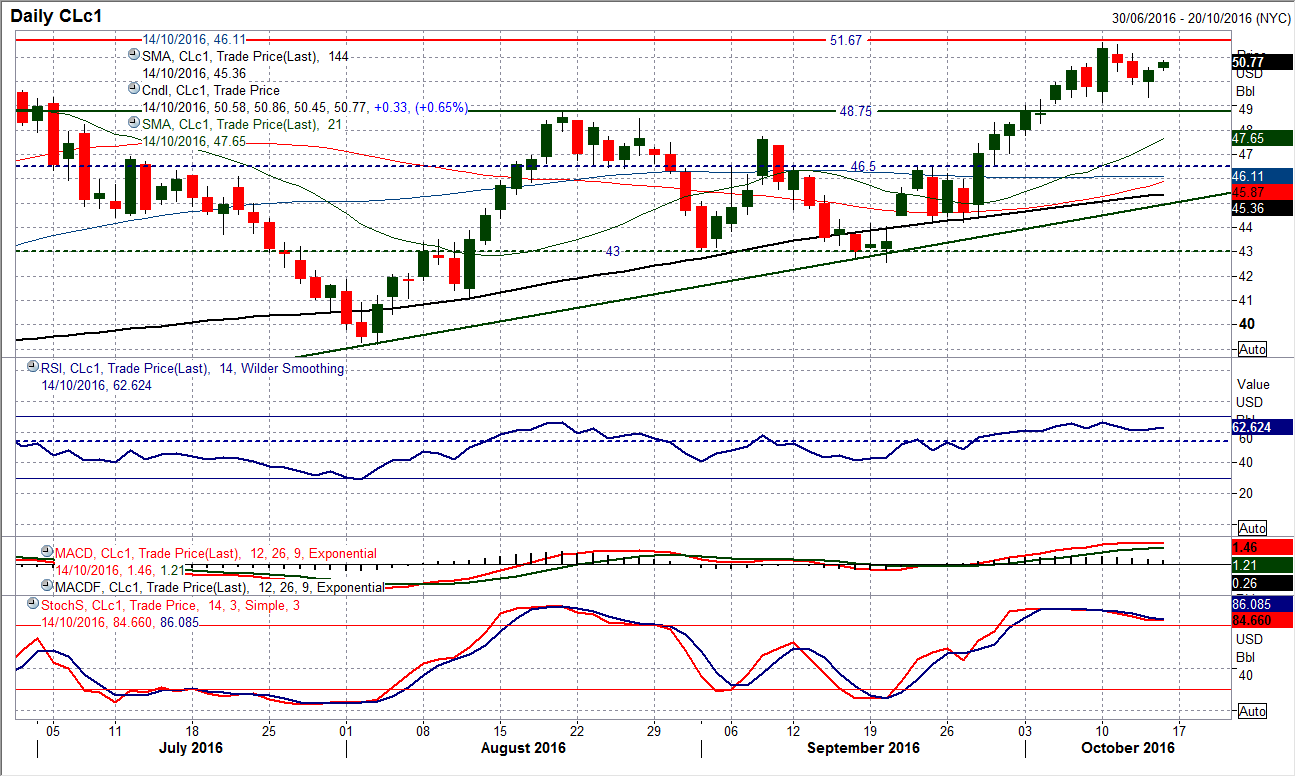

WTI Oil – Corrections are still being seen as a chance to buy and the improvement in the near term outlook means that the resistance at $51.15 is now within sight. $49.35 now protects $49.15 key support. (See below for more detail).

Cocoa (CCc1) – A strong bull candle shows that there is another potential near term recovery forming, but as has been the case across the last 8 weeks, the rallies are still likely to be sold into. Although momentum has ticked higher, the negative configuration on daily momentum indicators suggests that the resistance between 2708/2755 will be eyed for the next opportunity. Support at 2625 will be retested in due course.

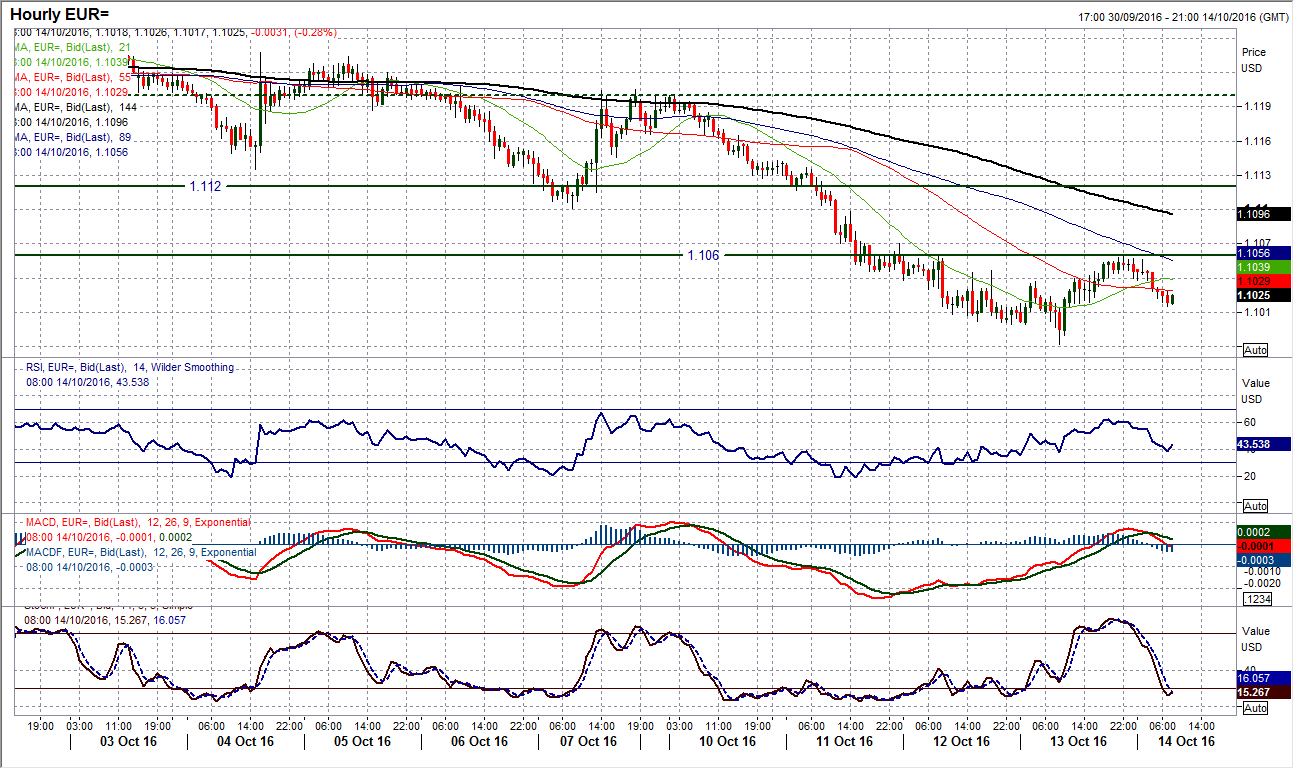

EUR/USD

After three strong bearish candles which have seemingly changed the outlook for EUR/USD there has been a slight unwinding of the move. This has come as the RSI had moved towards 30 which is a level considered to be extreme for the world’s most liquid currency pair. However I would still be looking to use rallies as a chance to sell. The breakdown of the long term pivot band $1.1050/$1.1100 now means that this becomes a key area of overhead supply. It seems that as the bears have stunted the rally overnight, this pivot band is once more acting as a basis of resistance. Momentum configuration remains bearishly configured despite the bounce and the hourly chart shows this move is simply helping to renew downside potential There is initial resistance is now $1.1060/$1.1070 on the hourly chart and look for rallies to be seen as a chance to sell. I continue to expect further pressure towards the key lows at $1.0950 with the initial support at $1.0982.

GBP/USD

The market remains volatile and despite the relatively small candle showing on the daily chart the high to low range was still 120 pips for yesterday’s session. The bears are in control and the market has now posted lower daily highs for the past 10 sessions. Momentum indicators show little to suggest any real prospects of a sustainable rally and this implies that intraday rallies should continue to be sold into. The hourly chart shows the importance of the resistance at $1.2330, whilst yesterday’s rally failed at $1.2270 and leaves further resistance. Hourly indicators are again falling away and suggests a negative drift but there is support at $1.2130 and if this holds the market could begin to form a consolidation range pattern. Whilst the market remains stuck below $1.2480 the bears will remain in control.

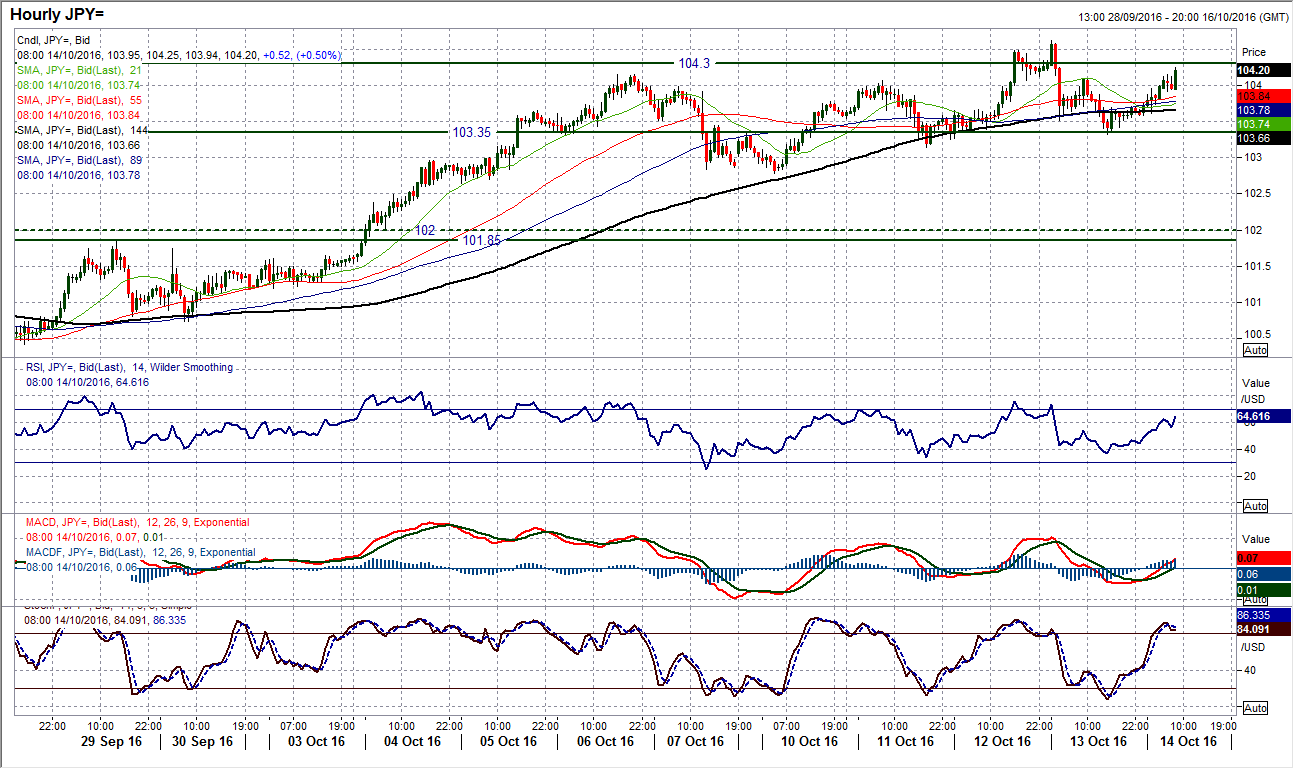

USD/JPY

The challenge of a break above the resistance of the September high at 104.30 has been a bit stop/start, however the bulls remain in control. With the key near term support intact at 102.80 the market is building for a breakout and yesterday’s slightly corrective candle has given the bulls another chance for a run at the resistance today. I still see an improving outlook on the medium to longer term outlook and the market closing above 104.30 would confirm this. The hourly chart shows positively momentum, whilst the 103.15/103.35 support band has once more provided the basis for the renewed push higher today. The bulls seem to be preparing for another go at 104.30 with the intraday resistance at 104.62. A clean break would open 105.50.

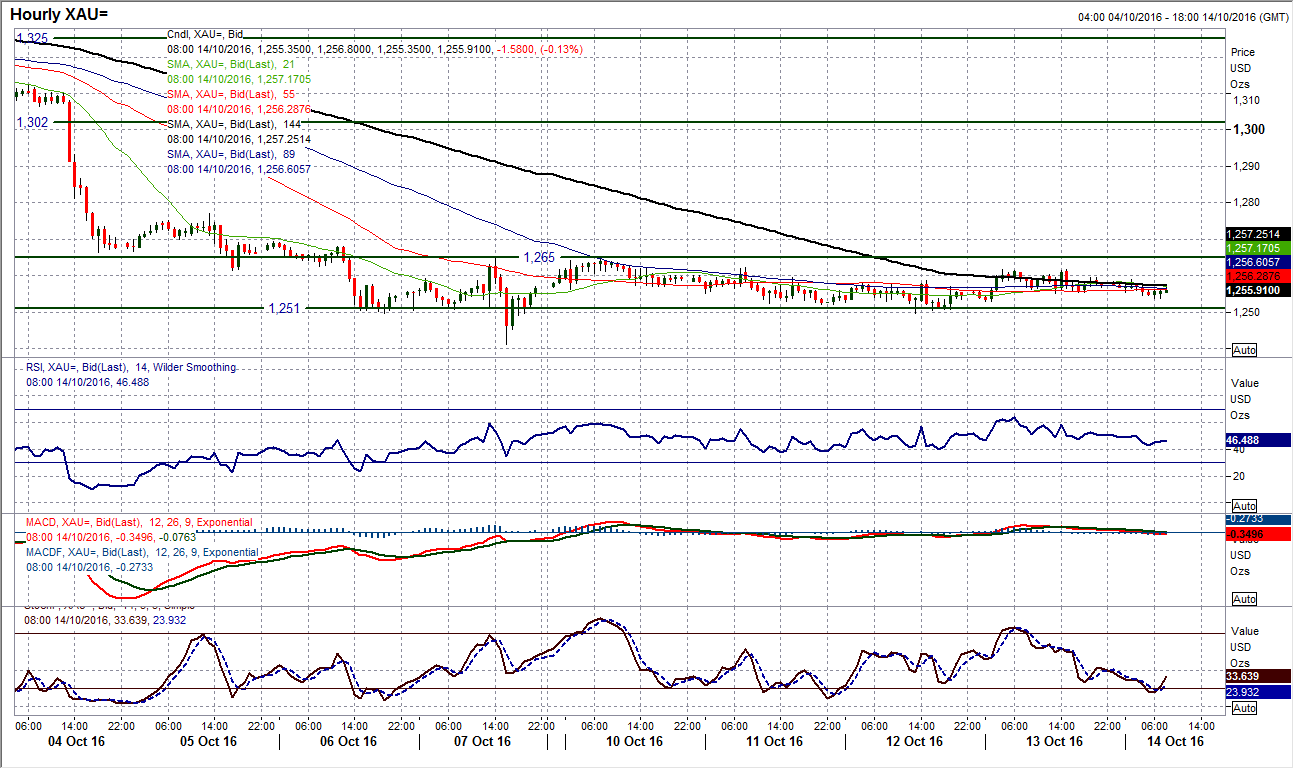

Gold

The consolidation continues on gold as once more a small body of a somewhat disappointing candle posted suggests that the bulls are still really struggling to form a recovery. The momentum indicators are also failing to get any real traction going either and this has the look of a bear market consolidation/rally to it. That means that even if the bulls manage to pull the price slightly higher, this is likely to come up against an overhead supply of sellers as the momentum really does not seem to be there for a recovery. The resistance initially at $1265 continues to hold and there would need to be a push above $1277 to realistically have any prospect of a serious recovery. Today’s slight drop back continues this outlook. For now though the market is in consolidation mode but not overly intent on selling gold lower either. The reaction to the support at $1249.70 will now be telling as the initial support, with a breach opening $1241.20 again.

WTI Oil

he bulls were under pressure yesterday as a third day of losses looked to be ready to test the key near term support at $49.15. A mixed takeaway from the EIA oil inventories report (gasoline and distillates had a bigger drawdown than expected, but crude stocks showed a bigger than expected inventory build) saw the market uncertain how to react but the bulls won over and a turnaround on the day has left a higher low at $49.35 and the positive near term momentum has kicked in again. These gains have thus far been held today and the bulls will be eying the initial resistance at $51.15 before the big barrier of $51.67 again. Corrections are still seen as a buying opportunity.

Author

Richard Perry

Independent Analyst