Risk appetite continues to build for 'phase one' with GBP hit by the BoE doves

Market Overview

Although the immediate geopolitical risk of the Iran/US missile exchanges in Iraq has been put on the back burner for now, the issue will continue to rumble on. This is likely to be a drag on Treasury yields in the coming weeks however, for now the near term focus switches back to the trade dispute and to “phase one” again. On Wednesday, the US and China are expected to sign the first section of their trade agreement. Risk appetite is positive (the VIX hit its lowest in two weeks on Friday, whilst the Chinese yuan strength is at five month highs to drag USD/CNH under 6.90 this morning). The market is anticipating phase one to be signed, but when it comes to the US and China, anything could still happen. Although Treasury yields are hovering, elsewhere the risk improvement is showing through, with gold slipping back whilst the yen is also sliding and equities are supported. This the forex space, one big mover is a drop in sterling. There is an increasing number of Bank of England MPC members talking of the prospects of rate cuts. One of the more dovish members, Gertjan Vlieghe suggesting that he would likely be voting for a rate cut in the next meeting. This is the third dovish comment (alongside Governor Carney and Silvana Tenreyro) in the space of a few days.

Wall Street closed slightly lower in the wake of a drab Non-farm Payrolls report on Friday (S&P 500 -0.3% at 3265) but US futures are rebounding today (+0.3% currently). This has allowed Asian markets a bounce with the Nikkei +0.5% and Shanghai Composite +0.8%. In Europe there is a mild recovery with FTSE futures and DAX futures both around +0.1% higher today. In forex markets, there is a slight risk positive bias, with AUD and NZD higher, whilst JPY and CHF are mildly weaker. The big mover is GBP where key lurch lower on Cable by around half a percent has been seen. In commodities there is a drop back on gold and silver by over half a percent, whilst oil is beginning to consolidate.

There is a UK focus on the economic calendar today. Monthly UK GDP for November is at 0930GMT and is expected to be flat on the month (0.0% in October) with the year on year growth at +0.6% (down from +0.7% in October). UK Industrial Production for November is expected to fall by -0.2% on the month (after growth of +0.1% in October) which would pull the year on year decline back to -1.4% (from -1.3% in October). The UK Trade Balance for November is at 0930GMT is expected to see the deficit improve to -£11.7bn (from -$14.5bn in October).

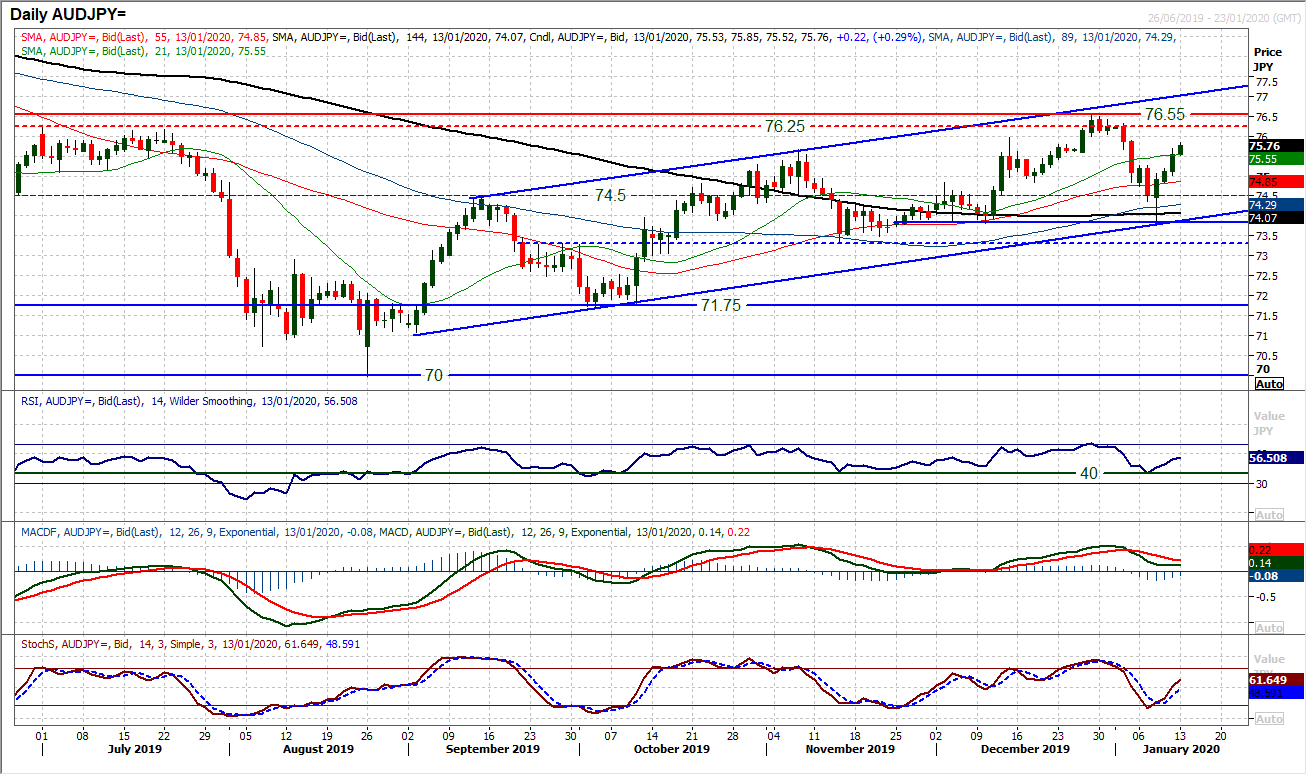

Chart of the Day – AUD/JPY

We have been looking at a risk recovery in recent sessions and this is once more evident through the outlook on Aussie/Yen. A near term corrective move back from 76.55 in December to bounce off 73.75 last week effectively now has formed an uptrend channel of the past four months. Now we see three consecutive strong bull candles have swung the market back into a renewed upward phase again. The uptrend channel is reflected across momentum indicators where the RSI is picking up consistently on the corrections around 40, whilst MACD lines are again holding above neutral and the Stochastics are accelerating higher from a bull cross. The market is now primed to test the resistance band 76.25/76.55 in the coming days. Near term corrections should be seen as a chance to buy. Immediate resistance is an old pivot around 76.00. On the downside, near term breakout support is at 75.25 with an old pivot at 74.50.

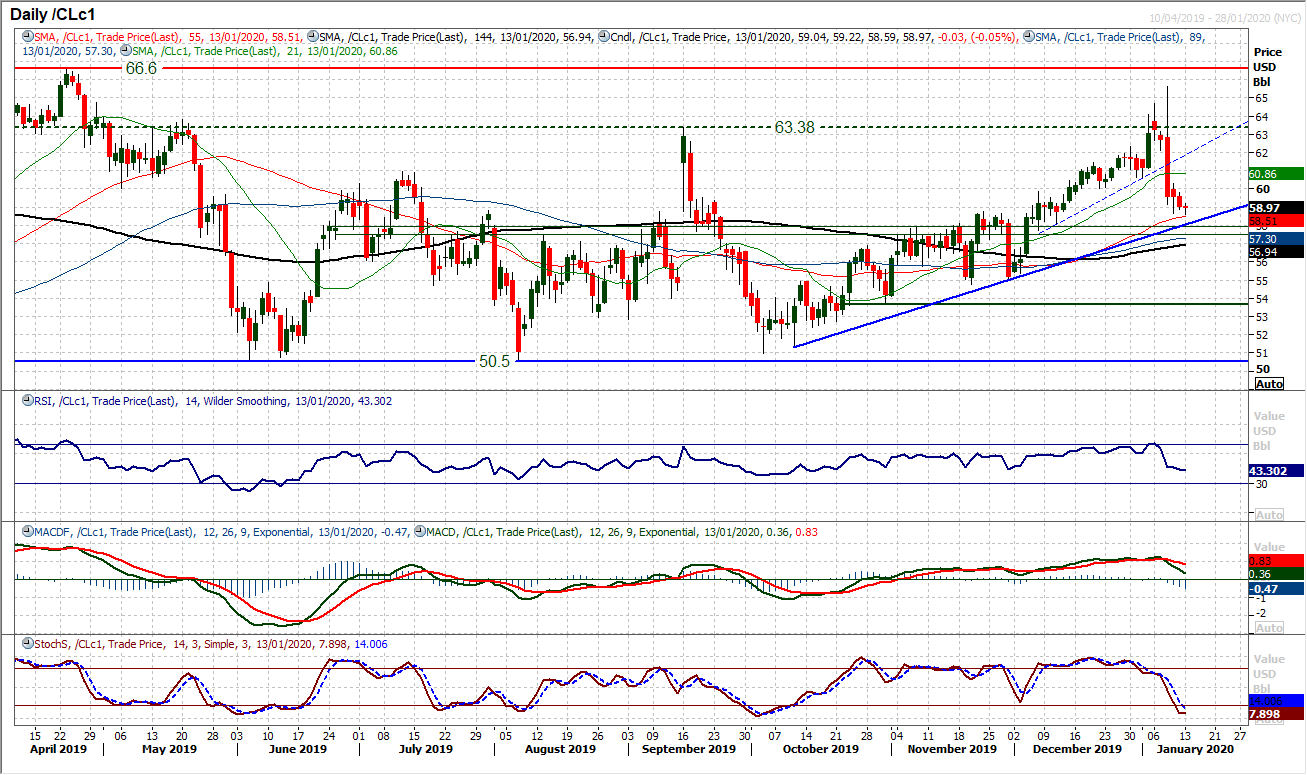

WTI Oil

WTI is still unwinding back towards medium term key support levels as the retracement from the big bull run has continued. Coming into this week though there is a band of old pivot support that the bulls will be looking at between $57.50/$57.85. There is also the support of the three month uptrend (around $58.00 today). This is therefore an area where the bulls will be looking at for the next higher low. Momentum has unwound back towards areas where the bulls have also previously built support (around 40 on RSI is prime). So to see the early positive rebound off $58.60 today will be encouraging, but the move needs to push back above initial resistance around $60.00 to really take a positive outlook again. We are still confident of the medium term positive outlook on oil, but support needs to form soon. Below the 144 day moving average (at $57.30) would breach all realistic support levels, whilst below $55.00 is bearish again.

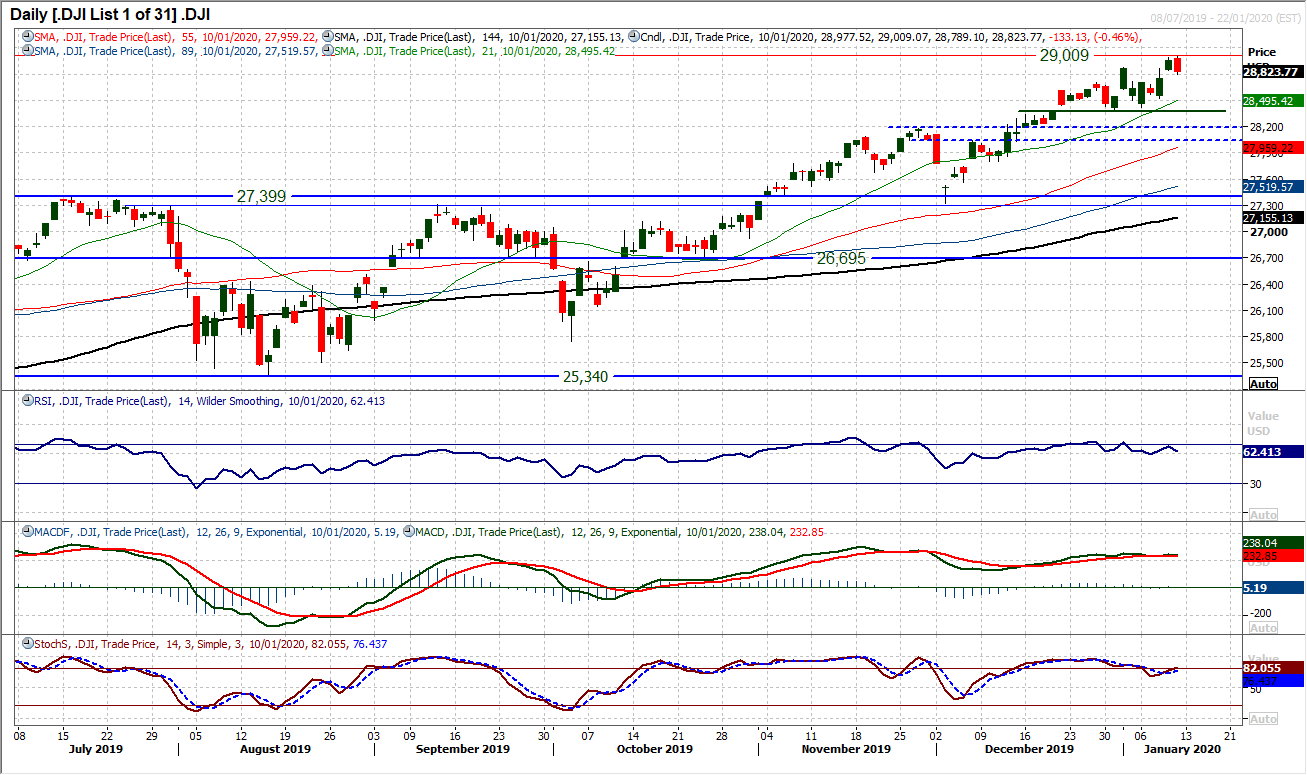

Dow Jones Industrial Average

The slightly softer than expected payrolls data on Friday resulted in a mild slip back on the Dow. The session was a bearish engulfing candle (and bear key one day reversal) which means that we need to be a little be more cautious in the coming days. Whilst this is not a chart that screams correction, the negative candle on Friday is a near term drag on the outlook and warning sign for a correction. The late December support at 28,376 is the key near term support of note and whilst this is intact there is little that the bulls need to be overly concerned by. A near term slip would even likely be considered to be a buying opportunity. For now, momentum is still positive (without being exceptionally strong), with the RSI in the 60s, along with MACD lines looking positively configured. There is certainly a case for a near term correction now, back from a traded all-time high of 29,009 on Friday.

Author

Richard Perry

Independent Analyst

Richard Perry, Independent Market Analyst, has over 20 years of experience working in financial markets in London.