Rising Household Leverage: Should We Be Worried?

Executive Summary

Some advanced economies have experienced increases in household leverage and household debt servicing ratios (DSR) in recent years. With many central banks beginning the process of normalizing their respective policy stances do these economies face a risk of stalling if debt servicing among households shoots higher? Could growth in the global economy be threatened again?

Our analysis suggests that any such concerns are probably premature. Some countries, notably Australia, Canada, Norway and Sweden face some risk of weaker growth in consumer spending due to higher debt servicing ratios for households. However, these four countries are hardly the most important economies in the world. In our view, household leverage seems to be a story for individual advanced economies rather than a systemic threat to the global economy.

Household Leverage Has Risen in Some Advanced Economies

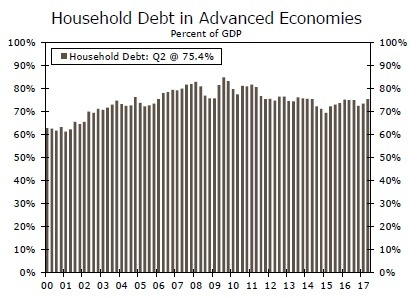

As is widely known, a build-up in household debt, not only in the United States but in some other major economies as well, led to the global financial crisis of 2008. As shown in Figure 1, the household debt-to-GDP ratio among 17 advanced economies rose from about 60 percent at the turn of the century to more than 80 percent in 2008. The ratio has subsequently trended down to 75 percent, but progress among individual economies has been uneven.

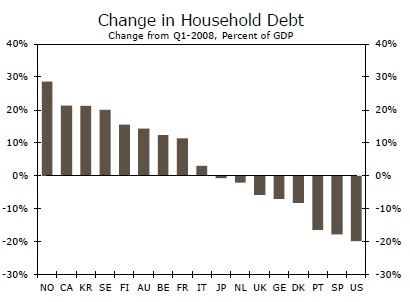

Since its peak in early 2008, the ratio in the United States has receded by roughly 20 percentage points (Figure 2). The comparable ratio in Spain (SP), which experienced its own housing bubble a decade ago, has declined nearly as much as the American ratio. However, a number of countries have seen their household debt-to-GDP ratios rise over the past decade. The ratio in Norway (NO) rose to more than 100 percent in Q2-2017 from 73 percent in early 2008. Canada (CA), South Korea (KR) and Sweden (SE) have all experienced increases in their respective ratios of 20 percentage points or so over the past nine years. Ratios in Finland (FI), Australia (AU), Belgium (BE) and France (FR) have also risen markedly over that period.

This increase in household leverage in some of the advanced economies of the world over the past decade begs an interesting question: could the global economy be setting itself up for another recession due to excessive household debt? This question is especially pertinent now that many central banks are starting to remove policy accommodation. The Federal Reserve has led the pack with 125 bps of rate hikes over the past two years. However, other central banks are starting to tighten their own policy stances. Notably, the Bank of Canada has jacked up its main policy rate 75 bps since July, and the Bank of England lifted its bank rate 25 bps in November.

Not only could higher interest rates dent consumer spending via their depressing effect on interest rate-sensitive spending (i.e., automobiles and other durable goods), but rising debt-servicing costs could siphon off income that could otherwise be used for purchases of goods and services. Could these rate hikes, and potentially more to come, cause consumer spending to buckle in some advanced economies in the foreseeable future? Which countries would be most susceptible to weakness in consumer spending via higher interest rates?

How Sensitive Is Household Debt Service to Rising Rates?

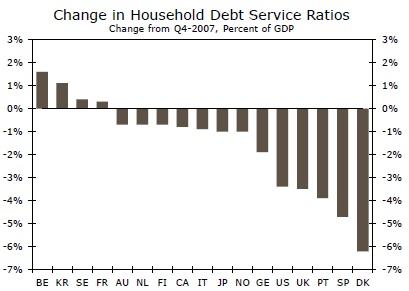

Fortunately, the marked decline in interest rates since 2008 has given consumers in most advanced economies some breathing room in terms of lower DSRs.1 For example, the DSR in Denmark (DK) has dropped more than 6 percentage points since its peak in 2008 (Figure 3). Not only did monetary easing reduce Danish interest rates—the National Bank of Denmark cut its discount rate 450 bps between November 2008 and July 2012—but Danish households have de-leveraged somewhat over the past decade (Figure 2). The same dynamics (i.e., monetary easing and household de-leveraging) led to a 3.4 percentage point decline in the household DSR in the United States.

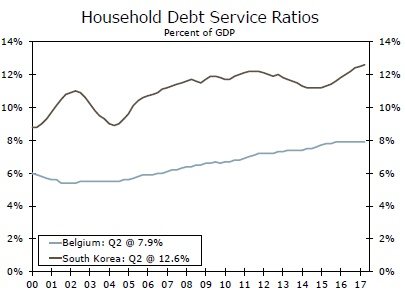

However, some countries have experienced an increase in their household DSR. Specifically, the DSR in South Korea (KR) has risen by more than 1 percentage point since 2008, and the comparable ratio in Belgium (BE) is up nearly 2 percentage points over that period. Household DSRs in Korea and Belgium currently stand at their highest levels since at least 2000 (Figure 4). Sweden (SE) and France (FR) have also seen increases in their respective DSRs since 2008.

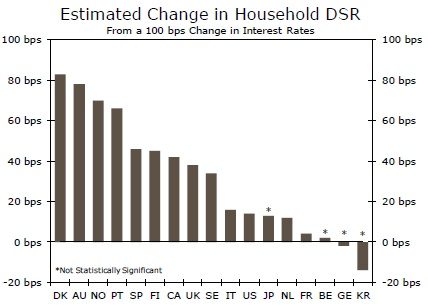

To ascertain which economies may be the most susceptible to rising DSRs from higher interest rates, we performed econometric regressions for the 17 advanced economies in our sample.2 Our regression results are portrayed in Figure 5, and they show how much the DSR in each country responds over four quarters to an increase of 100 bps in interest rates. Denmark (DK), where we estimate that the DSR increases 83 bps after interest rates rise 100 bps, has the most sensitivity among the 17 countries in our sample to changes in interest rates. Denmark is followed closely by Australia (AU), Norway (NO) and Portugal (PT) in terms of the interest rate sensitivity of their DSRs. In contrast, the United States has a relatively low sensitivity, with the household DSR rising only 14 bps when interest rates increase 100 bps.

The high interest rate sensitivity of household DSRs in the aforementioned countries makes intuitive sense because the vast majority of household debt in these economies has variable rate structures.3 In contrast, American households have low interest rate sensitivity because most mortgages, which account for two-thirds of household debt in the United States, have fixed-rate structures.

Which Countries Are Most at Risk to Rising Rates?

Based on Figures 2, 3 and 5, Sweden (SE) seems to be the country that is most at risk to a rising interest rate environment. Not only have households in Sweden become more leveraged in recent years, but the household DSR has trended higher and household debt in Sweden has a fair degree of sensitivity to rising interest rates. Other countries that stand out as potentially at risk include Australia (AU), Canada (CA), South Korea (KR), Norway (NO), Belgium (BE) and France (FR). Each of these economies has some combination of increased household leverage, a rise in its DSR since 2008, or sensitivity to rising interest rates.

Let’s start with Belgium and France. Both countries have experienced increases in household leverage and household DSRs in recent years. However, our econometric results suggest that households in each country have low sensitivity to rising interest rates. Moreover, the European Central Bank is not likely to hike rates anytime soon.4 Consequently, we do not think that consumer spending in Belgium and France is at high risk of buckling due to crowding out by higher debt service, at least not in the foreseeable future.

Korea appears to be facing a bit more risk than Belgium and France. Like their Belgian and French counterparts, Korean households have increased their leverage and they have experienced a rise in their DSR. Furthermore, many analysts look for the Korean central bank to tighten modestly in coming quarters.5 That said, the Korean DSR appears to have low sensitivity to changes in interest rates, so the outlook for consumer spending in Korea does not seem to be threatened unduly by rising rates.

In our view, Australia, Canada Norway and Sweden face the highest risk of deceleration in consumer spending due to crowding out from higher debt service. In each of these economies, household leverage has risen in recent years due largely to the marked run-up in house prices that each country has experienced. In addition, the household DSR in each country has a fair to a high degree of sensitivity to rising rates, which appear to be headed higher in each country, if only slowly.6

Conclusion

At the beginning of this report, we mused about whether the global economy is setting itself up for another recession due to excessive household debt. In our view, any concerns regarding that potential seem to be premature. Yes, some countries, notably Australia, Canada, Norway and Sweden, face some risk of weaker growth in consumer spending due to higher debt servicing ratios for households. However, these four countries are hardly the most important economies in the world.

The financial position of households in the United States, the world’s largest economy, has improved significantly over the past 10 years and American household debt is not very sensitive to changes in interest rates. Japan and Germany, the third- and fourth-largest economies in the world, respectively, have also experienced reductions in household leverage and household DSRs in recent years. Furthermore, the Bank of Japan and the ECB likely will not be tightening their respective policy stances anytime soon. In sum, household leverage seems to be a story for individual advanced economies rather than a systemic threat to the global economy.

Author

Wells Fargo Research Team

Wells Fargo