US may be headed for a V-shaped recovery

- Riots could assist US recovery by ending the economic paralysis

- Demonstrations will speed the end of social distancing and business restrictions.

- Urban riot damage will need a huge repair budget.

- Statistical evidence points to an April economic bottom.

The US economy may be headed for a V-shaped recovery aided ironically enough by the demonstrations that have made nonsense of the continued social and business restrictions and the riots whose damage will require massive spending to repair.

Whatever the public health issues Americans will likely resume their normal lives at an ever increasing clip. It makes little sense to permit huge crowds to gather and mingle, precisely the type of behavior that had been outlawed, and then tell business that their livelihoods are dangerous to the public.

Although much of the repair will initially be undertaken by the owners of the looted and destroyed properties, public assistance from Washington and the states will be probably be forthcoming. Either way the burst of economic activity will resemble the rebuilding after a major hurricane but spread across a wider swath of the country.

Consumption and the return of economic life

As people leave hibernation and return to activity there is a huge amount of deferred consumption that will resume. From haircuts to personal training, from doctor visits and elective surgery to manicures and dog grooming, the rise in business revenues will encourage hiring and in turn boost consumer spending.

Automobile sales nearly vanished over the past two months. Have all of the folks who needed or wanted new cars now decided to wait out the potential second wave? Not likely. Consumption carries an emotional charge that is its own reward and many people will seek it out.

The American consumers’ habits of several generations are not going to disappear because of a transitory and induced economic slowdown. The longer the resumption of life goes on the stronger the drive will become.

Behind the consumer and businesses are the assistance and loan programs from the national and state governments and the Federal Reserve. Their purpose is not to dig and fill the proverbial ditch of Keynesian theory but to enable the resumption of normal economic life. The money does not have to create activity, the machines and businesses are idle waiting for permission to start.

Statistical evidence of the May turn

Statistical evidence that April was the bottom comes from initial and continuing jobless claims, ADP payrolls, PMI surveys and probably this Friday's NFP report.

Initial jobless claims are forecast to fall to 1.8 million in the May 29 week their lowest level since the viral crisis began almost three months ago. Continuing claims which unexpectedly plunged 3.86 million in the week of May 15 to 21.052 million are forecast to fall to 20.050 million.

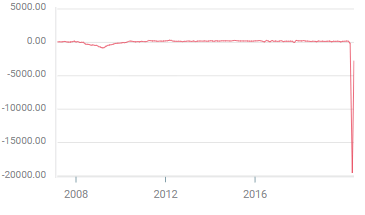

Private payrolls from ADP, the precursor to this Friday’s NFP report, fell 2.76 million in May, less than a third of the 9 million forecast and the April loss was revised down to 19.557 million from 20.236 million.

ADP employment change

Non-farm payrolls are projected to lose 8 million positions in May after April’s 20.5 million collapse, but NFP like jobless claims could be better than expected given the magnitude of the miss in the ADP forecast.

Business surveys from the Institute for Supply Management have lifted from their April lows. The manufacturing purchasing managers’ index registered 43.1 up from 41.5. The new orders index rose to 31.8 from 27.1 and the employment index edged to 32.1 from 27.5.

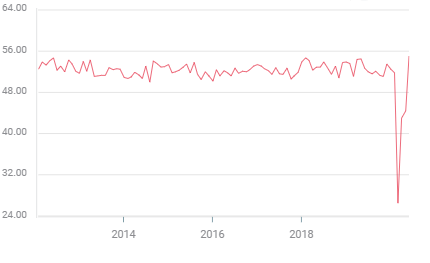

Services showed greater life with the overall PMI rising to 45.4 in May from 41.8, and new orders jumping to 41.9 from 32.9. Employment inched to 31.8 from 30 in April.

Services new orders PMI

While the employment indexes remain deeply in contraction hiring is normally the last indicator to improve in a recovery as firms wait to be sure conditions are better before increasing payroll costs.

Conclusion: Market convictions

Equity and currency markets have priced in a certain and rapid return from the shutdowns that have ravaged the US economy.

The Dow and S&P 500 were ahead 2.05% and 1.36% on Wednesday and are down just 7.95% and 3.34% respectively on the year.

The dollar has surrendered its risk-aversion premium with all of the major pairs at or close to their pre-crisis levels.

Yields in the Treasury market have also jumped with the 10-year up seven points on Wednesday to 0.761%, its highest close since April 8 and the 2-year higher by three points to 0.200% its best finish since May 1.

And finally there is China whose May Caixin purchasing managers index jumped to 50.7 in manufacturing. The services score of 55 ended three months in contraction that began with 26.5 in the virus month of February, the lowest reading in the eight years of the series.

Caixin services PMI

If China has succeeded in quelling the pandemic and reopening its economy there is every reason to expect the West will also.

The hardest estimate to make in economics is the one for Keynes’ animal spirits, the emotion that provides hope and confidence in the future. Betting against the US consumer has long been, in the British phrase, a mug’s game.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.