Reserve Bank of Australia Rate Decision Preview: Two makes a cycle

- The Reserve Bank of Australia (RBA) is expected to cut the cash rate 0.25% to 1.0%

- 1.0% would be a record low for the RBA base rate

- Unemployment and GDP are the bank’s primary targets

- US/China trade dispute is the unsettling background

The Reserve Bank of Australia will announce its decision on the cash rate at 2:30 pm AEST am in Sydney, Australia, 4:30 am GMT and 12:30am EDT Tuesday July 2nd.

RBA: A new easing cycle

The RBA’s second rate cut in as many months, and together the first in almost three years are likely to be followed by others as the bank tries to stimulate the Australian economy in the face of ebbing domestic and global growth.

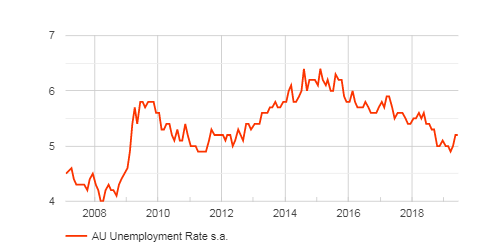

Governor Phillip Lowe had previously said that April’s 5.2% unemployment rate which continued into May and declining GDP indicated that little impact is being made on the extra capacity in the labor market. Unemployment has risen from 4.9% in March which was an eight year low.

FXStreet

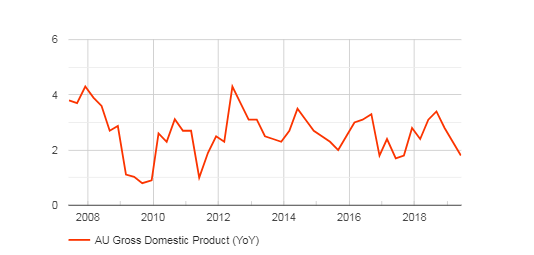

Australian annual GDP averaged 2.9% in 2018 but has been on a steady down path for nine months. From the second quarter high of 3.4% it dropped to 2.8% in the third, 2.3% in the fourth and 1.8% in the first three months of this year.

FXStreet

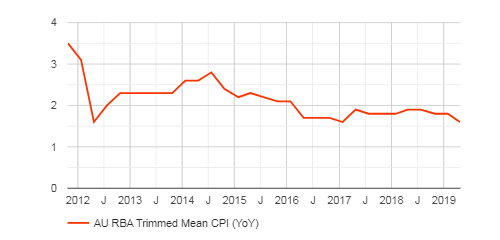

Inflation has also stayed stubbornly low having fallen from 1.9% year over year in the first and second quarters of last year to 1.6% in the first period this year.

FXStreet

Central Bank Uniformity

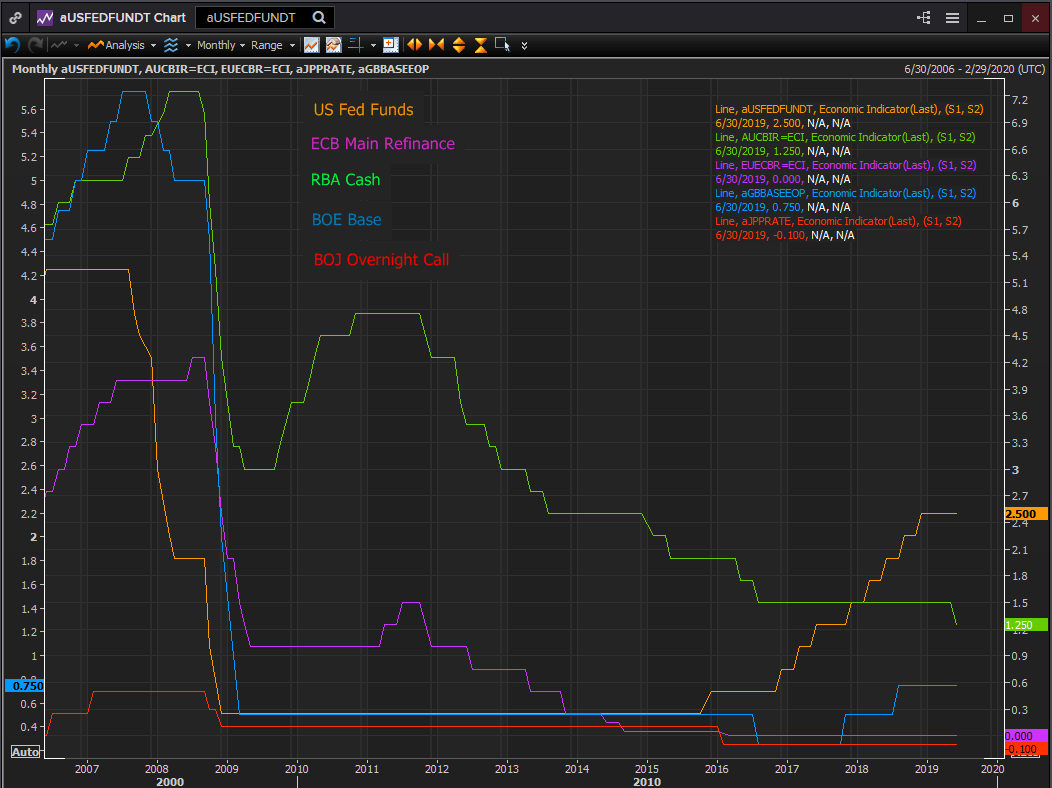

Every major central bank has joined the lower rate procession.

The RBA and the RBNZ have cuts rates. The Federal Reserve is widely expected to do so at the end of this month having moved to an easing bias in June. The Bank of England said at its last meeting that rates could now move either way, which might seem equivocal but it replaces a tightening policy. The ECB President Mario Draghi said last month that the bank could cuts rates or provide other liquidity should it become necessary. The bank’s main refinance rate is already at zero. But even if the ECB governors move to a negative main rate they would not be the first, the Bank of Japan’s overnight call rate has been at -0.1% for more than three years.

Zero rates: economic logic vs. empiricism

In the aftermath of the financial crisis the world’s central banks adopted a monetary policy of, in Mario Draghi’s famous words, “Whatever it takes.” He was referring to preserving the euro but in order to save the euro he needed to save the European economy, hence zero rates.

Reuters

For central bankers and their institutions who are often viewed as careful custodians of their economies the policy choices are surprisingly few. In fact they are not few but one: interest rates.

The response to the financial crisis and recession was uniform reduce rates as far and as fast as possible and by whatever means necessary.

But the bankers soon found that getting lower was not the same as being lower. The stimulus effect of bringing rates to below 1% was not the same as keeping rates that low for long periods of time.

The economies operating under the supposed economic gift of extremely low rates did not accelerate, they continued along an indeterminate path, moved higher and lower by other factors largely ignoring the historically miniscule cost of funds. Low rates became the background against which the industrial economies conduced business, a background that the bankers were fearful to change lest they precipitate a recession. Rates at the zero bound had lost their ability to promote economic growth and the bankers had lost their confidence that their economies could function without them.

Only the US Federal Reserve, the originator of quantitative easing, acted to return rates to a more normal environment. Throughout the three year effort to raise the Fed Funds upper target rate from 0.25% to 2.5% none of the traditional catalysts for a tightening campaign, rising inflation and wages and an overheating economy were present. The Fed governors persisted and now that the world’s central bankers are again worried about preserving growth, the Fed has more ability to effectively stimulate the US economy than any other industrial nation’s central bank.

The RBA may lower its cash rate to 1% and beyond. But the problems of the Australian economy do not stem from a restrictive monetary policy.

Perhaps the RBA governors should ask the Bank of Japan about efficacy of interest rates below 1%. Japan first instituted them more than 20 year ago. They are still in place.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.