Relentless flattening of the yield curve and Powell accelerated the move

An intraday stock market rally attempt failed again today and the intraday selloff in bonds reversed as well to more flattening at the long end.

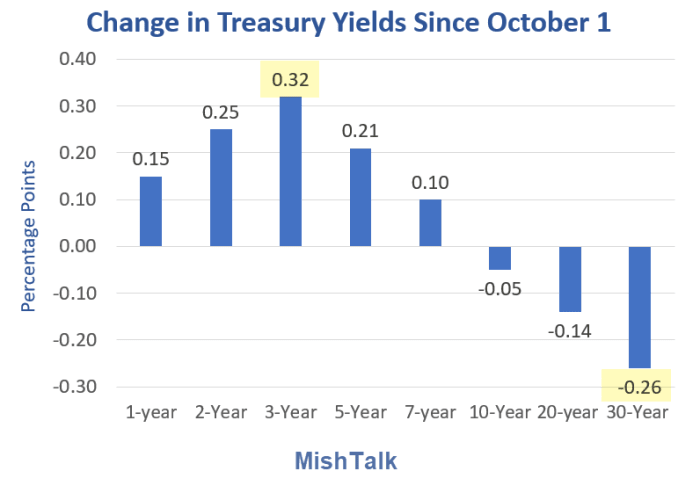

October Change Synopsis

- Since October 1, the yield on 3-year notes has gone up 32 basis points.

- The yield on the 30-year long bond has fallen 26 basis points.

- That is a relative flattening of 58 basis points, over double two quarter point rate hikes.

Powell Congressional Testimony

Yesterday, in testimony to Congress, Fed Chair Jerome Powell expressed concerns over inflation.

He also stated it was appropriate to consider wrapping up tapering a few months sooner. Previously, the Fed's tapering target was June 2022.

Interesting Bond Market Reaction

Yesterday I commented Stocks Decline as Powell Warns of Higher Inflation and Accelerated QE Tapering

The stock market reaction is what I would have expected on the above news.

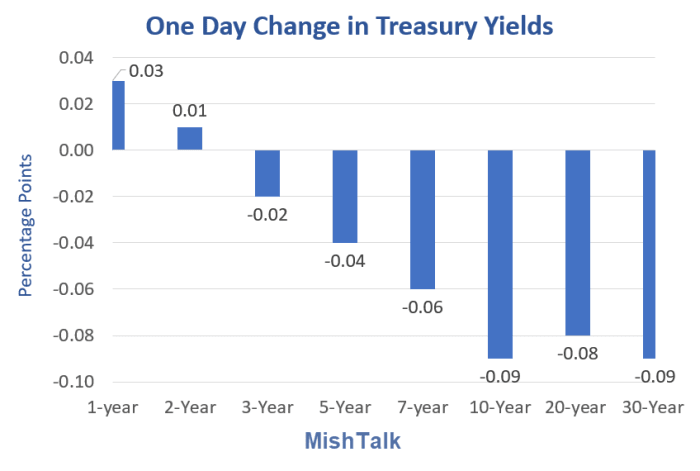

The bond market reaction is far more interesting. Yields at the long end tumbled and rose in the middle.

Given news that the fed would taper (end QE expansion) sooner and then start hiking rates sooner, one would have expected a stock market decline (and been correct).

But if the economy was strengthening, bond yields would normally go up across the board. They didn't.

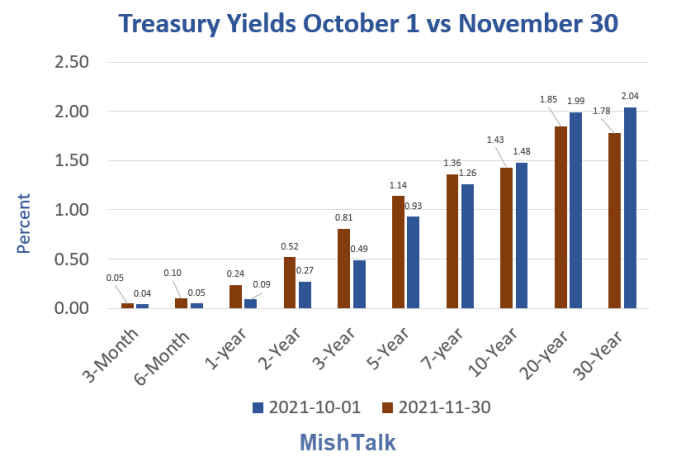

Treasury Yields October 1 vs November 30

The lead chart shows the relative change and the speed at which things are happening.

Retiring the Phrase "Inflation is Transitory"

After insisting for over a year that inflation was transitory, Powell finally decided to throw in the towel.

This brought out some amusing observations from economist David Rosenberg and others.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc