Record close for DJIA, S&P500 and Facebook Inc

Market Recap

|

Market Recap |

% |

Close Price |

|

DJIA |

0.37% |

22956 |

|

USDJPY |

0.33% |

112.19 |

|

USDCHF |

0.11% |

0.9756 |

|

USDZAR |

-0.61% |

13.3972 |

|

XAUUSD |

-0.82% |

1285.12 |

|

USDMXN |

-1.28% |

18.78 |

Prices as of previous day instrument closing.

-

DJIA and S&P500 made another record close while Nasdaq Composite lost 0.35 points at 6,623.65 and could not close above Monday close. S&P500 gained 1.72 points or +0.07% at 2,559.36 and was overperformed by the DJIA as it rose 40.48 points or 0.18% and closed less than 3 points below the psychological area 23,000 at 22,997.44. The CBOE VIX index however rose 4.04% as the index closed at 10.31. The rally seen on equities was not systematic as the Advancing/Declining on NYSE, AMEX and Nasdaq was not impressive: 35.2% issues advanced while 58.2% declined. Another interesting data is the number of issues above their 50 daily moving average. Actually 27.9% of the companies listed on NYSE, NASDAQ and AMEX are trading below their 50 MA. If this data would decrease even gauges would make new highs the rally would have a more idiosyncratic weight than a systematic one and could be an alert regarding overbought levels. The S&P500 and DJIA are up for the 9th consecutive quarter while the Nasdaq Composite is up for the 7th consecutive quarter. At the moment bullish expectations on Q3 corporate earnings, the new tax plan that should trim corporate tax to 20% are keeping market sentiment high. US President Trump is expected to choose the new FED Chairman before the 3rd of November.

-

The US Dollar Index rose for the second consecutive session and it closed at 93.48. EURUSD slid but closed above its intraday lows. USDJPY rose while USDCAD was quite volatile because the Loonie dollar lost ground during the European session but it recovered after new hopes for a NAFTA deal. MXN was not correlated with other EM currencies as thanks to a possible NAFTA deal it soared against the Greenback while ZAR,TRY and RUB slid. Volatility on CAD and MXN however is expected to stay high .GBPUSD dropped for the second consecutive session but a government that is divided does not have good probabilities to have successful negotiations with the EU. This factor could offset the expectations of a rate hike in November.

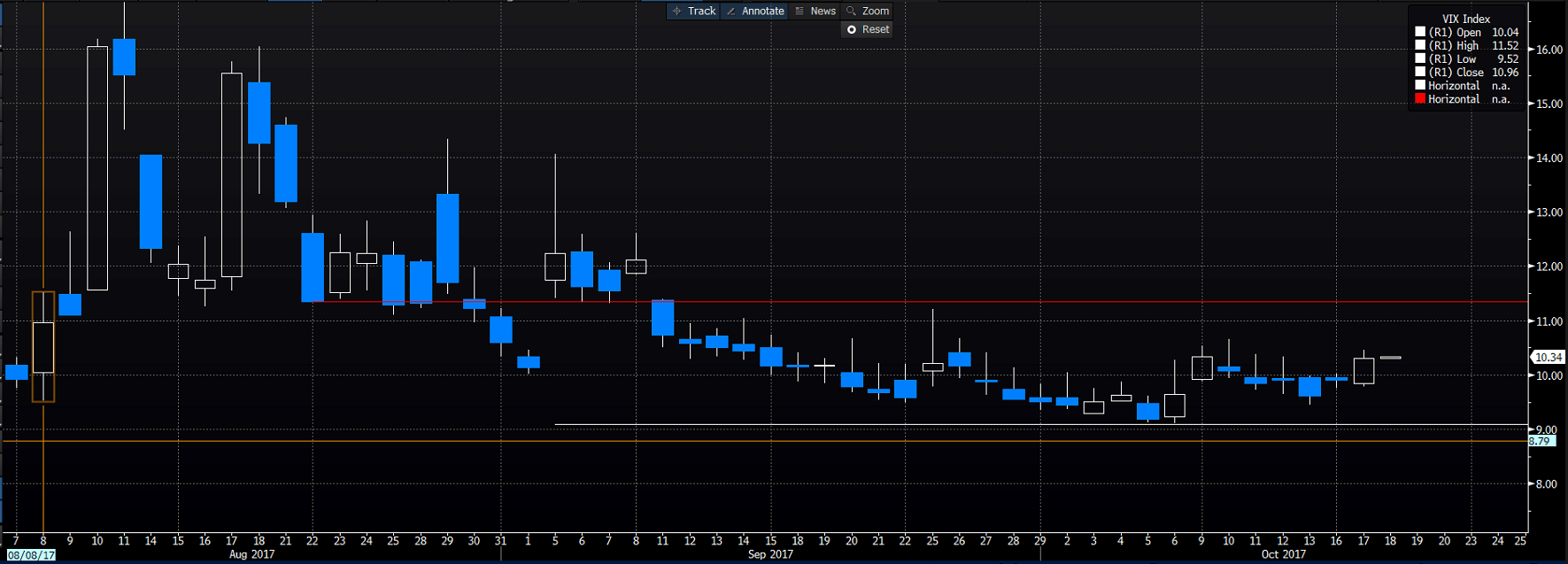

Chart of the day:

CBOE VIX Index

The CBOE VIX Index is compressed in a tight range of 2.20 points. In case it should make new lows it means that implied volatility of S&P500 options would collapse again. A breakout of the higher band could be linked to expectations of a retracement in the stock market.

Economic Calendar and Today Session (CET Time)

|

Wednesday October 18, 2017 |

Forecast |

Previous | ||

|

10:10 |

EZ |

ECB President Draghi Speaks | ||

|

10:30 |

GB |

Average Earnings 3M/YOY (Aug) |

2.1% |

2.1% |

|

10:30 |

GB |

ILO Unemployment Rate (Aug) |

4.3% |

4.3% |

|

14:00 |

US |

FOMC Member Dudley Speaks | ||

|

14:00 |

US |

FOMC Member Kaplan Speaks | ||

|

14:30 |

CA |

Manufacturing Sales (Aug; MoM) |

-0.3% |

-2.6% |

|

14:30 |

US |

Housing Starts (Sep) |

1175K |

1180K |

|

14:30 |

US |

Housing Starts (Sep; MoM) |

-0.4% |

-0.8% |

|

14:30 |

US |

Building Permits (Sep) |

1245K |

1272K |

|

14:30 |

US |

Building Permits (Sep; MoM) |

-2.1% |

3.4% |

|

16:30 |

US |

Crude Oil Inventories (Oct 13) |

-4.242M |

-2.747M |

|

20:00 |

US |

U.S. Federal Reserve Releases Beige Book | ||

China’s Communist Party starts its Congress today, which takes place only once in 5 years, ending on the 24th of October. While a shift in leaders is set to take place, President Xi Jinping is likely to strengthen his position. Investors should watch this event for any clues regarding future economic policy.

With UK headline inflation hitting a 5-year-high at 3% yesterday, an interest rate hike has become increasingly likely. Should the labour market data at 10:30 CET come in positive, it is unlikely that the BOE would not decide to increase the interest rate on the 2nd of November.

In the afternoon, FOMC members Dudley and Kaplan discuss economic development. Housing starts (14:30 CET) have been in a downward trend the past few months. The figure could have some upside risk to it as post-hurricane data is likely to lift future releases.

The Fed is releasing its Beige Book at 20:00 CET. It is interesting to watch this release to pick up any judgements on a lacking inflation figure. Average hourly earnings showed a strong reading for September and the members could thus have more confidence in meeting the inflation target.

Technical Analysis

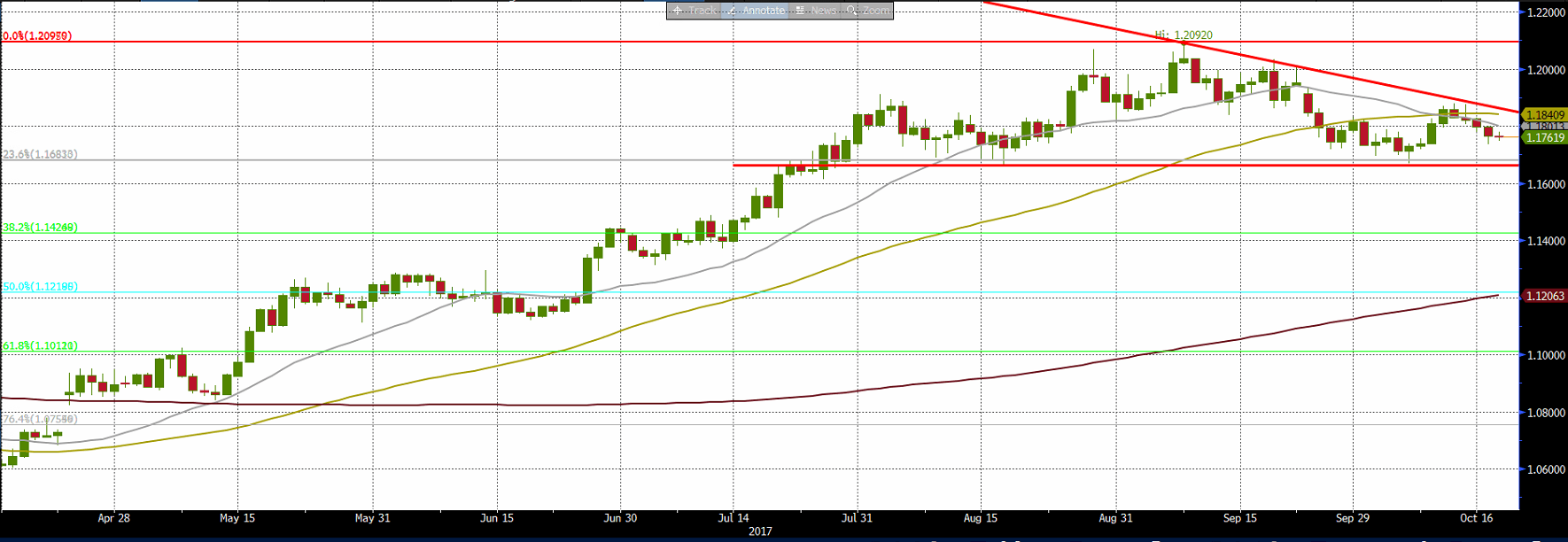

EURUSD (Daily timeframe)

The pair could test soon the medium term support at 1.1665. Beneath this level it may slide to 1.15 and then to 1.1425, the 38.2% Fibonacci Retracement of the bullish wave started at the beginning of this year. A breakout of the dynamic resistance could lift EURUSD to 1.20 and then to its 2017 top 1.2092.

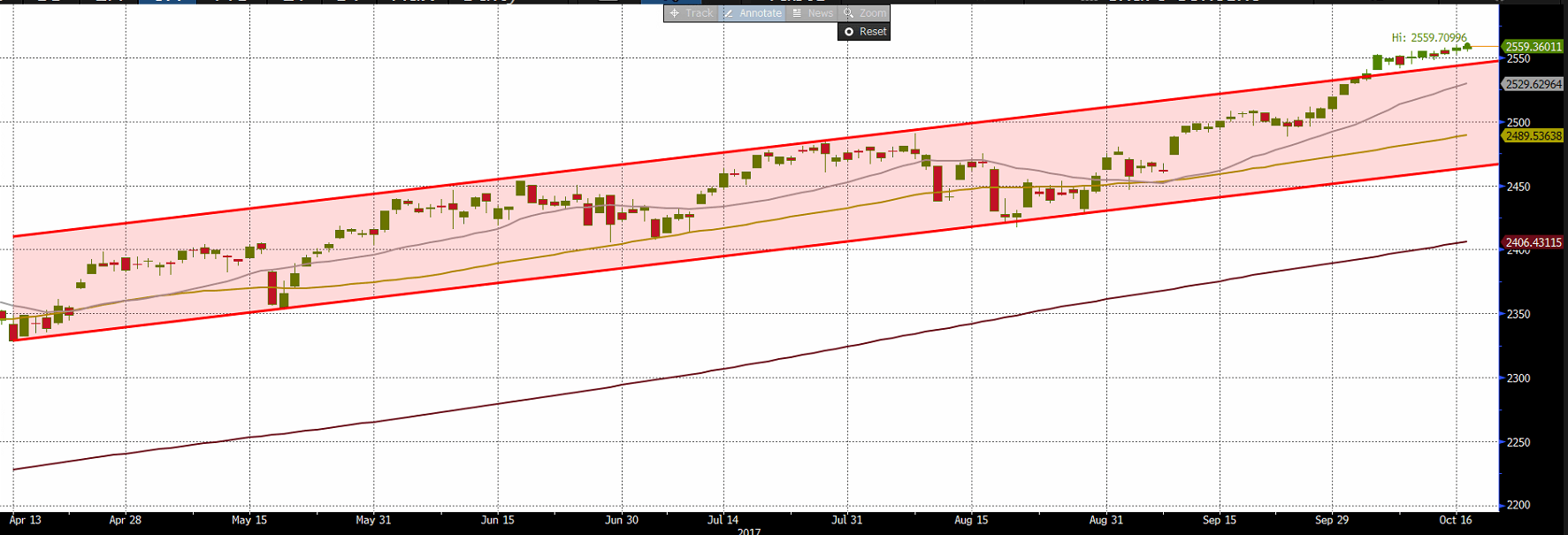

S&P500 (Daily timeframe)

The index made a breakout of the higher side of the bullish channel of medium term. In case it would retrace in the channel it could slide to 2,529 and then to 2,489. Important support is the lower side of the channel, now near 2,470. In case the gauge would continue to rise it could test 2,600 and then 2,630. This level is the price projection of the channel width.

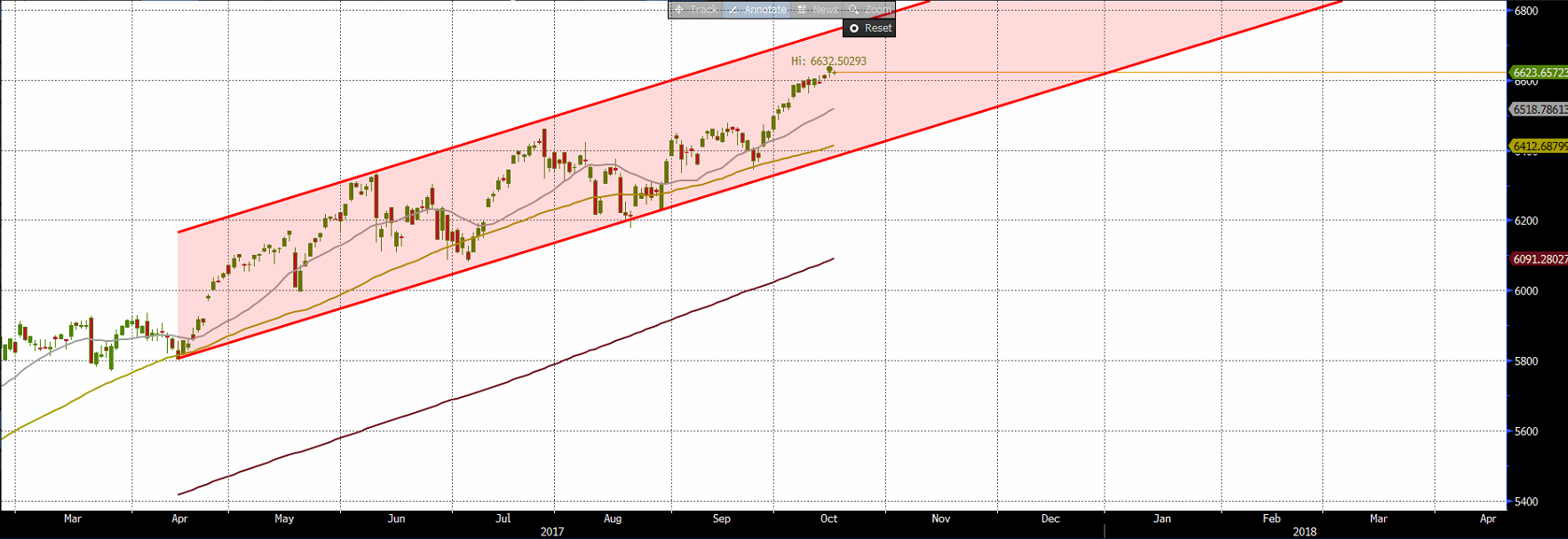

NASDAQ COMPOSITE (Daily timeframe)

The gauge is still in its medium term bullish channel and could test its higher side, now at 6,746. In case a breakout it will materialize the price projection level is at 7,000. In case of a retracement the index can find support near 6,500 and then at 6,400. Beneath this area selling pressure would increase and NASDAQ COMPOSITE could test its 200 MA, now in area 6,091.

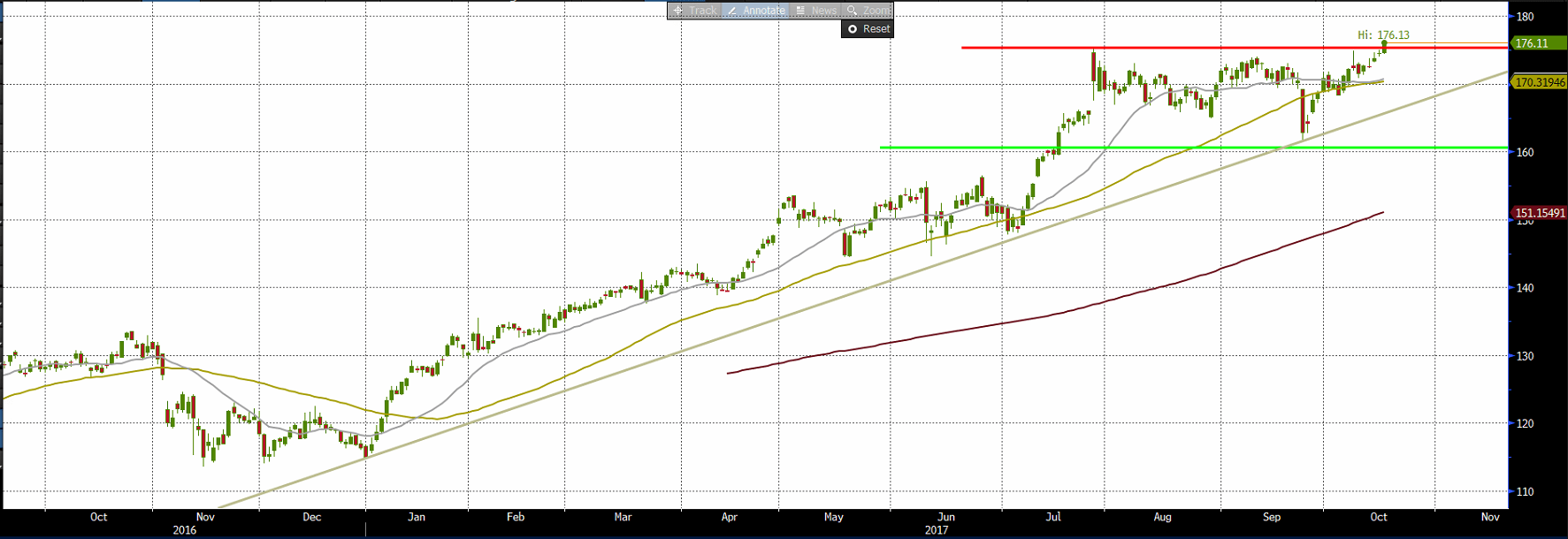

FACEBOOK Inc. (Daily timeframe)

The company founded by Mark Zuckeberg made a record high and could reach 180 and then 192. Psychological test in area 200. Support near 170, and below 160 it could slide to test its 200MA, now at 200.

Author

ALB Team

ALB Forex Trading

ALB Research Department is the research department of ALB Forex Trading Ltd.