Recession cancelled but Fed keeps strangling

The tariff recession is cancelled, but with the Fed strangling rates, we are nowhere near the boom Trump wants.

So say a pair of heavyweight numbers that dropped last week: GDP and jobs.

GDP came in at a very respectable 3% -- which is solid boom territory.

Meanwhile, private sector jobs hit a hundred forty thousand on the month -- reversing the previous month's 23,000 loss.

More importantly, those jobs are coming with very tame inflation -- despite tariffs -- with Truflation notching inflation at 2% on the nose.

GDP’s tariff whipsaw

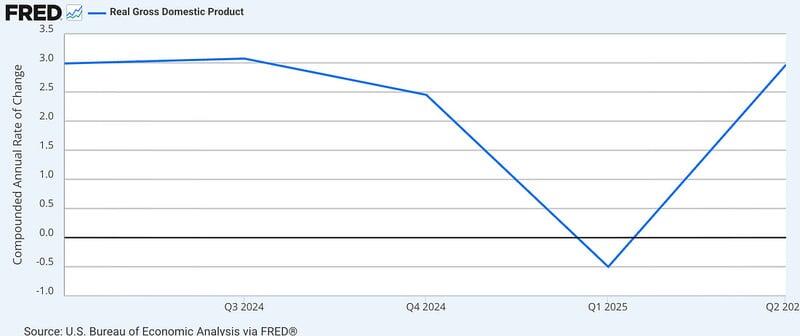

Both were closely watched after GDP turned negative in the first quarter. Back then, the media wet themselves over the Trump collapse. But at the time I mentioned, the numbers were driven by a huge surge in imports to beat Trump's tariff clock.

The way GDP's counted imports are negative GDP -- the idea is to avoid double-counting when the stuff's eventually sold. But it makes the GDP numbers dirty when you get a big surge.

And so, as expected, it reversed in Q2.

This makes it tricky to know what's actually happening. You could just average the two, which gives GDP growth of 1.25% -- which is very weak.

Or you could use Personal income, which measures actual earnings. That's humming along, logging a 3% growth rate.

For perspective, in Biden's last 3 years, disposable income was running just 0.9% per year.

So, going by GDP, we're crawling. Going by personal income, Trump tripled growth.

Jobs slow

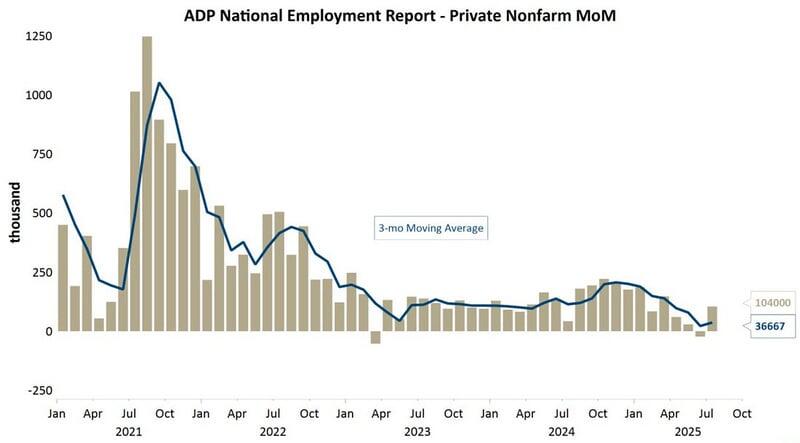

Beyond GDP, the other big number last week was jobs, which rebounded to a positive 104,000 on the ADP survey.

It was actually better than it looked since government-linked jobs — health, education, and of course government workers — dropped 38,000. While productive jobs actually grew by over 140,000.

Of course, the big caveat was the big BLS revision, where government statisticians knocked off fully one-third of jobs under Trump.

That would put jobs in the worse 8% of reports -- close to recession.

So, for different reasons, we don't exactly know what's happening -- imports are screwing up the GDP numbers. While BLS is screwing up the jobs numbers.

What’s next

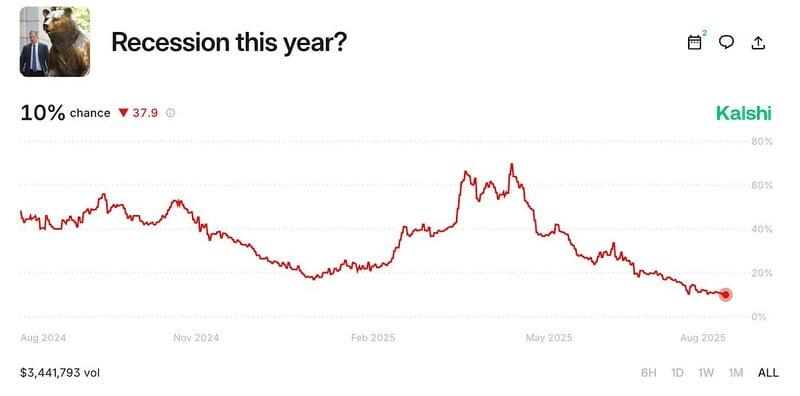

The easiest way to clear through the smoke is markets that crowdsource recession odds. Prediction market Kalshi is currently running just 10% odds of a recession this year.

Which is down from 53% under Biden.

And it's down from 69% in the worst of April's trade war.

Still, it's one thing to avoid recession; it's another to get the boom Trump wants.

Trump’s ticking the right boxes: tax cuts, deregulation. Deportations to raise wages. And at least bending the curve on federal spending compared to Biden, who tried to jack spending by 800 billion in his final budget -- almost triple what's happening now.

Still, the Fed's high interest rates are doing what they're supposed to do: strangle jobs.

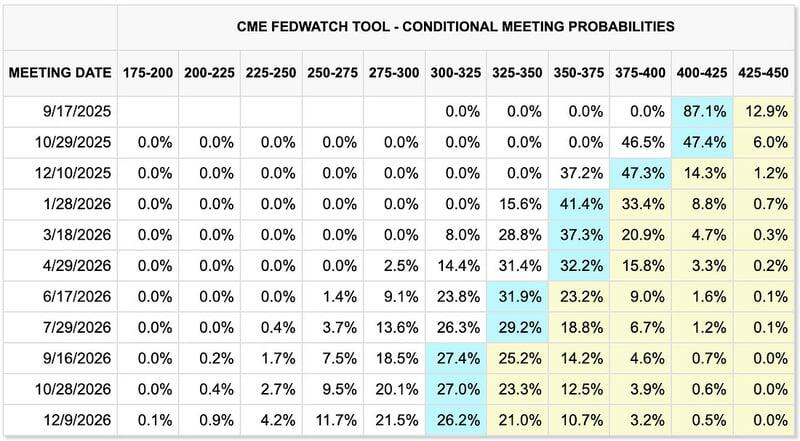

The BLS revision bumped odds rate cuts could start as early as September — see above.

But the Fed's still resisting imaginary tariff inflation. Meaning we could keep getting slow growth until Jerome Powell changes his ways, gets bullied into it, or leaves office next May.

Either way, the focus moves to Q3. The question being: did tariffs end up doing anything to inflation? Or do they continue barely showing up in the numbers, even as the media -- and the Fed -- desperately pray they do.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Peter St. Onge, PhD

Money Metals Exchange

Peter St. Onge writes articles about Economics and Freedom. He's an economist at the Heritage Foundation, a Fellow at the Mises Institute, and a former professor at Taiwan’s Feng Chia University. His website is www.ProfStOnge.com.