Rates Spark: When the hawks seem dovish

Rates remained under downward pressure, only this time it wasn't the US. The Bund curve bull-steepened as eurozone inflation was less hot than feared and the European Central Bank's Schnabel was seen as dovish. We are less certain that the odds of another hike in September can be dismissed as easily. But for today the focus is on US jobs.

Rates remain under downward pressure

US rates were still under moderate downward pressure, but for a change relatively quiet with the data yesterday largely falling in line with expectations. But markets were probably also gearing up for today’s payrolls release, one data point that has had the ability to shift market sentiment in the past.

More bubout his preference for a “Table Mountain” profile – he was speaking in Cape Town – for policy rates, rather than a “Matterhorn”.

EUR rates were also under downward pressure. Some of that was a relief that the aggregate eurozone inflation data did not come in as hot as feared after prior country releases had suggested upside risks. In then end the headline rate proved stable, but more importantly the core rate came down to 5.3% year-on-year. Mind you, that is still way above comfortable levels for the ECB.

When a hawk sounds dovish a closer look is warranted

Therefore, it was all the more surprising that ECB’s arch hawk Isabel Schnabel struck a more balanced tone than many would have expected of her. She continued to highlight the uncertainties surrounding the inflation outlook, but at the same time acknowledged that growth prospects had also deteriorated in the meantime. With regards to upcoming policy decisions she would not commit to any outcome, and rather stressed the data dependent approach. In more geographic terms: it’s elevated terrain but one can only look about 100m – it could be South Africa or the Alps.

The market went for the dovish interpretation, though we think that some of Schnabel’s assessments still point to her hawkish nature. For instance, she pointed out that under certain circumstances a hike could also “insure against the continued elevated risk of inflation remaining above [the ECB’s] target for too long”.

Yes, she refrained from making any prediction on rates. But she highlighted that the ECB not being able to pre-commit to any future action also means policymakers “cannot trade off a need for a further tightening today […] against a promise to hold rates at a certain level for longer”. This would close off one possible avenue for bargaining between the doves and hawks as the next steps are debated.

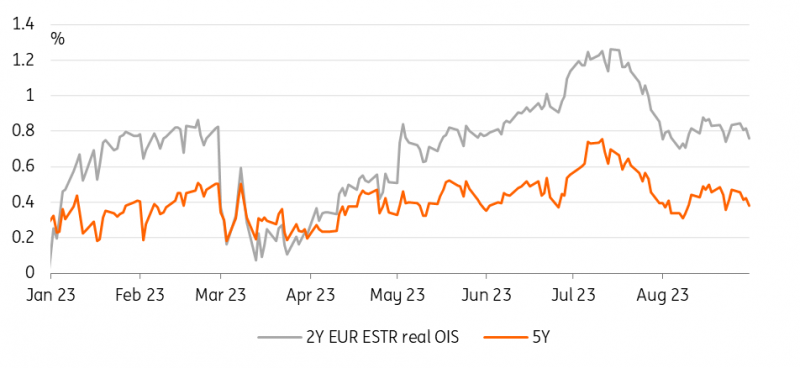

Finally, she also stressed the importance of real interest rates as a measure of the ECB’s effective policy stance. More specifically she cautioned that the recent decline in real interest rates “could counteract our efforts to bring inflation back to target in a timely manner”.

In the end Schnabel is but one voice, although an important one. The ECB minutes of the July meeting eventually also conveyed a slightly changed tone within the Governing Council – still very much concerned about inflation, but with doubts about one's own still very optimistic growth outlook starting to creep in. The market's pricing for the September meeting has slipped from previously discounting a greater than 50% probability for a hike to now around 25%.

The effective policy stance is not as restrictive as desired

Source: Refinitiv, ING

Read the original analysis: Rates Spark: When the hawks seem dovish

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.