Rates spark: Wake up call

A jump in US CPI today is well flagged, but it should be a wake-up call to what we think will be stickier inflation in the coming months, if not years. This would render the Fed's position increasingly stretched and the policy-sensitive 5Y sector has more room to cheapen. EUR rates are more supported near term, but the benign backdrop has an expiry date.

High US CPI print a wake-up call for what is to come

All eyes are fixed on today’s US consumer price inflation release, which our economists are expecting to jump from 1.7% to 2.4% year-on-year for March. More important though is that this may well be just the first of a string of elevated inflation prints. Our economists see, in particular, housing-related inflation components adding to the push higher in inflation towards 4% over the summer and crucially keeping it closer to 3% for longer.

This, in turn, should render the Federal Reserve’s current forward guidance of not raising rates before 2024 increasingly stretched. This puts the 5Y sector of the US yield curve, which is typically the most policy-sensitive, in the spotlight. With the timing of when the Fed initiates its rate hike cycle more likely to fall into the years 2022 to 2023 in our view, market rates in the 5Y sector have room to rise further and faster relative to the surrounding maturities.

And indeed, displays of optimism are progressively filtering through Fed officials' commentary, with Boston Fed President Eric Rosengren signalling the first hike could take place in two years' time. James Bullard of the Saint Louis Fed put down a similar marker, stressing the tapering debate could start when 75-80% of the population is vaccinated.

The valuation of the 5Y relative to 2Y and 10Y rates has retraced from its cheapest levels in the past few days, but we would view this as a temporary development, in part as markets built in a concession for this week’s US Treasury auctions. After the 3Y and 10Y sales went smoothly yesterday, markets still have to digest a US$25bn 30Y auction later today.

The supportive EUR rates backdrop has an expiry date

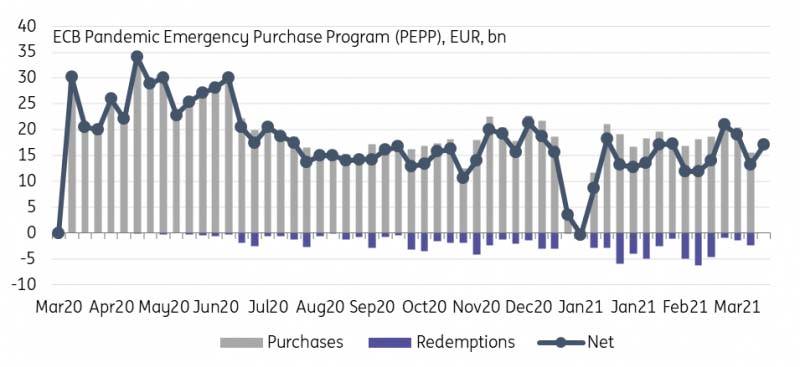

The ECB has bought a net €17.1bn of bonds under its Pandemic Emergency Purchase Programme over the past week. That is more than the €13.1bn in the week before but still below the €19 to €21bn in the prior weeks, after an increase in the pace of PEPP purchases was announced. In part, this is due to the Easter holidays which means that the ECB was effectively buying only on four days in each of the past two weeks. This week, redemptions may have led to a distorted net figure with Germany repaying a €21bn bond.

More important are the signals that have come from the direction of officials of late though. They have expressed little desire to let the higher pace of purchases run for longer than the three months that were announced at the last ECB meeting. While the current demand and supply balance - when taking into account the ECB’s higher purchases and seasonally larger bond redemptions - provides a supportive backdrop for eurozone rates, we think higher rates are in the offing here as vaccination efforts accelerate and Covid-19 gloom is about to be priced out.

ECB buying picked up again, but still low due to the Easter holiday

Source: ECB, ING

Today’s events and market view

Last week’s larger than anticipated jump in US producer price inflation to a 10-year high should have provided a warning shot, so the market's immediate reaction to today’s US CPI may be less impressive than a jump to 2.5% YoY (consensus) would suggest. The still looming 30Y UST later today could even see the long-end underperform, but eventually, we think that the more policy-sensitive 5Y sector on the curve should resume its underperformance.

The busy slate of eurozone bond supply could be another driver of long-end rate underperformance. Today’s sale of a new 15Y bond by the Netherlands (€4-6bn) had been well flagged. Yesterday, Spain also announced the syndicated sale of a 15Y bond while Austria announced a dual-tranche 4Y and 50Y deal. These are today’s new bonds which come on top of bond reopenings from Italy (up to €7.75bn) and a linker tap from Germany (€0.7bn). The data highlight in the eurozone is the German ZEW, which is seen to show further improvement.

Read more original analysis: Rates spark: Wake up call

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.