Rates spark: Under the thumb

Rates continue to feel the pressure from central bank purchases, pushing yields ever lower without a notable deterioration of sentiment. ECB purchase data confirmed more aggressive policies in July. The US 10yr's path of least resistance remains towards 1%. Only a quicker taper can change that.

The ECB steamrolled the EUR curve in July

There seems to be no let-up in the rally that is taking yields to new lows in somewhat illiquid summer markets. As ever, there is always a number of factors at play but we point to central bank intervention as a key driver behind the relentless drop in rates. The latest evidence came from the ECB, in the form of a trove of data relating to the execution of its QE programmes.

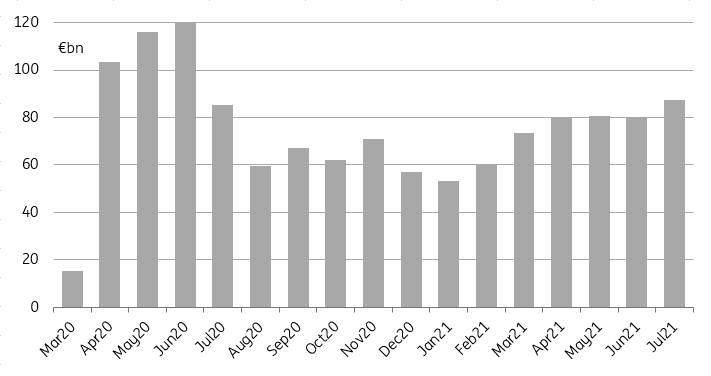

PEPP front-loading in July reached €7bn

Source: ECB, ING

Taking the largest of the two, pandemic emergency purchase programmes (PEPP), as an example, the ECB accelerated its purchases in the month of July. As we suspected, numbers suggest that it ‘front-loaded’ purchases in July before a decline in activity in August. Compared to the three previous months, the July increase was of roughly €7bn. Assuming it ‘backloads purchases in September by the same amount, it would allow it to carry out €14bn fewer purchases in August.

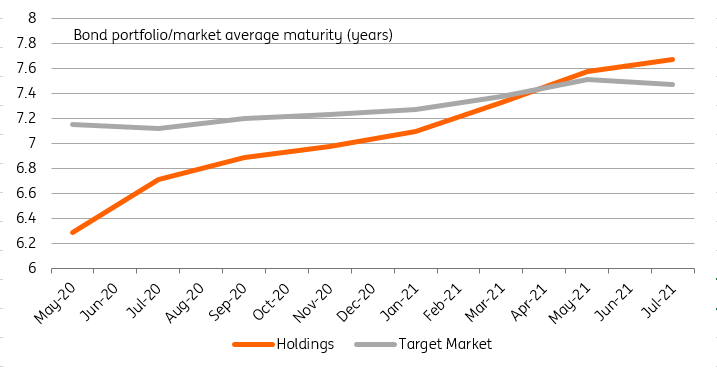

Another interesting takeaway is that the average maturity of public sector securities held in the PEPP portfolio has been rising steadily and now exceeds that of the universe of eligible bonds for the first time. When one takes into account the natural roll-down of existing bond holdings on the average maturity of the portfolio, this indicates a deliberate strategy to target long-dated bonds. Looking at the breakdown by issuers, it appears German and supranational bonds is where the most notable increases took place.

The maturity of bond holdings exceed that of the eligible market for the first time

Source: Refinitiv, ING

In the case of the former, we think it reflects a ‘catching up to the universe of eligible German bonds. In the latter, we think it suggests that new EU issues, which have a bias towards long-dated issuance, have been the main target of purchases. Both a front-loading of purchases and skew towards longer maturity would have been an additional factor suppressing yields, and flattening curves.

US 10yr at 1% remains the extrapolated target

Yesterday's US data came in broadly as expected. The PMI and ISM are headlined in the 60 areas. Prices paid are still very elevated (mid-80s), as are new orders (mid-60s), and the employment component has bounced back above 50. No reason whatsoever for the bond market to react to this, as all are close enough to prior expectations. Construction spending came in weak though. But still, in the scheme of things, not enough to cause a stir. In any case, macro data has not been a primary driver of rates lower in recent months.

The real driver has been excess demand for bonds and receivers, with the market in fact ignoring uppity data. It's causing issues as the approach to 1% for the US 10yr makes it tougher for the Fed to consider hiking any time soon, as they could prematurely invert the curve. We are some way away from that of course. A rapid taper is the real means to changing this dynamic, allowing the back end to get to more sensible levels. Until then the test lower continues with 1% still the logical extrapolated target.

A lower US borrowing target but some two-way risks

The US Treasury announced yesterday that it will borrow US$673bn in 3Q (a downward revision from its previous estimate), and another US$703bn in 4Q. These estimates are subject to considerable uncertainty as they assume the debt ceiling will be either suspended or raised. Any delay in doing so would reduce borrowing and force the Treasury to draw on its US$750bn cash pile, adding downward pressure to bond yields. It is not all downside risks, however. Infrastructure and new spending legislation being currently discussed in Congress could add to the need to issue debt, and relieve a market starved of safe assets.

Today’s events and market view

There will only be US data to watch today, in the form of factory and durable goods orders, not something we expect could upset the current status quo of falling yields in illiquid markets.

Austria will conduct the first euro government bond auction of the week, selling 5Y/10Y bonds.

Fed governor Michelle Bowman will be on the wires. Her colleague Christopher Waller argued in favour of tapering asset purchases 'early and fast'. His view differs from that of more cautious FOMC members but the spectre of tapering starting as early as October, with hikes starting in 2022 would light a fire under treasuries.

Read the original analysis: Rates spark: Under the thumb

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.