Rates Spark: The yield race to the top continues

US yields are rising across the curve but T-bills are at the intersection of a better economic outlook and a debt ceiling. Sterling rates are now offering a pick-up to dollar equivalents. This makes sense at the front-end but less so at longer maturities.

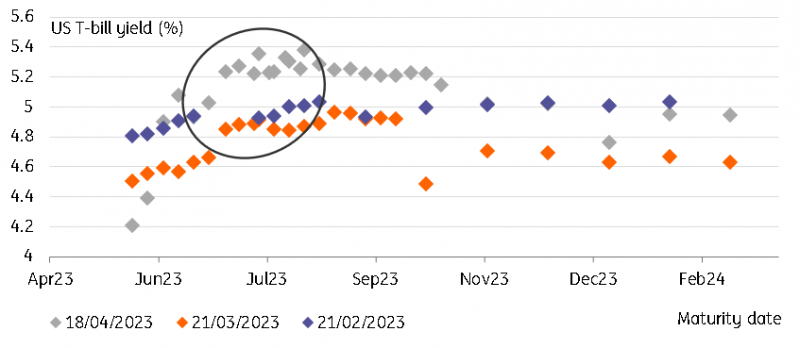

US T-bills at the intersection of the debt ceiling-recovery Venn diagram

US T-bills find themselves at the intersection of two uncomfortable developments. First, the longer time passes without any dramatic fall in economic data, the more the fear of a credit crunch fades in investors’ minds. Bank results so far this reporting season have failed to produce a recovery in the KBW US regional banks stock index but the broader bank stock gauge has shown clearer signs of a rebound. This is probably too early to sound the all clear but it is also fair to say that bank fears are no longer an impediment to higher front-end rates, and 2Y yields are still around 90bp below their each March peak.

The second development is the approaching debt ceiling showdown. There is a clear hump in the T-bill curve around the July-August maturity dates, when default risk is deemed most elevated. Information on tax receipts this week may help refine that estimate and so drive relative moves between securities. The fact is that ‘X-date’ is still roughly three months away, and so providing a precise estimate at this stage is challenging. The other driver is of course political developments but widespread expectation is for any solution to be found much closer to the deadline this summer.

Once a compromise is found, and it is our expectation that one will be found, T-bills face another challenge: the Treasury ramping up issuance to re-build a cash buffer in the Treasury General Account (TGA). As of last week, its balance was $109bn, but it is likely to go up this week thanks to tax receipts, before going down into the X-date. Assuming the Treasury aims to build its balance back to $500-600bn after the debt ceiling is solved, markets face upwards of $400bn in T-bill issuance, and a commensurate drain of liquidity.

The default probability 'hump' in US T-bill yields is moving forward to June

Source: Refinitiv, ING

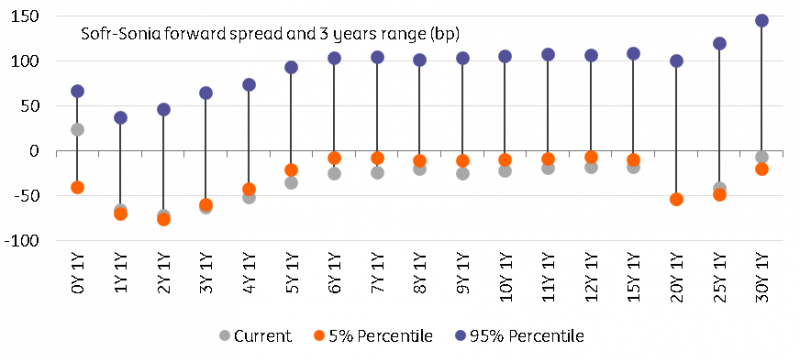

Gilts pick-up to treasuries widens

The re-pricing higher in US yields has been impressive these past two weeks and has widened the spread with euro rates, a development we think will prove short-lived once Fed cuts come into view. The sell-off in sterling bonds however has outpaced that of Treasuries, and that move accelerated with higher than expected wage growth in February. Clearly, the release, combined with core CPI failing to slow in March, increase the odds of a May hike at the Bank of England but market expectations have gone further than that. The Sonia swap curve now prices two more hikes in this cycle, more than what is priced by the dollar curve.

This has taken 10Y gilt yields at a higher than 20bp pick-up to the Treasury curve. Understandably, the pick-up offered by GBP rates is higher at the front-end of the curve. 5Y Sonia swaps are almost 50bp higher than their Sofr equivalent which we justify by the market’s greater conviction that the Fed is about to cut rates later this year. We agree that European policy rates, sterling rates included, will take longer to be cut. We find is harder to justify that longer-dated forward, for instance the 5Y GBP rate in 5Y is higher than its USD equivalent, by almost 30bp.

GBP forward swaps are higher than their USD equivalent at all but one maturities

Source: Refinitiv, ING

Read the original analysis: Rates Spark: The yield race to the top continues

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.