Rates spark: Real low

Record low real yields across the world betray an exceptional degree of macro angst. Or do they? Don’t look at rates in isolation. Other markets are fine. The tide of central bank purchases lifts all boats and normal liquidity conditions will only return at the end of the summer.

Low confidence is mostly a rates thing

In an otherwise quiet session, much attention will be paid to US consumer confidence but we expect most risk-taking to be reserved for after the more significant events later this week, namely the FOMC meeting, US Q2 GDP, and PCE deflator. Nonetheless, consumers’ outlook on the economy matters for the current market narrative, in particular with rates plumbing new lows in real terms. Risk assets on the other hand display none of the macro angst visible in bonds.

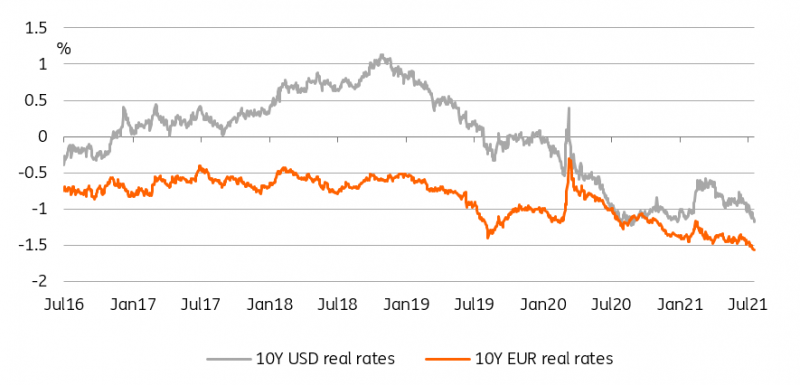

Central bank purchases lift all boats, resulting in record low yields

Source: Refinitiv, ING

Should consumer sentiment continue to be impacted negatively by higher prices, bond investors would see their doubt about the sustainability of the recovery vindicated. This in turn could conceivably reduce US rates’ ability to rise back as more liquid market conditions reassert themselves into September but we think liquidity factors play a greater role in driving the market. In the meantime, all bets are off, and we suspect the same causes (Fed purchases, lower liquidity, Covid-19 worries) will produce the same effect: low rates with little connection to economic reality.

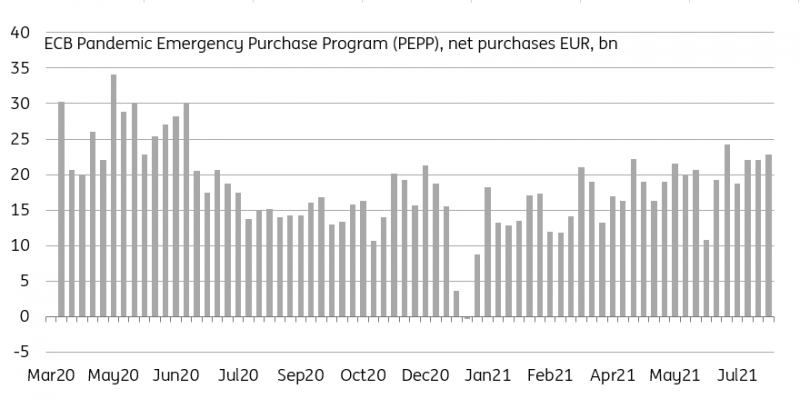

Higher ECB purchases hit yields particularly hard in poor liquidity conditions

Source: ECB, ING

To illustrate this point, for the third week in a row the ECB published weekly PEPP purchases in excess of €22bn. This implies a monthly rate in July that exceed the €80bn of previous months and could be a result of a front-loading strategy ahead of a further reduction of liquidity in August. Higher central bank purchases are a prime reason for low rates and flatter curves but a slowdown in August will not necessarily bring higher yields, due to a slowdown in supply. A more likely turning point in our view is when the September supply surge comes into view. In the meantime, rates could drop lower still, but don’t read too much into that.

Read the original analysis: Rates spark: Real low

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.