Rates spark: Rates ease lower, for now

The peak inflation narrative has allowed the market narrative to quickly move on to macro concerns. In the near term data and geopolitics provide a fertile ground for the bond rally to extend. Central banks are sticking to their guns however, and that may catch up with markets once the projected rate hikes are implemented.

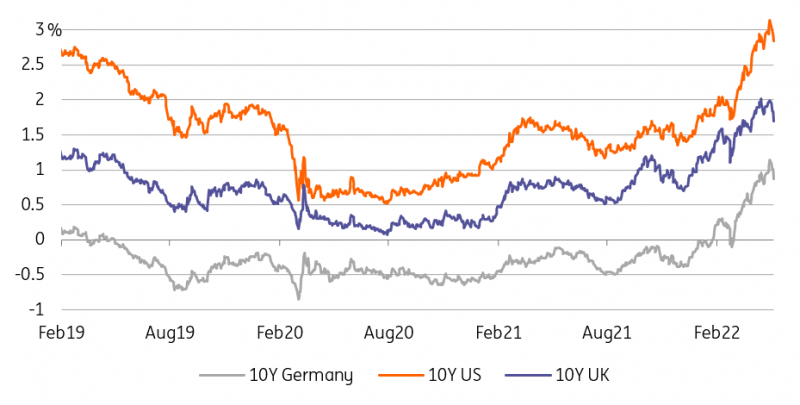

US inflation expectations continue to drift lower

The fall in the US 10yr yield continues to be driven by an easing in inflation expectations. Breakeven inflation in the 10yr is down to the 2.6% area. Remember this had been above 3% a couple of weeks before the FOMC. The fall in the 10yr Treasury market yield back below 3% has been driven by this. The 10yr real rate is also off the highs, and was the primary driver of higher market rates generally, basically since March.

Latest flows data show selling in inflation linked bonds, which fits with the notion that real rates are being driven higher while inflation expectations are drifting lower. These are the main themes in play right now, with the Federal Reserve likely pleased that inflation expectations have been drifting lower since the FOMC decision(s).

The narrative is shifting to macro concerns

The market focus is increasingly shifting to macro concerns amid more aggressive central banks. Risk assets are weaker and rates are further retreating from their highs with curves showing a tendency to flatten lately. Early days for the curve moves, and for now they pale in comparison to the volatility observed in outright yields.

After the important data releases and central bank meetings of the past week(s), it is a theme that may stick around for a while. The week ahead may feed into these worries. Tier one data may not feature on the data calendar, but the upcoming US housing indicators will put one possible weak spot of the US economy into focus. Perhaps not an immediate concern, but any whiff of weakness could fall on fertile ground.

European markets will follow the developments in connection with Russia. Gas supply disruptions, Finland’s NATO accession bid moving forward and a possible Russian retaliation offer enough potential for negative headlines.

Further abroad concerns over the development of the pandemic in China may keep risk sentiment on the back foot, as data out of the country on Monday is expected to show the impact of latest restrictive measures.

One, two, three, rejected: Bond rally catches on as the narrative shifts toward macro concerns

Source: Refinitiv, ING

... but central banks are sticking to their guns

The European Central Bank is still headed for normalisation, and it will take a lot to push it off course now. The forward overnight rate for the end of the year is still close to 0.2%, well into positive territory and in line with the recent shift of ECB communication. And indeed, with the release of the ECB minutes next Thursday we may get further insight into what prompted that sudden urgency within the Council to speed up policy normalisation. Markets are unlikely to be moved by hindsight, though.

But as we had suspected it is post normalisation trajectory that markets are starting to price shallower, with especially the 5Y sector softening further on the curve. Sticking with that sentiment, the current ECB speakers slate for the week ahead, featuring the Council’s doves Panetta and Lane, could underscore that sense of caution.

Rates have retreated from their highs and indeed our strategic view for the longer term horizon until year end is that yields will head lower. But we remain wary of calling the top of the cycle just yet. While we may now see an episode of markets reassessing the longer term outlook, central banks will still have to deliver on the anticipated tightening paths, the Fed is expected to ratchet up rates by 150bp in short succession over the next meetings, the ECB likely by 75bp before the turn of the year going by recent official comments. That can still gear overall rates higher, even if curves become flatter in the process.

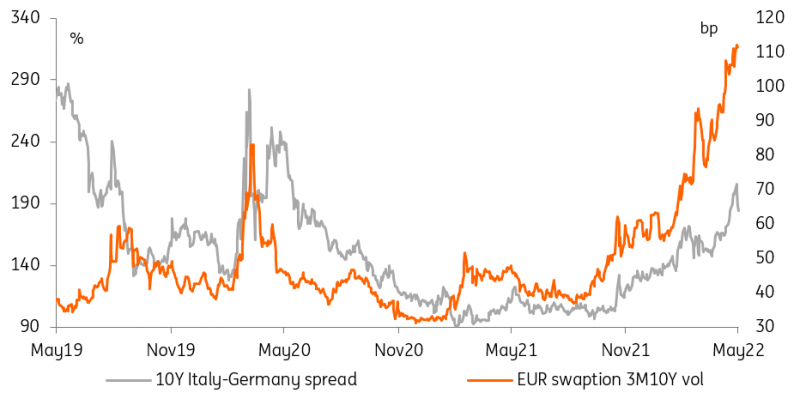

Italian bonds recover, bucking macro concerns and volatility

Source: Refinitiv, ING

Italian bond spreads over Bunds retreat further from the 200bp threshold

Scanning the riskier assets it is notable that within the European debt space Italian government bonds have actually started to outperform again. The benchmark 10Y Italy/Bund spread has further tightened back from its +200bp levels. However, we doubt the retightening marks the end of market concerns about Italian debt.

The retightening looks like a mechanical reaction to less aggressive pricing of the ECB trajectory. We would caution that the ECB is still set on ending asset purchases very soon and as of now communication suggests that the bar for any new tool to address a widening spreads remains high.

Equally the retightening of the Bund asset swaps spread confirms the directional nature of this spread nowadays rather than being a measure of stress and flight to safety as it used to be in the past.

Read the original analysis: Rates spark: Rates ease lower, for now

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.