Rates spark: Pre-meeting complacency

We expect pre-FOMC profit-taking on Treasury longs. The ECB shouldn’t take the calm in peripheral bond markets as a sign that QT is no big deal.

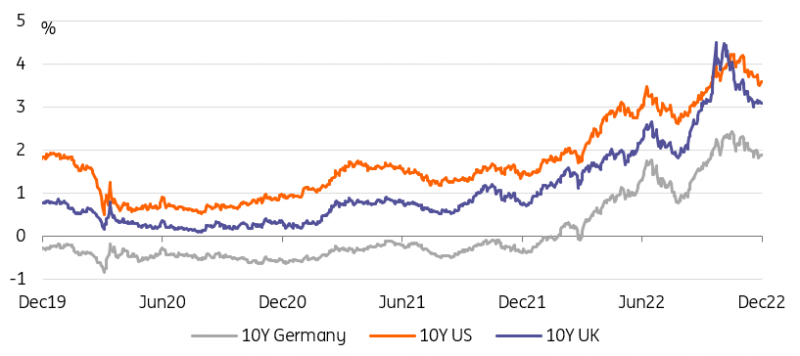

The treasury rally stalls at 3.5%

10Y Treasuries bounced on the 3.5% resistance level after a surprising rally that took them down 75bp from the 4.25% reached as recently as the end of October. The rally occurred with no encouragement from the Fed. On the contrary, the Fed has been at pains to stress that, if anything, it saw a higher terminal rate than in its September projection. Since then, data has been mixed, with a slowdown in various measures of inflation being balanced by still strong labour market indicators. What’s skewed market reaction in favour of a dovish interpretation to the recent data flow has been the Fed signalling a downshift to 50bp hikes.

Market participants may see a vindication of their recent dovish inclinations if US PPI does slow down on an annual basis as is expected in Friday’s release, but we feel the lack of other ‘tier one’ economics publications this week and the proximity of the 14 December FOMC meeting, suggest momentum towards lower rates has indeed stalled. We think 3% is a reasonable forecast for 10Y yields in 2023. The recent rally from 4.25% to 3.5% has taken rates more than halfway towards that level so we suspect many short-term investors will consider that the risk-reward balance of chasing the rally further is poor and will take profit. That profit-taking should mean yield will rise into next week.

The November rally has taken bond yields too close to our end-2023 forecast

Source: Refinitiv, ING

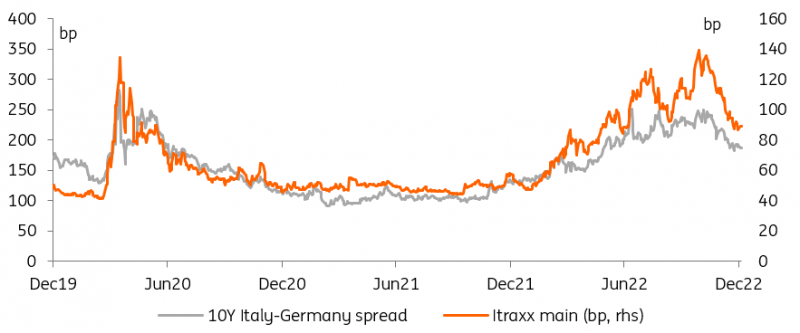

Calm in the bond market can breed complacency

The Fed is now in the midst of its pre-meeting quiet period, meaning we’re expecting no policy guidance until next Wednesday’s press conference. The ECB’s start on Thursday, which leaves two more days for its officials to skew expectations. So far, only a minority has pushed for a 75bp hike at the 15 December meeting, thus cementing expectations of a smaller 50bp move. Instead, focus has been on the timing and size of its bond portfolio reduction (QT), with little noticeable market impact so far. Indeed, 10Y Bund yields have rallied 50bp since their October peak, and 10Y Italy has outperformed them by more than 60bp.

Hawkish voices have pushed in favour of a QT start as soon as early 2023 with, for instance, Gabriel Makhlouf arguing for end Q1/early Q2 2023. Whilst we would expect QT to take the form of a progressive phasing out of APP (one of the two ECB QE portfolios) redemptions, Joachim Nagel said last week that markets were able to handle an abrupt end. We expect this view to be in the minority but it does illustrate an important point: it’s not just central bank policies that influence markets, the reverse is also true. The decreasing dispersion between euro sovereign yields has given the impression that QT is no big deal, and has emboldened the hawks.

Italy-Germany 10Y spreads standing below 190bp is probably below where most would have put them just one week before the ECB takes decisive steps towards unwinding its bond portfolio. This tool has been instrumental in compressing spreads, most would expect that its going into reverse would put widening pressure to spreads, even if the effect might not be felt immediately.

Sovereign and credit spreads have tightened into the ECB QT announcement

Source: Refinitiv, ING

Read the original analysis: Rates spark: Pre-meeting complacency

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.