Rates spark: Plot twist

Bonds quickly reversed their gains and look under further pressure from the goldilocks state of play across financial markets. There are risks to these not too hot nor too cold markets, however. A more hawkish Fed in today’s minutes is one. Hard US economic data point to a healthy 3Q but things should worsen in 4Q.

Banking on a dovish Fed carries risks

Bunds have tested the 1% yield level again after a 9bp round trip in two days. This is the proof that market moves in illiquid summer months, even more so due to bank holidays in some parts of Europe on Monday, should be taken with a pinch of salt. Bonds more broadly continue to trade weak with a bias toward higher yields evident since the start of the month. We attribute some of the move to better risk sentiment across developed markets, but risks to these goldilocks, neither too hot that central banks need to keep hiking nor too cold that the economy falls off a cliff, state of play abound.

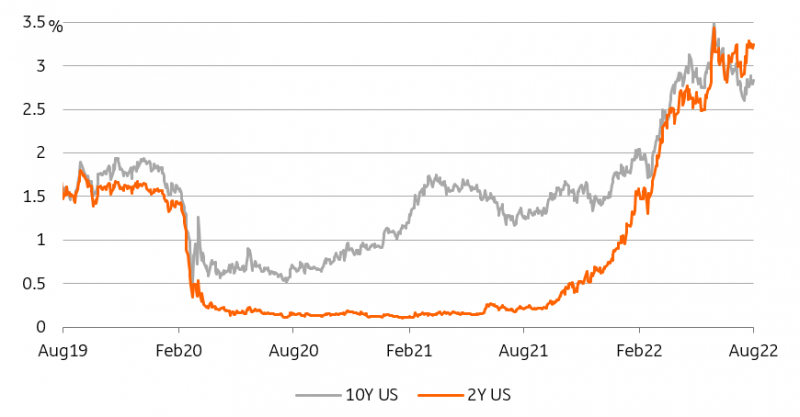

Hawkish FOMC minutes and strong retail sales could bump up the US yield curve

Source: Refinitiv, ING

The first and most obvious challenge is that central banks can ill afford a loosening of financial conditions as they still grapple with record high inflation. The Fed is clearly one example but by no means an isolated one. Tonight’s Fed minutes might well jar with the upbeat tone evident in many financial markets. Even if investors might be tempted to discount any hawkish concerns as ‘pre-CPI peak’, the tone of Fed comments since the July FOMC meeting leaves no doubt about their mood. This in turn should result in higher treasury yields, reaching above 3% again, and a softer tone in risk assets.

Both economic optimism and tighter spread look at risk

The discrepancy between soft and hard data in the US continues to drive some of the whipsaw in bond yields. Industrial production yesterday cemented our expectations for a solid 3Q GDP growth, and July retail sales, to be published today, should look equally solid. The contrast with sentiment indicators might only be a matter of timing however, with 4Q growth prospects looking a lot less healthy. It is difficult to imagine markets extrapolating this good stint of positive US numbers for long, with other corners of the economy, most notably housing, heading south.

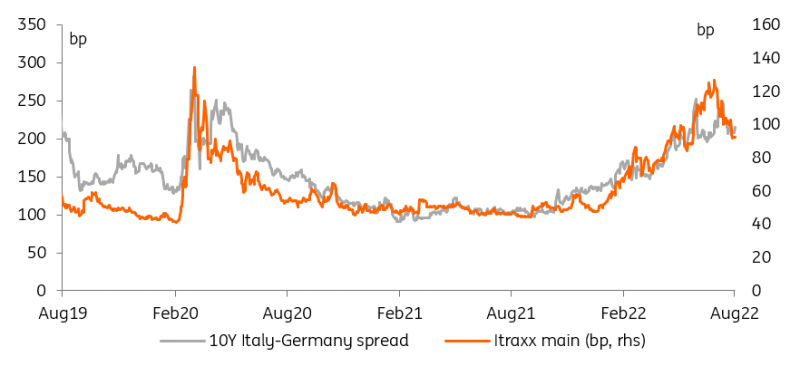

Risk of profit-taking in fixed income into the September supply window are rising

Source: Refinitiv, ING

Another risk is coming from the rise in government bonds themselves. Independent of the tone of central banks, rising core yields bring about wider sovereign spreads. This has been evident in the underperformance of peripheral bond markets this week with greater volatility in core yields also affecting demand for spread products. There is also a looming risk of a profit-taking into the September/October supply window after the gains registered over the summer months. This may not be the case yet but, in the case of sovereign spreads, some investors may well decide that they do not want to go into the last month of Italian election campaign with too much exposure.

Read the original analysis: Rates spark: Plot twist

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.