Rates spark: Playing chicken

The Fed should, but is unlikely to, send a strong signal on tapering. Even if these aren’t justified economically, low rates are a product of the squeezed summer bond market. This state of play is unlikely to change this week. EUR rates should prove more stable, but higher inflation could further weaken the ECB’s dovish rhetoric

Fed: Full speed in 2021, and slamming the breaks in 2022

This week will likely see the FOMC persisting in its game of macroeconomic chicken with inflation. Our economics team reckons that all this meeting will deliver is a further preparation for a tapering of asset purchases that will eventually be announced this December. Between here and then, the thinking goes, a very gradual shift in communication will prime markets for the end of QE, and allow the economy to clock more job market gains.

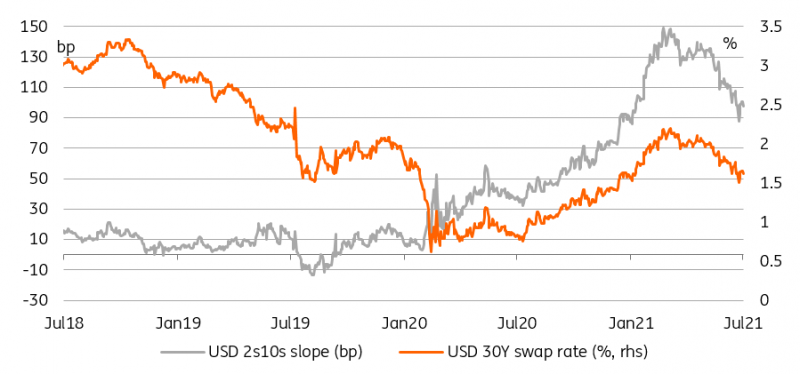

The Fed is still easing at full speed, resulting in flatter curve and lower rates

Source: Refinitiv, ING

This is a laudable objective but the subsequent policy tightening will prove a lot trickier to pull off. Our core view is that the $120bn/month bond purchases is to be reduced down to zero by the time of the first rate hike in September 2022, which will be followed by a second in December. To us, the Fed’s persistent dovishness in the face of persistent inflation is akin to a driver keeping their foot on the accelerator to only slam the break at the last minute.

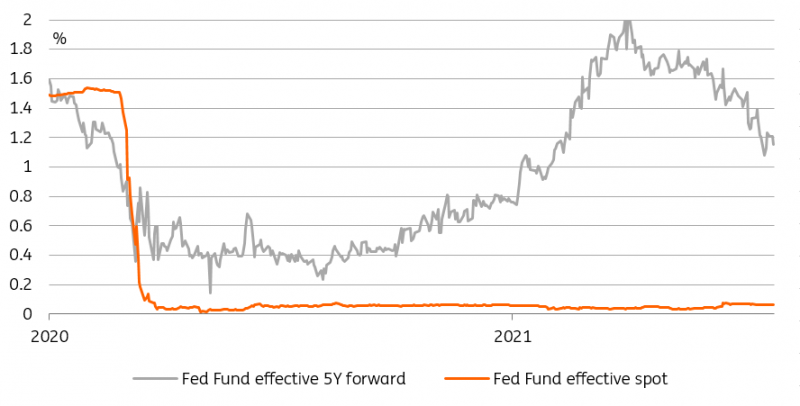

US rates in full delusion mode

These consideration are far from the rate market’s thinking. In recent months, yield curves have shaved nearly 100bp to the expected terminal Fed Fund rate, and also delayed the date at which they expect the first hike to occur. The temptation is great to take these at face value and conclude that investors anticipate a sharp slowdown in economic activity.

The curve has priced out nearly 100bp of hikes within 5 years

While there may some legitimate concerns about the spread of the Covid-19 Delta variant, these feel to us like an attempt to fit a story to the move. The drop in interest rates has at least as much to do with heavy-handed Fed purchases, constrained supply, and illiquid summer markets. If we’re right, then QE is as much part of the solution as it is part of the problem.

Supportive technicals in the near term but the case for owning Treasuries is poor

In the near term, only a change in the Fed’s communication surrounding QE could affect this state of play and, as we wrote above, we doubt the Fed will send a strong signal this week. Granted, there is broad agreement that current yield levels do not reflect economic fundamentals but, as we are still in the ascending phase of the current Covid-19 wave, we fear that appetite to fade the move on that basis will remain limited.

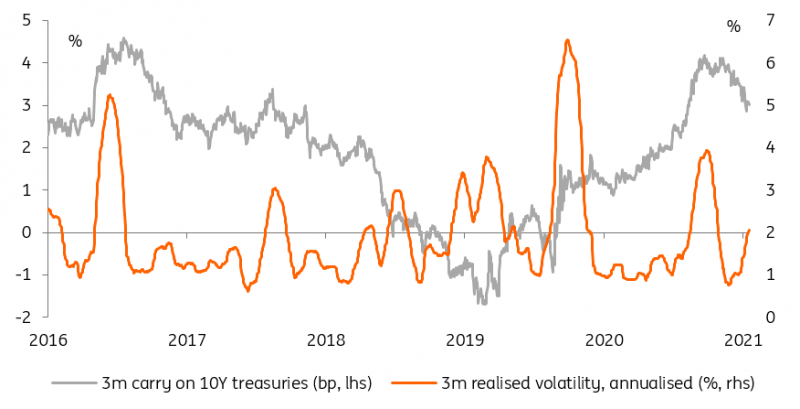

Higher volatility and lower returns, not a winning combination

Source: Refinitiv, ING

Yet the case for holding treasuries at this yield level is weakening fast. Not only is the carry benefit proportionally diminished, the jump in volatility means investors should demand a greater compensation for taking the risk of owning them. There could, of course, be a period of stabilisation at current levels. This, in our view, would require at least a month of anaemic price action. By this time next month, we expect market liquidity to have recovered, and for the September supply surge to come firmly into view, hardly a recipe for stable rates.

Read the original analysis: Rates spark: Playing chicken

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.