Rates spark: Pivot alert

Markets are smelling blood in the water, but do they have enough evidence to price a policy turnaround? Not yet in our view. The BoE’s reluctance to buy gilts is a sign that it hasn’t given up the fight against inflation.

Markets on high alert for a central bank pivot

The sight of a bond rally when investors smell a whiff of a central bank pivot is something to behold. The root cause of the recent re-pricing lower in rates can be traced back to two factors: the global economic slowdown and resurgent fears for financial stability.

The former is nothing new, and investors were wrong-footed by a surprisingly resilient US economy as recently as August, lending credence to the hawkish tone of the Fed, and by etension fo the Bank of England (BoE), and European Central Bank (ECB). The need for emergency BoE intervention in the gilt market last week has brought the latter to the fore. While most expected the dramatic jump in rates to translate into financial stress, the timing and location of the first crisis were difficult to predict with any degree of precision.

All this begs the question: is this really a turning point in central banks’ tightening cycles, or at least have tightening expectations gone far enough? Any answer to that question has to start with the Fed. There were signs last week that financial stress is starting to register in its consciousness, most notably with Lael Brainard’s speech on Friday, and with Thomas Barkin expressing concerns about the spillover of a stronger dollar yesterday.

Recent hopes of a pivot have been disappointed, however. Despite signs that a housing recession is already there, it is unclear whether economic circumstances have changed enough to prompt a policy change. Investors, however, may secretly be hoping for a slower pace of hikes going forward, or for Quantitative Tightening to be reconsidered. The RBA hiking only 25bp against a 50bp consensus overnight may well have reinforced these hopes.

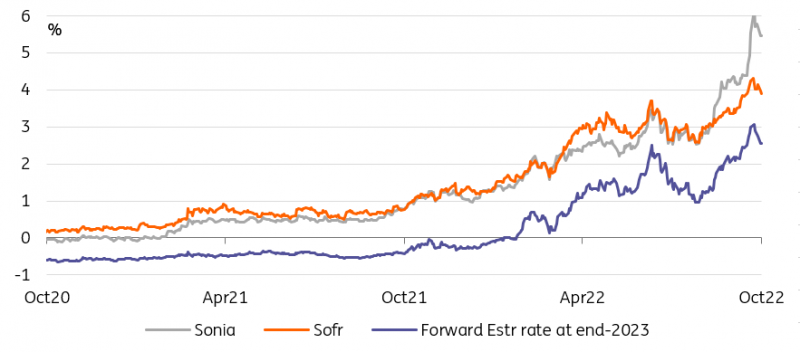

Swaps have pared back hike expectations as financial stress spreads

Source: Refinitiv, ING

BoE caution shows that the inflation fight isn’t over

A look at the UK can also be instructive, although the read-across to other central banks is admittedly more limited than for the Fed. Monday’s BoE long-end gilt buying operation only accepted anecdotal amount of offers amid the generalised bond rally.

To us, this is a strong signal that it sees its intervention as a backstop against market volatility, rather than a quantitative target. The result? 30Y gilts were the only developed market sector that ended the day with higher yields than on Friday. At the very least, this suggests that the central bank is wary of debt monetisation calls, or of the counterproductive effect of purchases in its fight against inflation. The fact that it will now request the identity of underlying sellers also indicates that it wants the program to remain targetted to pension funds.

The next few days might deliver additional information on how fast economies are slowing down or – more realistically – how widespread financial stress is. But, for the moment, we fear the bond rally is running short of tangible evidence of a change in monetary policy. Neither can the more than 20bp rally in 10Y Treasuries and Bund since Friday be attributed to safe-haven demand, given that stock indices ended the day up and credit indices tighter.

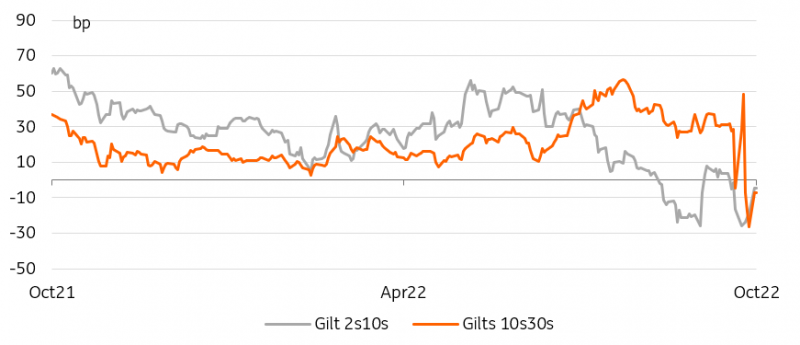

The gilt long-end steepened after more timid BoE purchases

Source: Refinitiv, ING

Read the original analysis: Rates spark: Pivot alert

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.