Rates spark: Pause and think

There are enough event risks on this week's calendar to afford at least a pause in the washout of US reflation trades. Powell could drop some tapering hints, and supply should help steepen the curve. If the ECB decides to update its forward guidance, lower rates will ensue however, and a flatter curve.

A more volatile start to the summer

Those hoping for a quiet couple of months did not start their summer on a very good note. We have argued in June that carry consideration would be tempting many investors to trade the market on the long/receiving side. Those who did probably saw their view vindicated by the move lower in rates, but not by a lack of volatility.

Our view was that long-end rates would lead most of the gains while short-end rates would remain elevated due to the impending risk of central bank tightening. This proved correct insofar as yield curves flattened aggressively but last week saw rate hike discount being trimmed by yields curve in USD, EUR, and GBP.

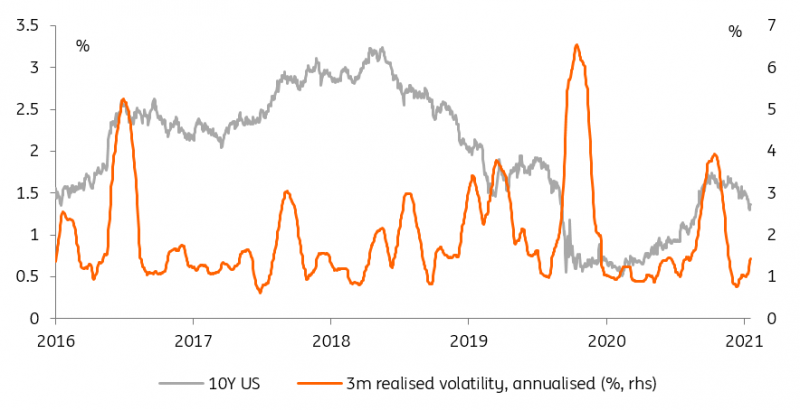

US yields dropped so far this summer but at the cost of higher volatility

Source: Refinitiv, ING

If a degree of softening can be seen in economic data, we do not share the gloom implied by the aggressive drop in interest rates globally. At least in part, we blame the move on a wash out in remaining reflation trades. Whether this washout is over is an open question, but this week brings a number of mitigating factors that could at least afford a pause in the curve flattening move.

All eyes on Powell for hints on tapering

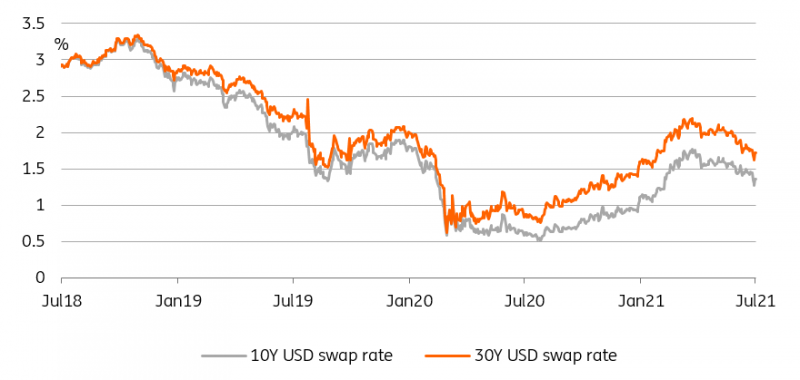

Supply is exhibit one. The US Treasury selling 10Y/30Y debt should help cater to buyers of long end debt, regardless of whether they are adding new positions or stopping out of old ones. Fed Chairman Jerome Powell’s semi-annual testimony will also be an opportunity for him to further prepare the ground for a tapering announcement later this year. Depending on how forceful he is, some selling of long-dated treasuries might also emerge there.

Supply and tapering hints should prevent a further drop in US rates

Source: Refinitiv, ING

Against these potential near term drivers for higher USD rates, a slight slowdown in CPI and PPI this week might not do much to help the case for a steeper curve. For one thing, inflation pressure remains elevated and the risk of Fed tightening as well as supply constraints slowing the economy is ever present. It should be repeated at this point that we do not share the gloom consistent with rates trading as where they are right now.

ECB forward guidance now in play

The build up to next week’s ECB meeting will be particularly interesting for EUR rates. the pre-meeting self-imposed quiet period starts on Thursday concentrating central bank headline risk to the first three days of the week. The ECB’s new interpretation of its price stability mandate could prompt a re-wording of its forward guidance on July 22nd. President Lagarde strongly hinted at such in a Bloomberg interview over the weekend, pointing out that forward guidance would be revisited to demonstrate the ECB's commitment. We expect that there is a range of diverging opinions on the governing council but risks are clearly skewed towards a more dovish guidance.

The result would be lower nominal rates for even longer. We are more sceptical about the impact on inflation expectations. Markets have fully integrated that inflation depends on many factors that lie beyond the control of the ECB, so the odds of a repeat of the US reflation trend in EUR market look pretty thin in our view.

Read the original analysis: Rates spark: Pause and think

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.