Rates spark: Living with inflation risks

The ECB is looking through higher headline inflation and inflation swaps. We doubt these will be enough to change easing expectations in December but hawkish comment risks will remain a threat to carry trades. In the US, inflation prints have not affected breakevens much in recent months, but as a stand-alone they point to ongoing above norm inflation.

Inflation risks everywhere, but no ECB policy implications

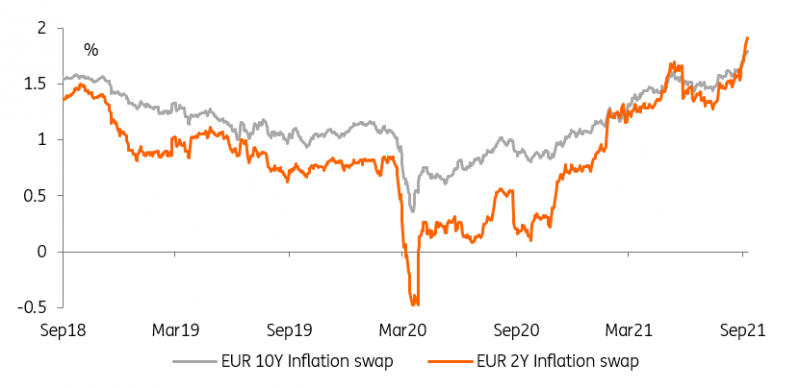

The relentless rise in EUR inflation swaps since their trough in the first stages of the Covid-19 crisis in March 2020 is striking. As such, it is not a new development but it is catching many investors’ attention as indicators such as the 5Y5Y rates reaches their 2017 peak, and as they are no longer far from the ECB’s inflation target of 2%. Meanwhile, elevated headline inflation, jumps in energy prices, and the steady drumbeat of ‘inflationary’ news stories about staff shortages, supply chain bottlenecks, etc keep inflation fears front and centre.

Long-term inflation swaps are also converging to the ECB's 2% target

Source: Refinitiv, ING

Despite a fairly relaxed communication on the topic at last week’s ECB meeting, President Christine Lagarde acknowledged the risk of upside surprises and put the focus on the current round of wage negotiations. An aptly-timed speech from her fellow board member Isabel Schnabel struck a similarly dovish tone yesterday, but also reviewed the risk factors that could blindside the ECB’s models in the coming months and year. Between the lines, the message was that the ECB does see what consumers see, although she also sought to reassure markets that so far they have no policy implications.

In all likelihood, the ECB can continue arguing this case in the coming months. It has already well flagged the fact that base effects are behind the recent jump, and are unlikely to subside before the new year. It would feel equally justified in looking through another jump related to energy prices. Second-round effects cannot be dismissed out of hand but it will take time for these to appear in traditional economic data. In short, inflation remains a concern but we doubt it will be enough to stop markets from expecting further ECB easing to be announced in December, even if hawkish headline risk remains ever present as early September has shown.

US inflation discount - neither hot nor cold; but likely to remain relatively warm

Despite the dramatic upmove in US inflation in previous quarters and the constant debate on the prognosis ahead, the inflation discount coming from breakeven spreads remains remarkably steady. There is a 2.6% per annum discount out to 5 years. This is not a new discount, as its been there for the past number of months. But its resilience is quite remarkable. The inflation discount for 2 years to 3 years at this rate is not that remarkable, given where inflation currently is, but the discount for 4 years and 5 years is quite elevated, as is the cumulative discount over the full 5 years.

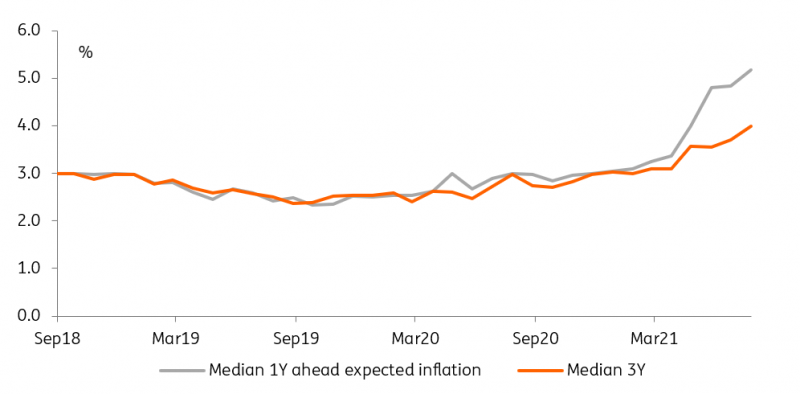

Consumer inflation expectations remain ingrained, and so will demand for inflation hedges

Source: New York Fed, ING

Then the longer term discount is in the area of 2.25% to 2.5%. Again not a dramatically high discount, but one that smells of a persistent inflation experience into the medium term. Whether we get a reaction to the US CPI release will be interesting. Likely we won't, even if there is a surprise. The consensus call out there has been to expect a drop in the breakeven, and for that to facilitate a rise in real yields. That's not our view. We think inflation expectations remain ingrained, which is backed up by ongoing flows into linkers, and for any rise in real rates to coincide with a medium-term recovery; a slow grind though.

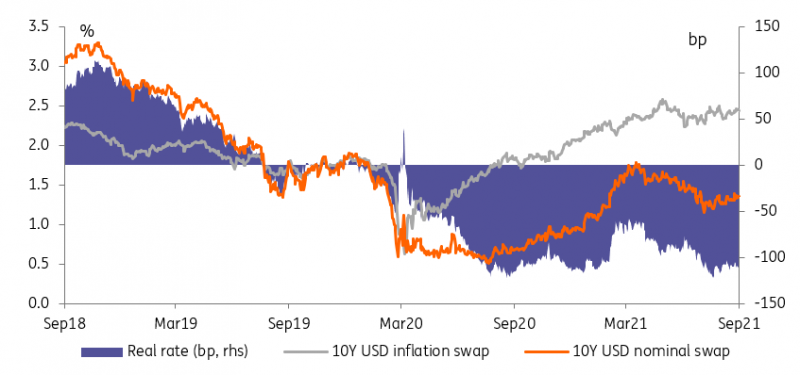

Real rates are set to climb as the recovery takes hold, but only slowly

Source: Refinitiv, ING

Read the original analysis: Rates Spark: Living with inflation risks

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.