Rates Spark: Kicking a bond when it’s down

Expect hawkish rhetoric from central bankers today but euro and dollar rate markets are already pricing in that outcome. Supply resumes this week, with a detrimental effect on duration, front-loaded to the start of the week.

Hawkish central banks well anticipated by markets

Rates markets will be looking to public appearances from European Central Bank board member Isabel Schnabel and Fed Chair Jerome Powell. Despite some notable differences in communication style and in economic fundamentals, markets have taken a uniform view that domestic inflation will soon be back under control, and that their respective tightening cycles will soon come to an end. What both central banks have in common is that the drop in rates, tightening in credit spreads, and rally in other risk assets make their task of bringing inflation back to target more difficult.

Many would object that in the current disinflationary trend, central bankers will not care if the yield curve prices rate cuts before the end of the year. We think this is more true of the Fed than of the ECB but, when it comes to it, we expect both officials to strike a hawkish tone. The main difference is that there is much less confidence about the downward trajectory of European inflation. This will make Schnabel’s push back against market pricing more potent than Powell’s.

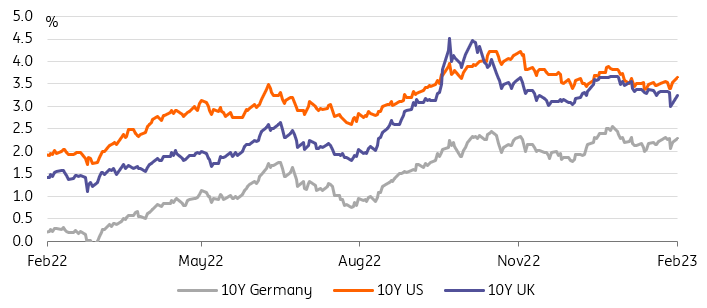

Helped by a bumper jobs report in the US, and hawkish post-meeting ECB comments, we would argue that both Schnabel and Powell face an uphill struggle to move yields up much further. 10Y Bund yields for instance are 25bp off their post-ECB meeting trough already, to a level we would call low but not strikingly so. The same goes for 10Y Treasury yields, around 3.6%, they are much lower than Fed funds but already 30bp above last week’s lows.

Bond yields have bounced convincingly off last week's lows

Source: Refinitiv, ING

Primary market activity picks up this week

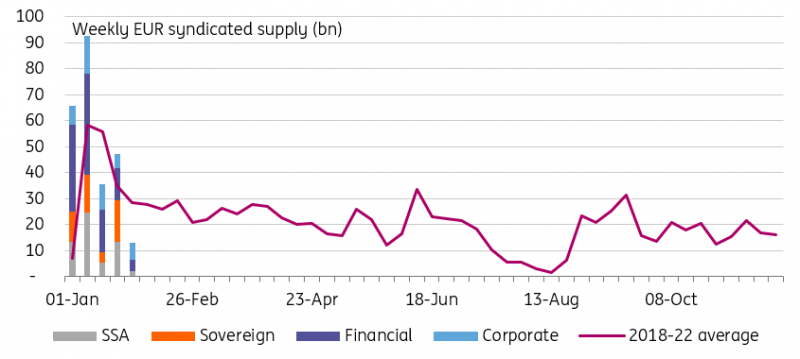

Bond issuance resumes in earnest after a week-long hiatus. Euro syndicated deals last week fell to €13bn from €47bn the week before. In the best of times, it is difficult to distinguish the impact of supply on rates direction. The effect tends to be transient, and localised. In addition, it was nearly impossible to make out its effect last week given the cascade of events and economic releases.

This week should prove easier. First of all, we expect some degree of catch up after a quiet week in primary markets. Secondly, some of the deals already announced reinforce that view, and speak to a skew towards longer-dated deals, at least today (see events section below). Thirdly, the fact that many European financials are still reporting this week should reduce the number of swapped deals, making the rest of issuance more market-moving, and also reducing its swap spread tightening impact.

As usual, the main challenge is timing. Looking to the US, long-dated 10Y/30Y auctions later this week are well flagged, and the long-dated France and Poland euro deals have probably already seen most of their market impact on rates direction. We would stop short of ascribing the bond sell-off on Friday and Monday to supply pressure, but we think it helped.

Bond issuance needs to catch up after a quiet week

Source: Refinitiv, ING

Read the original analysis: Rates Spark: Kicking a bond when it’s down

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.