Rates spark: Higher Oil prices meet a slowing global economy

Core bonds have so far shrugged off the jump in oil prices. This suggests that global growth concerns take precedence over the fear of another inflationary cycle. At the very least, this should keep rates volatility elevated, and provide a floor to long-term yields.

Higher Oil prices meet slowing global growth

The OPEC+ production cut announced over the weekend is a wild card that may well wrong-foot our call for lower rates this week. Our commodities strategist colleagues had to revise higher their oil price forecast as a result, with Bretn now expected to average $101/bbl over H2 2023, but bond markets have so far shrugged off the move. Rapidly declining growth expectations, especially in the US on the back of the regional banking crisis, go some way to dampen the contagion from energy to rates markets.

This view was lent some support from the decline in China’s PMIs, and the negative signal it sent about external demand. Our China economist notes a silver lining, however, in that the report increases the odds of fiscal support. China was not the only part of the world suggesting that higher oil prices may not fully translate into durable inflationary pressure. The drop in US ISM manufacturing, especially the forward-looking new orders component helped rates more than retrace their oil-induced jump.

It is still early days and higher oil forecasts from our colleagues clearly raises the stake for rates markets. In our base case, the decline in economic activity is advanced enough for markets to at least consider the detrimental effect it could have on already faltering growth. The alternative scenario is a daunting one, however. If growth fails to slow, already twitchy central banks may well conclude that more tightening is in fact needed.

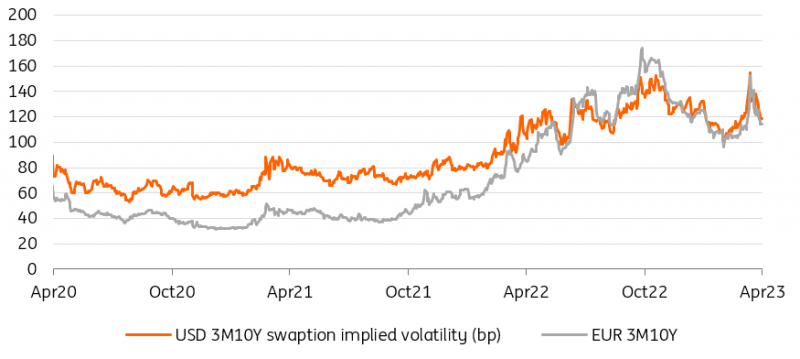

Higher Oil prices would raise the stakes for rates markets, preventing a fall in implied volatility

Source: Refinitiv, ING

The stakes are high for markets and swaptions reflect the wide range of outcomes

The argument for lower rates volatility for the remainder of this year rests on hopes that rates also converge lower. Even if this view, which is also our view, proves correct, lower rates may not translate into much lower volatility. At the macroeconomic level, higher volatility is simply a reflection of the wide range of possible scenarios, from disinflationary recession to inflationary economic rebound. Data, for now, corroborate the former scenario, but 2023 has proven that economic releases can be volatile. What’s more, both extremes could prove correct, not at the same time, but in succession.

Markets are nervous of banks remaining hawkish in the face of a recession

Indeed, even a recession and drop in inflation may not necessarily be the end of the inflation scare. The ‘three Ds’ (demographics, decarbonisation, and deglobalisation) often cited by economists mean that investors may well be justified in their fear that a subsequent recovery see a return of above-target inflation. This is one key reason why we doubt long-dated rates have much to fall in this cycle, as more dovish central banks would result in a greater inflation premium. This means that despite our view that 10Y Treasury yields will drop to 3% this year, we doubt lower levels can be sustained for long. The same is true for Bund yields falling below 2%.

The corollary is also that the more dovish central banks turn, the steeper yields curves will get. Price action so far this week suggests that markets are scared of the opposite: central banks remaining hawkish in the face of a recession. Hawkish comments from the likes of James Bullard at the Fed and Robert Holzmann at the European Central Bank yesterday probably fanned these fears.

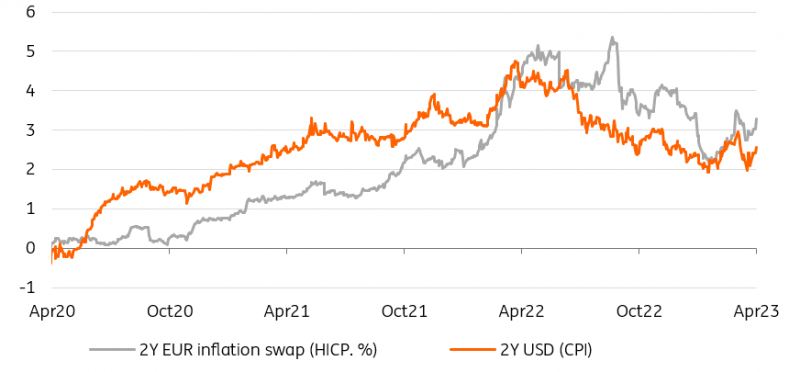

A jump in inflation swaps prevented short-end rates from dropping alongside long-dated ones

Source: Refinitiv, ING

Read the original analysis: Rates spark: Higher Oil prices meet a slowing global economy

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.