Rates spark: Exit strategy

The Bank of England should take a modest but significant step towards removing monetary accommodation today. Its next steps, hikes and balance sheet reduction, are up for debate. They will no doubt be watched by other central banks. Near term reaction might be a jump in GBP, and global, rates.

The slow grind toward zero net purchases

Perhaps unsurprisingly going into today’s Bank of England (BoE) meeting, and possible tapering announcement, GBP rates have been more volatile than their EUR and USD peers. Today and the coming months will provide further data points to central bankers at the Federal reserve and European Central Bank (ECB) on how to manage exit from exceptionally accommodative monetary policy. The UK is no sandbox however, the repercussions on other rates markets in case of botched communication could be significant.

Our expectation of a reduction from £4.4bn to £3bn in the weekly pace of purchases fits nicely with the amount left for the BoE to buy by the end of the year. At the new speed, it will reach its £895bn target this December. The advantage of a reduction now is that it will preclude the need for further reductions. As history suggests, the BoE seldom changes the pace of its purchases. It is also consistent with the more upbeat economic forecasts we expect the central bank to publish today.

The contrast with the ECB couldn’t be starker. The central bank has painted itself into a corner where every meeting is the object of endless discussions on the future speed of purchases, even if the eventual portfolio size has long been known. In our opinion, the BoE would do well to address the issue at this meeting, and leave it definitively behind it. Especially since it has bigger fish to fry.

Balance sheet reduction is within sight

Indeed, after today’s announcement, the focus should quickly turn to the upcoming tightening cycle. We are eagerly awaiting further information on which order the BoE intends to reduce its balance sheet and increase rates. Recent hints suggest that both could happen at the same time, we think in 2023 at the earliest. In the longer run, this needs not be a huge deal for GBP rates. We estimate that the marginal impact of balance sheet expansion has diminished, so it stands to reason that a gradual reduction would be manageable for gilt and interest rate swaps.

This invites two caveats however. First, markets might still react badly to the announcement in the near-term. This is particularly true at a time when the exit strategies of other central banks are under the microscope. Another, related, concern is be that some investors are linking asset valuation and central bank balance sheets too directly. Second, an earlier balance sheet reduction imply a steeper curve, especially if balance sheet reduction is a substitute for hikes.

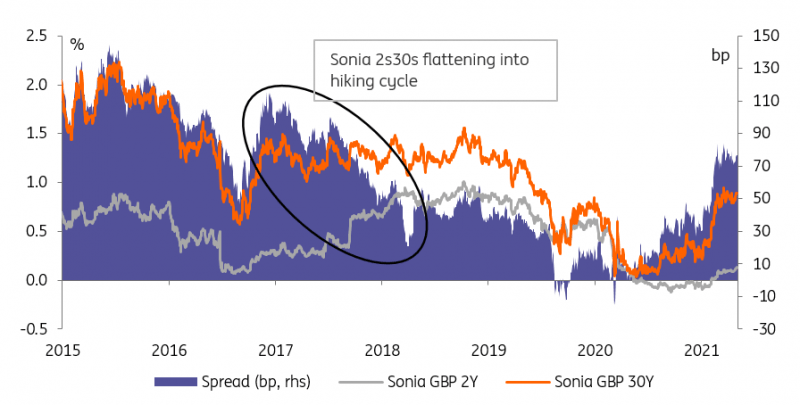

An earlier balance sheet run-off means the GBP curve could remain steeper for longer

Today’s events and market view

In addition to the BoE meeting, rates markets have to contend with bond sales from Spain (5Y/10Y/30Y) and France (10Y/20Y/30Y). EUR rates could be under upward pressure into the sales but might revert lower afterwards. On balance, we think the BoE’s announcement skews price action in favour of higher GBP rates, and this might well spill over into other markets.

There will be no letup in US employment data with initial jobless claims (although they relate to a different period than tomorrow’s payrolls) today. The barrage of Fed comments should continue with speakers too numerous to list here. Speeches of late have reinforced market expectations of officials putting the debate off for another few months, possibly into the Jackson Hole symposium.

Read the original analysis: Rates spark: Exit strategy

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.